Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

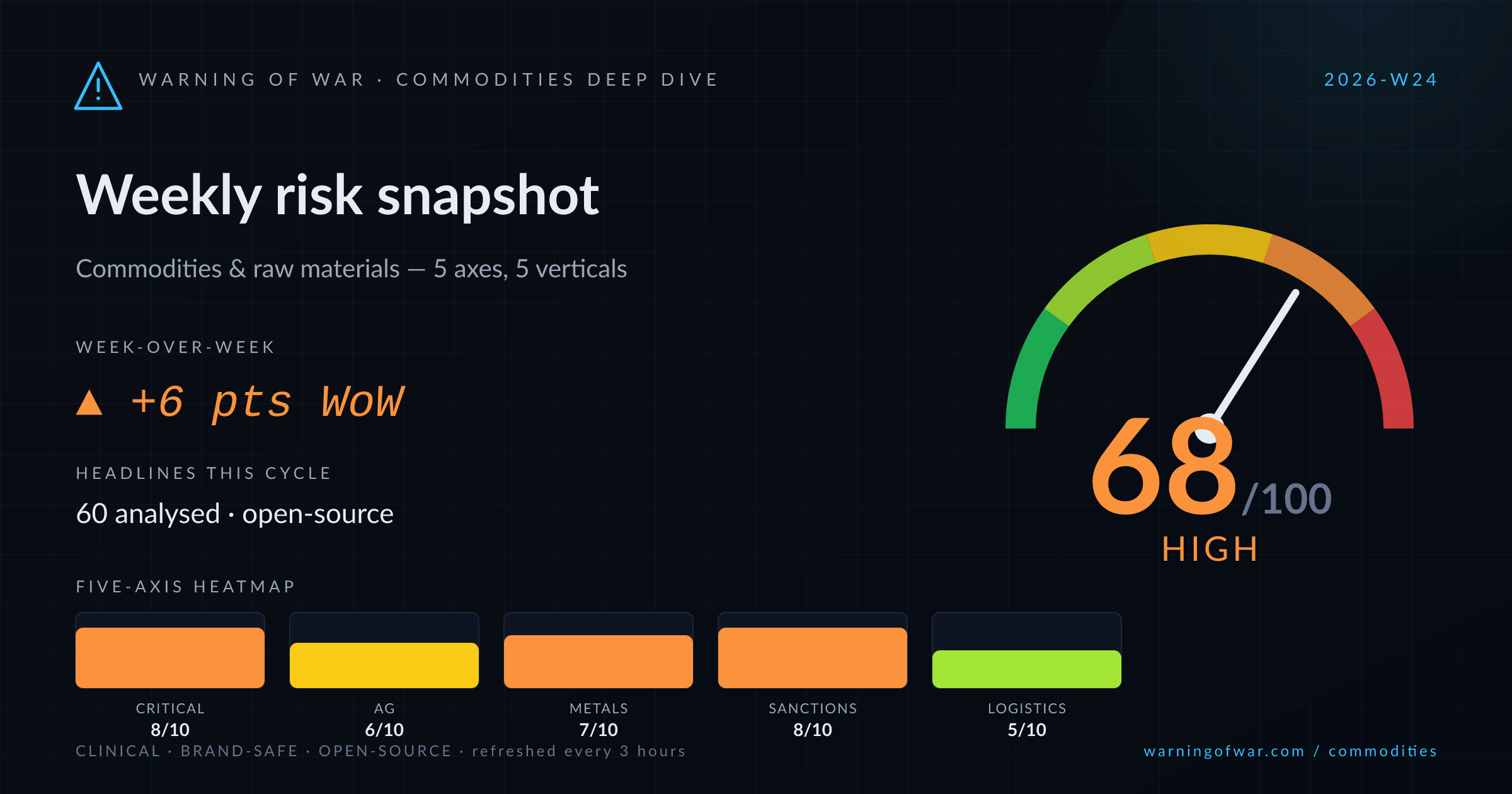

68/100 · High — +6 pts WoW.

