Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

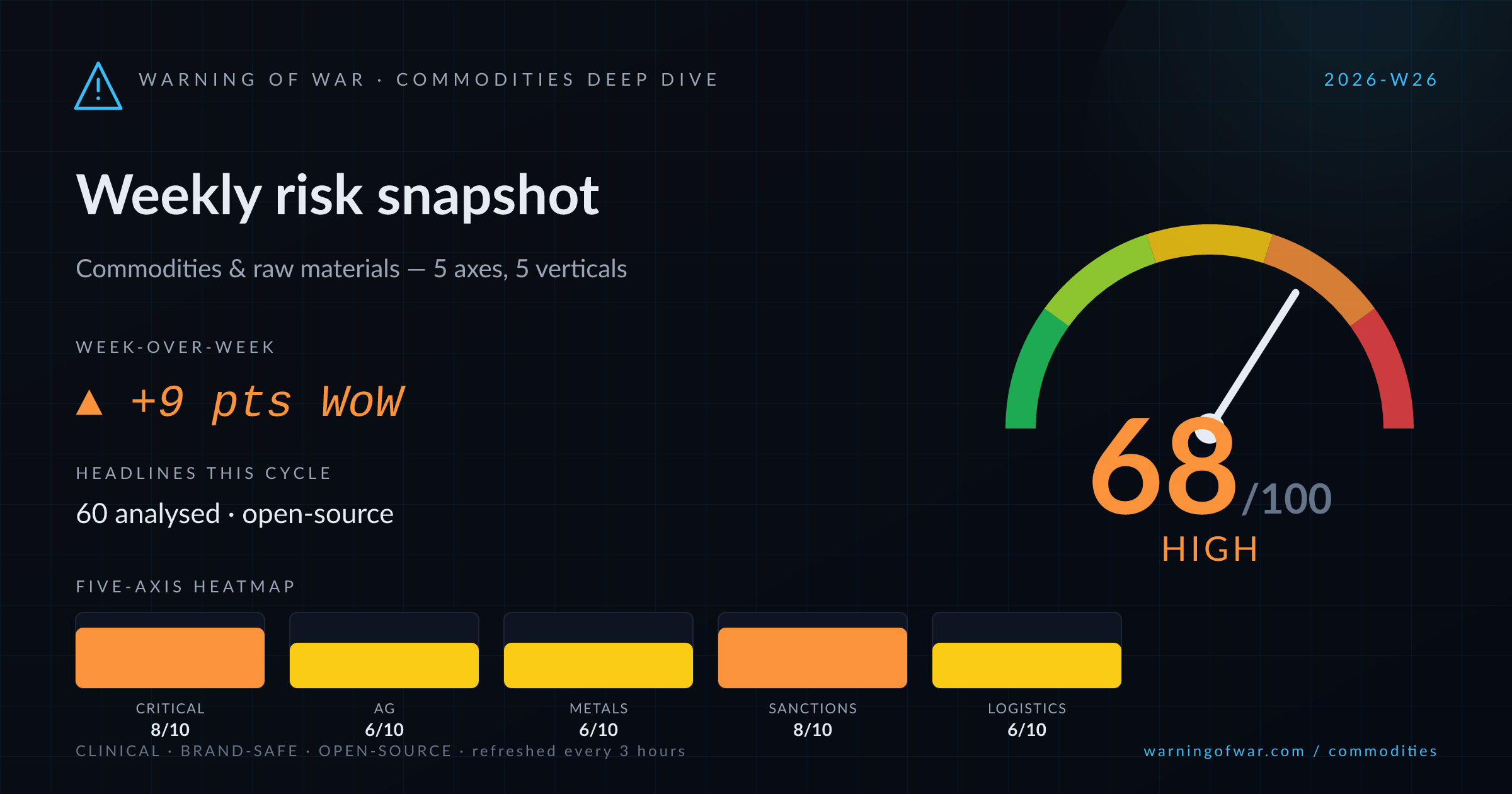

68/100 · High — +9 pts WoW.

China's throttling of critical-mineral exports to Japan (rare earths, gallium, germanium) under Xi-Takaichi geopolitical pressure marks the dominant commercial signal this cycle, reinforcing G7 CRMA re-shoring urgency. Congo's cobalt pivot toward Western offtake partners reshapes DRC supply allocation. LME copper retreats on a hawkish Fed and dollar strength; iron ore recovers from multi-month lows on Chinese restocking via Fenix/Pilbara corridors. The Black Sea grain corridor sustains throughput above 7,800 vessel transits. ICL's potash supply agreement with India's largest importer anchors phosphate/potash pricing ahead of kharif season. Persian Gulf tanker rates spiked to 897% of benchmark, adding freight cost pressure to fertilizer flows through Hormuz.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Critical Minerals & Metals | 8/10 | High | ▲ +1 |

| Agricultural Markets | 6/10 | Elevated | ▲ +1 |

| Base & Industrial Metals | 6/10 | Elevated | → no change |

| Export Controls & Sanctions | 8/10 | High | ▲ +2 |

| Logistics & Throughput | 6/10 | Elevated | ▲ +1 |

▲ +1 WoW

Beijing's decision to restrict critical mineral exports to Japan as geopolitical leverage (headlines 24, 40) is the highest-impact event this cycle. Pakistan's emerging rare-earth sector gains commercial attention as a potential alternative supplier (headline 12). G7 policy bodies are accelerating diversification frameworks (headline 51). PLS Group flags lithium market reliability as a structural constraint beyond price (headline 20), adding procurement-risk complexity for battery-supply chains.

