Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

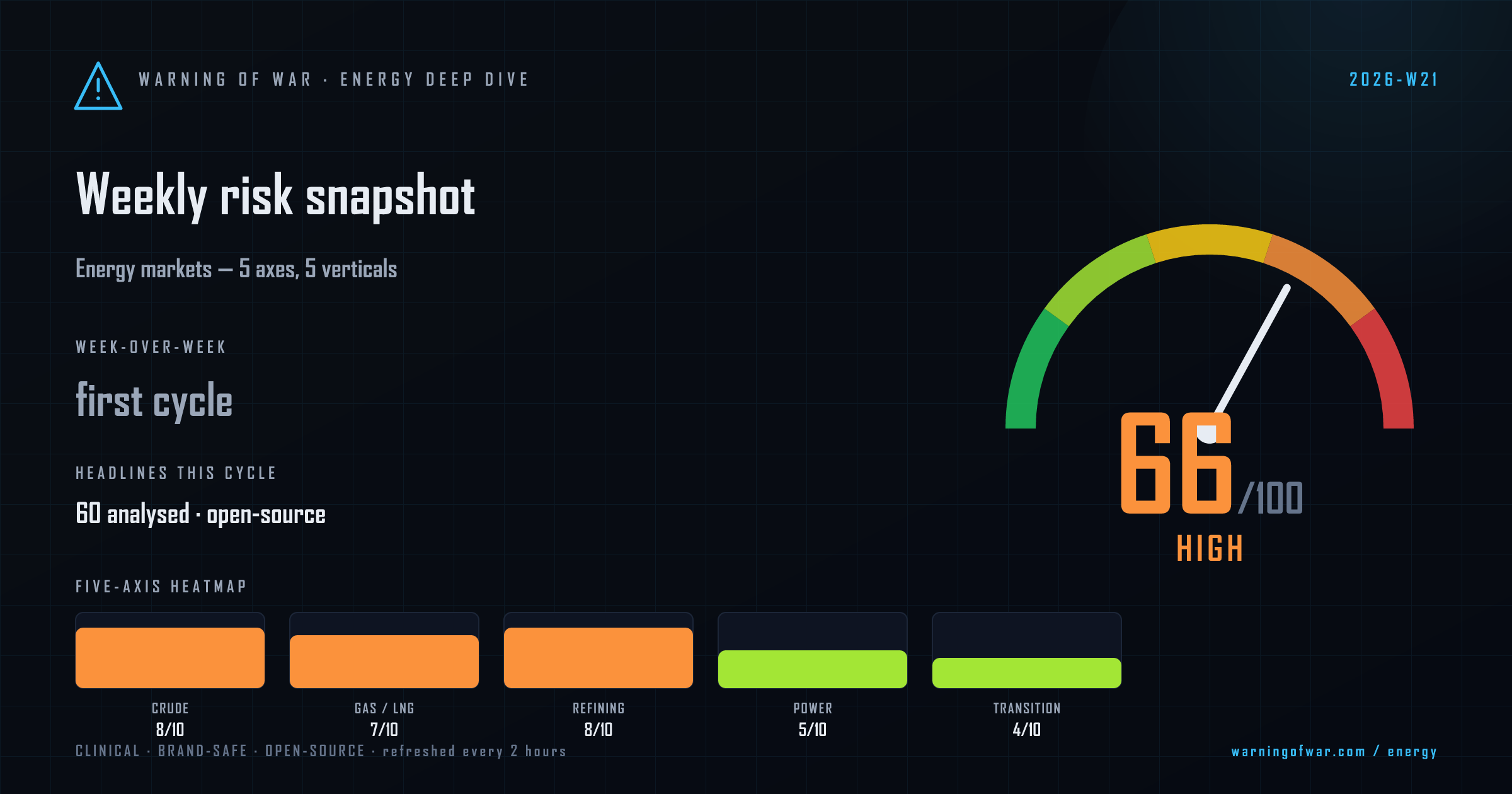

66/100 · High — first weekly snapshot.

Global energy markets are operating under elevated stress this cycle, driven by a convergence of Hormuz transit risk, Russian refinery capacity degradation, and Iran-related geopolitical premium on crude. WTI has pushed above $107/bbl as market participants price in potential military action against Iran. India's plan to dispatch empty tankers into the Strait of Hormuz for direct Gulf loading underscores growing concern over chokepoint operability. Ukraine's repeated drone strikes on the NORSI/Lukoil Kstovo refinery complex in Nizhny Novgorod Oblast — which handles approximately 5% of Russian crude throughput — are materially tightening Russian refined-product export capacity. The UK government has quietly loosened Russian oil sanctions in response to domestic fuel-price pressure. OPEC+ is signalling a June 2026 output increase, partially offsetting supply anxiety. On LNG, industrial action at two Australian offshore facilities introduces near-term liquefaction risk, while Russia-China Power of Siberia 2 negotiations gain strategic momentum as Hormuz disruption redirects Asian LNG procurement. Golar LNG and Flex LNG both report strong contract cover metrics, reinforcing firm LNG freight and tolling margins.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Crude Oil Supply | 8/10 | High | · — |

| Natural Gas & LNG | 7/10 | High | · — |

| Refining & Products | 8/10 | High | · — |

| Power & Grid | 5/10 | Guarded | · — |

| Transition & Policy | 4/10 | Guarded | · — |

(no prior week)

Crude markets are absorbing a meaningful geopolitical risk premium as Trump administration threats of military action against Iran keep Hormuz transit operability in question. Two supertankers carrying Iraqi and Qatari crude have successfully transited, providing partial relief, but India's decision to send empty tankers to load west of the chokepoint signals persistent anxiety among Asian importers. Nigeria's upstream segment shows structural weakness, with rig count falls driving a 41.7% decline in exploration activity per OPEC data. OPEC+'s flagged June 2026 output increase introduces a modest supply-side offset. The Indian Rupee's record low near 97/USD compounds import-cost pressure for price-sensitive South Asian buyers.