This cycle's dominant signal is China's active rare earth export-control regime, driving yttrium and broader REE price appreciation with measurable pressure on EV, semiconductor, and defence supply chains. DRC cobalt export curbs are tightening battery-materials flows, while Woxna graphite (Leading Edge Materials) advances purification for premium applications. In base metals, copper commands bullish consensus at Jefferies' $17,636/t target; Nyrstar zinc smelters require a cumulative $345m bailout; and Century Aluminum is leveraging US tariffs and its Oklahoma facility for margin recovery. El Niño emergence threatens seasonal crop yields across Asia-Pacific, while Philippine rice price-cap enforcement and Malaysia's palm oil inventory build add regional agricultural price-management complexity.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Critical Minerals & Metals | 8/10 | High | ▲ +1 |

| Agricultural Markets | 6/10 | Elevated | → no change |

| Base & Industrial Metals | 7/10 | High | ▲ +1 |

| Export Controls & Sanctions | 8/10 | High | ▲ +1 |

| Logistics & Throughput | 5/10 | Guarded | → no change |

→ no change

China's rare earth export ban regime is causing demonstrable yttrium price appreciation and prompting diversification efforts in Brazil, Taiwan, and the US (DOMINANCE Act). DRC has imposed cobalt export restrictions generating a supply squeeze in a key battery element. Cornish Lithium advances UK domestic production while European Lithium faces merger-risk pressure from depressed lithium spot prices. Indonesia's revised nickel mining rules risk reducing Chinese operator participation, complicating cathode supply chains.

Operational signals

Headlines this cycle

→ no change

El Niño has formally emerged in the Pacific, raising yield-risk concerns for rice, corn, and wheat across Asia-Pacific growing regions. Taiwan's Taitung rice harvest faces weather disruption from heavy rains. Philippine authorities are actively enforcing a P50/kg imported rice price cap and evaluating a 30-day extension, signalling persistent import-price pressure. CBOT corn is technically consolidating near the $4.26–$4.28¼ range. Rice-farmer lobbies in Ghana are demanding a six-month import ban, adding policy uncertainty to import procurement flows.

Operational signals

Headlines this cycle

→ no change

Malaysia's palm oil reserves recorded their largest monthly jump in five months as export demand slumped, per MPOB data, widening the carry basis and pressuring CPO futures. Dekel Agri-Vision reported strong May production growth from its Ivory Coast operations, adding supply-side volume. El Niño emergence raises medium-term concerns for palm oil yields in Malaysia and Indonesia, as well as sugar and cotton in South and Southeast Asia. The net near-term picture is bearish on export demand but potentially bullish on a forward weather-risk premium.

Operational signals

Headlines this cycle

▲ +1 WoW

Copper is the standout signal: Jefferies' $17,636/t target exemplifies broad Wall Street upgrades, driven by energy-transition demand and tight mine supply. Near-term spot is softening (forecast lower 10-6-2026), but the structural bull thesis is intact. Nyrstar zinc smelters are losing $15m per month, requiring a cumulative $345m Australian federal-state rescue package. China's zinc treatment-charge margins have collapsed to record lows. Century Aluminum is positioning its Oklahoma smelter to benefit from US tariff protection. Aluminum fell to a one-month low on Iran-US tension and US rate-outlook uncertainty.

Operational signals

Headlines this cycle

▼ -1 WoW

Kazakhstan has announced construction of its first urea plant, a project valued at over 800 billion tenge, representing a significant Central Asian nitrogen-production capacity addition that could redirect regional import flows away from Russian and Chinese suppliers. Iran-US hostilities introduce indirect risk to Persian Gulf fertilizer shipping lanes (ammonia and urea flows from Iran, UAE, and Qatar). El Niño-driven demand forecasting for nitrogen applications in affected crop belts adds a forward procurement-timing consideration for importers.

Operational signals

Headlines this cycle

No named disruption events reported in this cycle.

Outlook pending next cycle.