Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

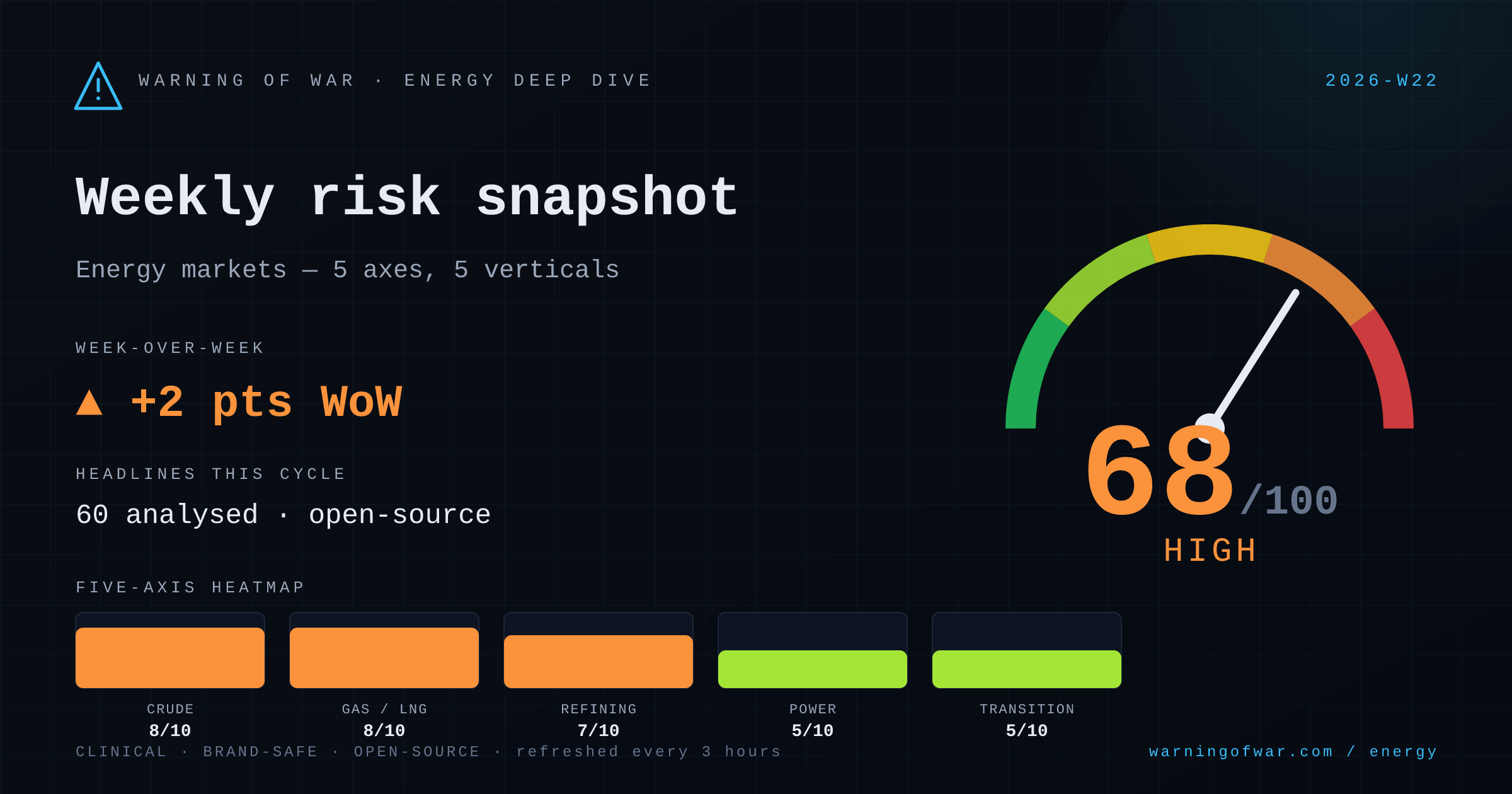

68/100 · High — +2 pts WoW.