Operational signals

Headlines this cycle

▲ +1 WoW

Over 7,800 vessel transits recorded through the Black Sea corridor (headline 1) confirm operational continuity of Ukraine grain exports. Egypt is actively expanding bilateral grain trade with Poland (headline 9), reflecting importer-side diversification strategy. Vietnam signals rice export recovery on high-quality demand (headline 27), while Afghan and West Bank wheat harvests proceed under logistical constraints (headlines 23, 19). US soybean export flows to China remain a monitored bilateral channel (headline 10).

Operational signals

Headlines this cycle

▼ -1 WoW

Commercial signal in softs is limited this cycle. A regional Ilocos Norte coffee development programme (headline 6) and Georgia Cotton Commission's scheduled annual meeting (headline 7) represent localised industry activity with no material price or supply impact. Zimbabwe's 10-year sugarcane expansion plan targeting ethanol and industrial output (headline 33) is a medium-term positive for sugar supply but does not alter near-term pricing. No material cocoa, palm oil, or coffee price disruptions are evident in the headline set.

Operational signals

Headlines this cycle

→ no change

LME copper held losses as a strengthening dollar and hawkish Fed posture weighed on non-ferrous benchmarks (headline 16), with copper testing technical support levels (headline 46). KGL Resources (ASX) and Rio2's Peru copper mine resource upgrade (headline 49) signal pipeline expansion, though near-term price headwinds persist. Iron ore staged a partial recovery from multi-month lows as China restocking activity lifted Pilbara-origin demand, with Fenix Resources (ASX:FEX) as a bellwether (headlines 25, 45). Gold dropped below $4,100 on tech-sector liquidation pressure (headline 35).

Operational signals

Headlines this cycle

▲ +2 WoW

StoneX analysis confirms a phosphate market cost floor that demand destruction cannot breach (headline 4), providing pricing support for DAP/MAP producers. ICL's potash supply agreement with India's largest importer (headline 30) anchors kharif-season procurement volumes and reduces spot-market uncertainty. Persian Gulf tanker rate spike to 897% of benchmark (headline 18) elevates fertilizer freight costs via Hormuz routing for Asian importers. Philippines-Egypt fertilizer trade dialogue (headline 3) and Pagudpud farmer aid distributions (headline 2) reflect active government procurement activity in Southeast Asia.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| China–Japan Critical Mineral Export Throttle | critical-minerals | ACTIVE | Beijing has implemented active export restrictions on rare earths and key minerals destined for Japan, creating near-term procurement gaps for Japanese semiconductor and EV component manufacturers reliant on Chinese gallium, germanium, and rare-earth oxide supply. |

| Congo Cobalt Offtake Reorientation | critical-minerals | RISING | The Democratic Republic of Congo is strategically redirecting cobalt offtake agreements toward Western buyers, reducing allocation to Chinese refinery networks and reshaping global cobalt supply-chain routing. |

| Black Sea Grain Corridor — Sustained Throughput | agriculture-grains | STABLE | The Ukraine Black Sea grain export corridor has maintained cumulative throughput above 7,800 vessel transits, sustaining operational wheat and corn export volumes from Ukrainian loading terminals. |

| Phosphate Cost Floor Establishment | fertilizers | STABLE | StoneX analysis confirms that phosphate market pricing has stabilised at a structural cost floor, limiting downside for DAP and MAP benchmarks even under demand-side pressure scenarios. |

| Persian Gulf Tanker Rate Spike | fertilizers | ACTIVE | An oil tanker booking in the Persian Gulf was executed at 897% of the benchmark rate, signalling acute freight cost inflation on Hormuz-routing lanes critical for fertilizer and petrochemical feedstock flows to Asian importers. |

| Iron Ore Multi-Month Low Recovery | base-metals | RISING | Iron ore benchmarks are recovering from multi-month lows, supported by confirmed Chinese steel-mill restocking demand drawing on Pilbara and West African origin cargoes. |

Over the next 60–90 days, the dominant commercial pressure point will be China's expanding critical-mineral export-control regime targeting Japan and potentially broadening to other G7 jurisdictions, accelerating G7 CRMA and US IRA re-shoring procurement timelines and supporting price premiums for ex-China rare-earth and gallium supply. Cobalt pricing will respond to DRC's western-reorientation policy as Chinese refinery intake contracts. On base metals, copper remains vulnerable to continued dollar strength and any Fed rate-hold signalling, while iron ore's restocking-driven recovery will be tested by Chinese property-sector data due in Q3 2026. Fertilizer markets face a dual pressure of a structurally supported phosphate cost floor and elevated Hormuz-route freight costs, which will keep CFR Asia urea and DAP pricing elevated through the kharif procurement window. The Black Sea grain corridor's throughput stability provides a partial buffer for wheat and corn importers, but Egypt and Southeast Asian buyers are actively diversifying bilateral supply chains — a trend expected to produce new trade-flow agreements within the forecast window. Lithium market reliability constraints flagged by PLS Group will increasingly shift procurement strategies from spot toward long-term offtake agreements among battery manufacturers.