Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

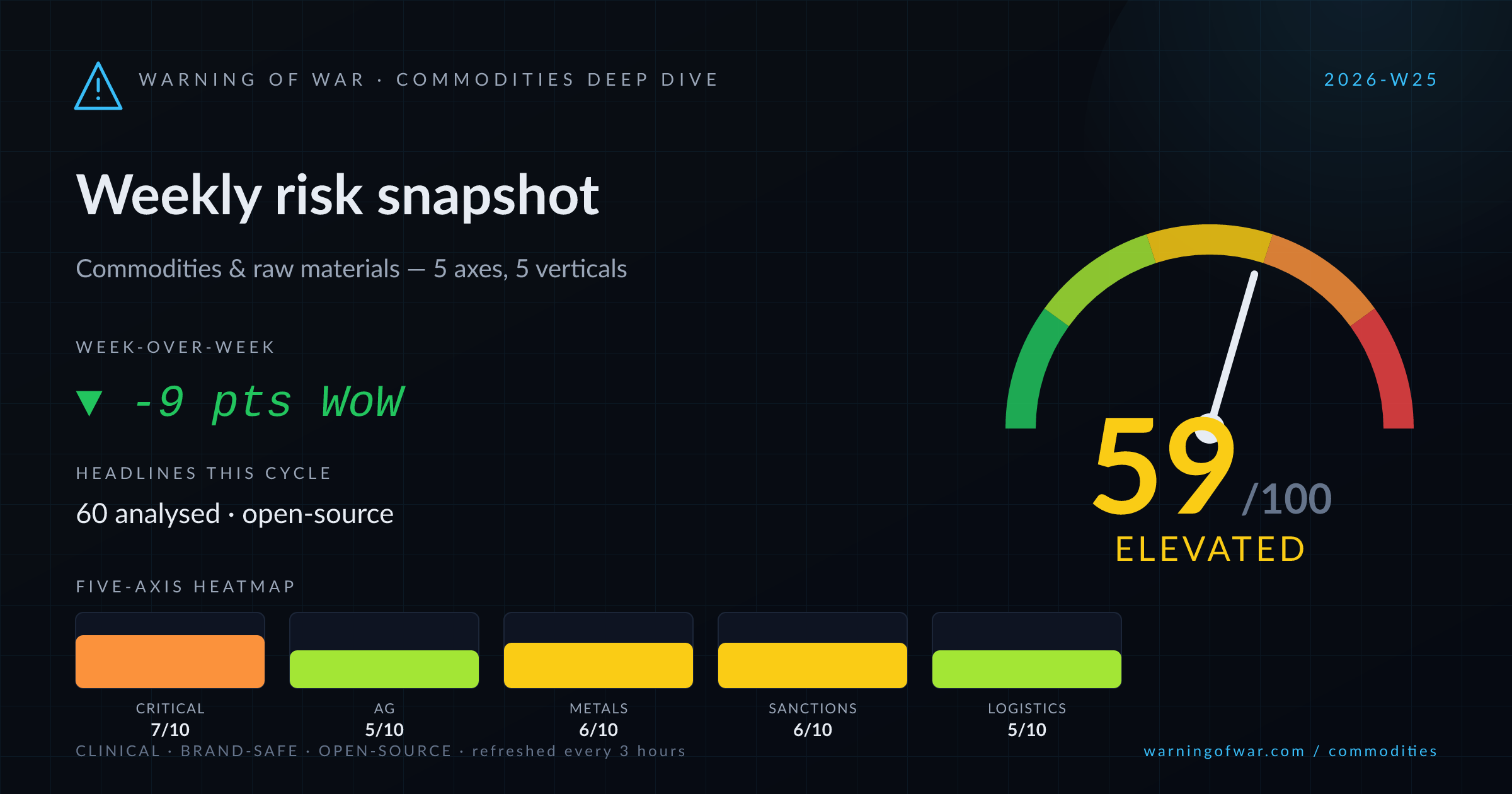

59/100 · Elevated — -9 pts WoW.

Critical minerals supply chains are under active strategic realignment: Nickel Industries (ASX: NIC) posted a near-5% share price surge, Indonesia's nickel-nationalism policy framework faces structural pressure from Chinese processing dominance, and Paladin is expanding ex-China rare-earth recovery nodes in South Korea and the Netherlands. Rio Tinto's Oyu Tolgoi copper export corridor in Mongolia faces a protest-driven operational blockade. Iron ore has breached the $100/t floor on abundant supply and subdued Chinese steel demand, while BHP and Rio Tinto pivot iron ore marketing toward Indian steel growth. An interim US–Iran accord is easing Hormuz transit risk, softening wheat and Middle East crude benchmarks, and loosening fertilizer-flow logistics.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Critical Minerals & Metals | 7/10 | High | ▼ -1 |

| Agricultural Markets | 5/10 | Guarded | ▼ -1 |

| Base & Industrial Metals | 6/10 | Elevated | ▼ -1 |

| Export Controls & Sanctions | 6/10 | Elevated | ▼ -2 |

| Logistics & Throughput | 5/10 | Guarded | → no change |

▼ -1 WoW

Paladin's South Korea and Netherlands expansion marks tangible allied supply-chain diversification away from Chinese rare-earth processing. Indonesia's nickel policy framework is under pressure from entrenched Chinese smelting technology. Nickel Industries (ASX: NIC) surged ~5% on a positive trading update. Lithium Ionic is presenting at the Fastmarkets Global Lithium & Critical Materials Conference in Las Vegas, signalling active capital-market engagement in battery-mineral supply chains.

