Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

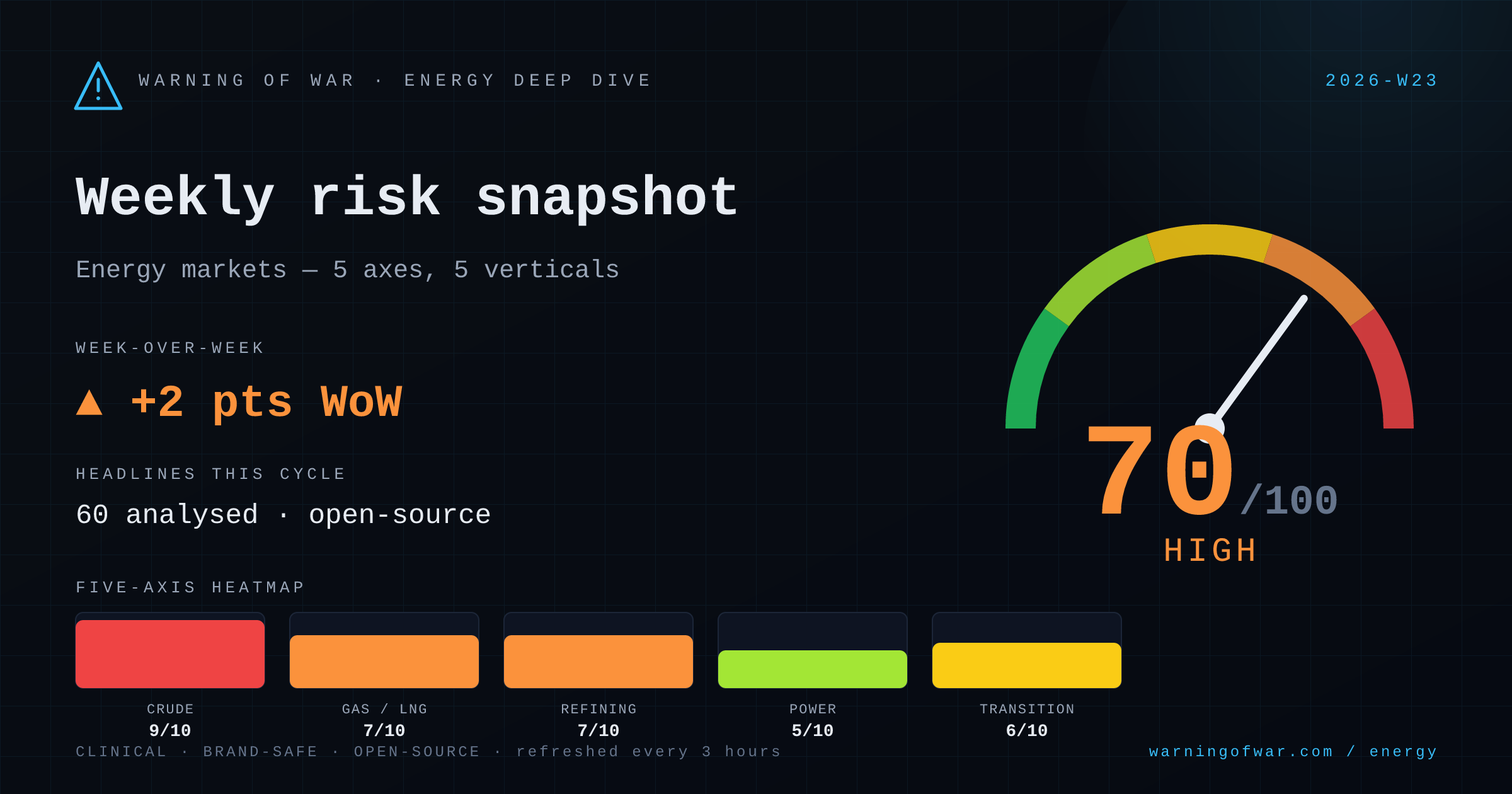

70/100 · High — +2 pts WoW.