The Strait of Hormuz closure—driven by U.S.-Iran hostilities—is the dominant commercial signal this cycle, with Brent and WTI pricing in a prolonged-disruption premium and ADNOC deploying tankers in "dark mode." The U.S. SPR has dispatched a rare Asian cargo, reshaping short-haul trade flows. Russia's Tuapse refinery has sustained its fifth successive drone strike, compressing Urals-grade crack spreads. UK Ofgem's 13% price-cap uplift from July 1 reflects wholesale gas pass-through from Middle East risk. CNOOC's Kenli 10-2 Bohai Sea field entering full production adds modest incremental supply. Canada-Germany LNG offtake alignment accelerates European de-Russification of gas supply.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Crude Oil Supply | 8/10 | High | → no change |

| Natural Gas & LNG | 8/10 | High | ▲ +1 |

| Refining & Products | 7/10 | High | ▼ -1 |

| Power & Grid | 5/10 | Guarded | → no change |

| Transition & Policy | 5/10 | Guarded | ▲ +1 |

→ no change

The partial Hormuz closure is the primary upstream signal: ADNOC is routing tankers in dark mode, the U.S. SPR has dispatched an Asian cargo for the first time since late 2022, and Fed official Logan has publicly cautioned that U.S. shale cannot fill the resulting supply gap. Oman crude prices fell more than $3/bbl mid-week as U.S.-Iran deal speculation emerged. CNOOC's Kenli 10-2 Bohai Sea field (China's largest offshore shallow-layer lithologic cluster) has commenced full Phase 1 production, providing a modest incremental offset. Petrobras continues to expand oilfield-services engagement.

Operational signals

Headlines this cycle

▲ +1 WoW

The Hormuz disruption is generating a sharp reassessment of LNG supply security. ADNOC's dark-mode LNG transit and U.S. LNG emerging as a Gulf hedge are reconfiguring short-term cargo economics. European analysts at WSJ warn the market is underpricing LNG supply risk. The Canada-Germany LNG deal advances Atlantic Basin de-Russification. Novatek is exploring LNG-to-power in Vietnam, extending Russian LNG reach into Southeast Asia. The Mozambique-Total $2 billion claims dispute adds project-execution risk to an expected liquefaction expansion. Asian early heat wave signals summer gas demand pull.

Operational signals

Headlines this cycle

▼ -1 WoW

Russia's Tuapse refinery on the Black Sea coast has sustained its fifth drone strike of the spring, creating cumulative throughput uncertainty for Urals-grade crude processing and Black Sea product exports. TotalEnergies has extended its retail fuel price cap in France through June, signalling downstream margin pressure in European product markets. Rajasthan petrol pump operators are threatening a supply strike from June 1, indicating product-distribution stress in India. MOL's Hungarian petrochemical olefin unit experienced an operational interruption during restart, reducing Central European naphtha/olefin availability.

Operational signals

Headlines this cycle

→ no change

Ofgem's 13% UK energy price cap increase from July 1, directly attributed to elevated wholesale gas costs linked to Middle East disruption, marks the most significant consumer-facing utility price event this cycle. Indonesia's Sumatra blackout is prompting regulatory review of PLN's operational structure via the Danantara fund. Asia's early heatwave is flagging potential summer peak-load stress for coal and gas-fired generation across the region. German storage policy (2027 FID deadline for 2029 grid-fee exemption) reinforces the commercial calendar for utility-scale storage investment.

Operational signals

Headlines this cycle

▲ +1 WoW

The IEA's Global EV Outlook 2026 release provides the headline benchmark for electrification trajectory this cycle. Kyivstar's 105 MW solar portfolio acquisition in Ukraine's Lviv region demonstrates ongoing private-sector renewable investment in conflict-adjacent markets. Paraguay's first large-scale solar tender signals frontier-market policy maturation. The USDA's move to restrict solar development on US farmland introduces a permitting constraint for utility-scale solar pipelines. Germany's storage grid-fee exemption framework and the Permian lithium co-production opportunity (LibertyStream) represent complementary supply-chain signals for energy transition.

Operational signals

Headlines this cycle

No named disruption events reported in this cycle.

Outlook pending next cycle.