Operational signals

Headlines this cycle

▼ -1 WoW

World wheat prices are declining as the northern hemisphere harvest advances — China's summer wheat harvest is 90% complete in major producing areas — and an anticipated Hormuz reopening removes a transport-cost premium. CBOT corn is hovering near $4.35, approaching a technical resistance zone at $4.19/$4.35, with weather and the upcoming USDA acreage report as near-term price catalysts. Taiwan's MFIG locked in a large Brazilian corn cargo, confirming South American export competitiveness.

Operational signals

Headlines this cycle

→ no change

Cocoa benchmark prices have declined substantially, with confectionery manufacturer Tony's Chocolonely characterising the fall as a significant commercial setback for producers dependent on premium pricing. Palm oil market conditions are tracked in the CME June 2026 monthly update, signalling ongoing volatility. Coffee is experiencing structural price appreciation driven by climate-related yield risks, prompting Japanese corporates and others to enter coffee farming as a capital allocation strategy.

Operational signals

Headlines this cycle

▼ -1 WoW

Iron ore spot prices have retreated below $100/t as supply remains ample and Chinese steel sector demand signals remain weak, with BHP and Rio Tinto actively redirecting marketing efforts toward India's growing steel consumption. Rio Tinto's Oyu Tolgoi copper mine in Mongolia faces a protest-driven export blockade to China, creating near-term tonnage risk. Copper is additionally pressured by anticipated 2026 supply tightness linked to mine disruptions and data-centre-driven demand growth. Steel benchmarks have dropped to a two-month low.

Operational signals

Headlines this cycle

▼ -1 WoW

Fertilizer prices are softening, but Arkansas-area agricultural operators report that the decline has arrived too late to benefit spring planting-season purchasing cycles, indicating demand-timing mismatches. The anticipated reopening of the Strait of Hormuz — a key transit corridor for Middle East-origin urea and ammonia — is expected to ease logistics costs and improve supply availability over the coming months. Broader oil-price easing following the US–Iran interim accord reduces ammonia feedstock (natural gas) cost pressure.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| Oyu Tolgoi Copper Export Blockade | base-metals | ACTIVE | Protesters have blocked copper export shipments from Rio Tinto's Oyu Tolgoi mine in Mongolia to China, creating a near-term operational tonnage disruption in an already tightening global copper supply outlook. |

| Strait of Hormuz Transit Normalisation | fertilizers | EASING | An interim US–Iran accord and associated tanker movement data indicate a progressive reopening of Hormuz transit lanes, reducing freight risk premiums for Middle East-origin urea, ammonia, and LNG cargoes. |

| Indonesia Nickel Policy Erosion | critical-minerals | ACTIVE | Indonesia's nickel downstream-processing nationalism framework is showing structural erosion as Chinese smelting technology maintains dominant operational control over in-country processing capacity, undermining policy objectives. |

| Iron Ore Sub-$100 Price Break | base-metals | ACTIVE | Iron ore spot benchmarks have declined below $100/t on abundant seaborne supply and a clouded Chinese steel-demand outlook, with BHP and Rio Tinto redirecting commercial focus toward Indian consumption growth. |

| Cocoa Benchmark Price Decline | agriculture-softs | ACTIVE | Cocoa prices have experienced a significant reversal from recent highs, with manufacturer Tony's Chocolonely characterising the fall as a major commercial setback for supply-chain participants dependent on elevated price floors. |

| Paladin Ex-China Rare Earth Re-shoring | critical-minerals | RISING | Paladin is advancing allied-supply-chain rare earth recovery infrastructure in South Korea and the Netherlands, reflecting accelerating G7-aligned policy momentum to diversify processing capacity away from Chinese facilities. |

Over the next 60–90 days, the dominant commercial theme across commodities markets will be the structural aftermath of Hormuz normalisation: wheat, fertilizer (urea/ammonia), and Middle East crude benchmarks are expected to recalibrate lower as freight risk premiums unwind, benefiting grain importers and downstream fertilizer users while compressing margins for producers in high-cost corridors. Copper supply tightness risks will intensify entering 2026 — the Oyu Tolgoi blockade, broader mine-disruption signals, and accelerating data-centre demand combine to keep LME copper structurally supported despite near-term China demand uncertainty. Iron ore is likely to remain range-bound below $100/t absent a material Chinese infrastructure stimulus announcement, with BHP and Rio Tinto's India pivot providing a longer-dated but not near-term demand offset. In critical minerals, G7 policy alignment on ex-China rare earth and nickel supply chains — visible in Paladin's European/Korean expansion and South Korean presidential G7 agenda items — will drive incremental capital allocation toward allied-supply projects, potentially tightening financing conditions for non-allied processing assets. Cocoa's price reversal warrants monitoring for second-order effects on West African producer revenues and soft-commodity fund positioning.