Operational signals

Headlines this cycle

(no prior week)

Industrial action at two Australian offshore LNG facilities following UGL wage-negotiation breakdown introduces near-term liquefaction supply risk at a moment when Asia is already scrambling to replace Hormuz-exposed Middle Eastern supply. The Hormuz situation is materially boosting Russian LNG imports into Asia, with one gas carrier delivering a cargo after six months at sea, illustrating the extreme rerouting economics now in play. Flex LNG has lifted guidance as contract cover tightens — a direct freight-market signal of supply scarcity. Inpex's commercial gas supply agreement with Indonesian state firms (Pupuk Indonesia, PLN, PGN) for the Abadi LNG project, PTT's 15 mtpa vision, and the Power of Siberia 2 'understanding' all point to a structurally tightening LNG landscape over the medium term.

Operational signals

Headlines this cycle

(no prior week)

The NORSI (Lukoil Kstovo) refinery in Nizhny Novgorod Oblast has sustained multiple confirmed drone strikes within a 72-hour window, with damage reported to storage reservoirs holding 140,000 cubic metres of product and active fire incidents. The facility processes approximately 11.6 million tonnes of crude per year, or roughly 5% of Russian national throughput. Repeated operational disruptions at this scale structurally reduce Russian domestic product availability and export capacity, with secondary tightening effects on European and Asian diesel/naphtha trade flows. Meanwhile, the UK's quiet relaxation of Russian oil sanctions introduces a price-relief valve but complicates enforcement credibility. Tata Steel has flagged crude-oil price hikes as a material cost risk to its Dutch operations.

Operational signals

Headlines this cycle

(no prior week)

Power and grid markets face two converging pressures this cycle. Data-centre and AI workload growth is materially reshaping electricity demand curves, creating new peak-load management challenges for grid operators in North America, Europe, and Asia. Energean's 41-day production halt at the Karish platform offshore Israel — attributed to the Middle East conflict's operational disruption — reduces gas availability to Israeli and regional power utilities, with Energean cutting both dividend and full-year production guidance. South Korea and Japan are intensifying bilateral energy cooperation in response to the Middle East supply crisis, with utility procurement strategies being revised. Pakistan's solar policy is under IMF scrutiny, adding policy uncertainty to South Asian power-sector planning.

Operational signals

Headlines this cycle

(no prior week)

Transition-sector activity this cycle is incrementally positive but below systemic threshold. A 30 MW green hydrogen project in Cumbria, UK, has reached FID — a modest but commercially meaningful signal for UK hydrogen infrastructure. Orient Green Power's Tamil Nadu wind capacity expansion and a ₹62 crore wind contract award reflect continued Indian renewable build-out. Commentary emerging from Iran-war oil-demand disruption frames the supply shock as a potential accelerant for clean-energy adoption, though this remains a demand-side signal rather than confirmed policy action. Pakistan's solar subsidy tensions with the IMF illustrate the ongoing political economy friction in emerging-market energy transitions. EU ETS and IRA implementation signals are absent this cycle.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| Lukoil NORSI Kstovo Refinery Strikes | refining-products | ACTIVE | The Lukoil NORSI refinery in Nizhny Novgorod Oblast — processing approximately 11.6 million tonnes/year, or ~5% of Russian crude throughput — has sustained multiple confirmed drone strikes within a 72-hour window, damaging product storage reservoirs (140,000 m³ capacity) and triggering active fire incidents. |

| Hormuz Strait Transit Risk | upstream-oil | ACTIVE | Ongoing Iran-conflict geopolitical pressure on the Strait of Hormuz has prompted India to plan direct in-Hormuz crude loadings for the first time since conflict onset, while Chinese buyers continue to receive supertanker deliveries of Iraqi and Qatari crude, indicating partial but operationally stressed transit continuity. |

| Australian LNG Facility Industrial Action | lng-gas | ACTIVE | Maintenance workers at two offshore Australian LNG facilities have commenced protected industrial action following the breakdown of wage negotiations with engineering contractor UGL, introducing near-term liquefaction and operational throughput risk. |

| Energean Karish Platform Suspension | lng-gas | EASING | Energean's Karish gas production platform offshore Israel was suspended for 41 days due to Middle East conflict-related operational disruption, causing Energean to reduce its full-year production guidance and cut its Q1 dividend. |

| UK Russian Oil Sanctions Relaxation | upstream-oil | RISING | The UK government has quietly loosened its Russian oil sanctions framework in response to domestic fuel-price pressure attributed to the Iran conflict, introducing incremental Russian barrel accessibility but undermining G7 sanctions-regime coherence. |

| Power of Siberia 2 Framework Agreement | lng-gas | RISING | The Kremlin has confirmed that a preliminary understanding has been reached on the Power of Siberia 2 pipeline connecting Russian gas fields to China, with the Iran-war-driven Hormuz risk serving as a strategic catalyst accelerating negotiations. |

Outlook pending next cycle.