The Strait of Hormuz closure is the dominant supply-side shock this cycle: Iraq is routing incremental barrels via Kirkuk–Ceyhan to Turkey's Mediterranean coast, while Kharg Island saw its first VLCC call in nearly a month, signalling partial Iranian export resumption under ceasefire fragility. WTI and Brent are pressing toward USD 100/bbl on US inventory drawdown and Iran-Gulf tensions. Russia–Saudi rapprochement is reshaping OPEC+ quota architecture as the UAE exits the bloc. US Secretary Rubio's signal on ending Russian oil sanction waivers adds secondary supply-side risk. The Novoshakhtinsk refinery in Russia sustained Neptune-missile-related unit outages, tightening Russian product export capacity. Centrica–Peyto and INEOS–Marubeni long-term LNG offtake deals point to continued European and Asian gas diversification away from Russian supply.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Crude Oil Supply | 9/10 | Critical | ▲ +1 |

| Natural Gas & LNG | 7/10 | High | ▼ -1 |

| Refining & Products | 7/10 | High | → no change |

| Power & Grid | 5/10 | Guarded | → no change |

| Transition & Policy | 6/10 | Elevated | ▲ +1 |

▲ +1 WoW

The Strait of Hormuz closure is forcing Iraq—OPEC's second-largest producer—to accelerate Kirkuk–Ceyhan pipeline exports toward a tripling of throughput within three months. Kharg Island received its first VLCC in nearly four weeks, indicating fragile export resumption. WTI is surging on sharp US inventory drawdown and Iran-Gulf military exchanges. Russia–Saudi realignment is redrawing OPEC+ quota governance, while the UAE's departure complicates collective output signalling. Venezuelan upstream recovery remains stalled by legal and infrastructure deficits.

Operational signals

Headlines this cycle

▼ -1 WoW

Centrica has locked in a 10-year natural gas supply agreement with Canada's Peyto, explicitly linked to LNG export markets—reinforcing the Canada-to-Europe gas corridor ahead of LNG Canada Phase 1 ramp-up. INEOS has signed a long-term LNG supply deal with Japan's Marubeni, deepening Asian offtake commitments. EXMAR is advancing the Dutch LNG terminal expansion, adding NW European regas capacity. TotalEnergies is permitted to divest its 10% stake in Russia's Arctic LNG 2, reducing Western exposure. LNG Canada Phase 2 has received a limited notice to proceed from the JGC joint venture.

Operational signals

Headlines this cycle

→ no change

Ukrainian Neptune missile strikes have knocked out two processing units at Russia's Novoshakhtinsk refinery, reducing Russian product export capacity and tightening regional distillate balances. Platts methodology changes to Middle East and Asia gasoil/jet fuel Market on Close processes reflect elevated price discovery complexity. Hormuz closure-driven crude rerouting extends freight costs and feedstock delivery windows for Asian and Middle Eastern refiners. Oman crude benchmark rose more than USD 5/bbl this cycle, directly pressuring refinery input costs across South and East Asia.

Operational signals

Headlines this cycle

→ no change

The EU has enacted energy-efficiency standards for data centres as AI-driven power demand growth strains grid capacity across member states. India's POWERGRID has tendered 3 GWh of battery storage projects in West Bengal, responding to grid-balancing requirements as variable renewables penetration rises. The St Petersburg oil terminal and naval base strike by Ukraine has no direct power-grid commercial implication but reinforces infrastructure vulnerability pricing across commodity markets. No major grid-collapse events or capacity-market crises are visible in this cycle's headlines.

Operational signals

Headlines this cycle

▲ +1 WoW

BlackRock-backed Atlas Renewable Energy has frozen USD 1 billion in planned Brazilian solar capacity citing chronic grid curtailment and national grid operator rejection of renewable dispatch—a material signal of merchant-risk deterioration in the Brazilian power market. The UK AR8 renewables auction timeline has been published with Gate 1 project exclusions, resetting competitive dynamics for offshore wind. Skyborn is approaching FID on a major Baltic offshore wind project. India, Mexico, Cambodia, and Zambia all show distributed and utility-scale solar deployment momentum. Platts is shifting US REC assessments (Texas, New Jersey, PJM) to daily frequency from 1 July, reflecting carbon-market liquidity growth.

Operational signals

Headlines this cycle

No named disruption events reported in this cycle.

Outlook pending next cycle.