Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

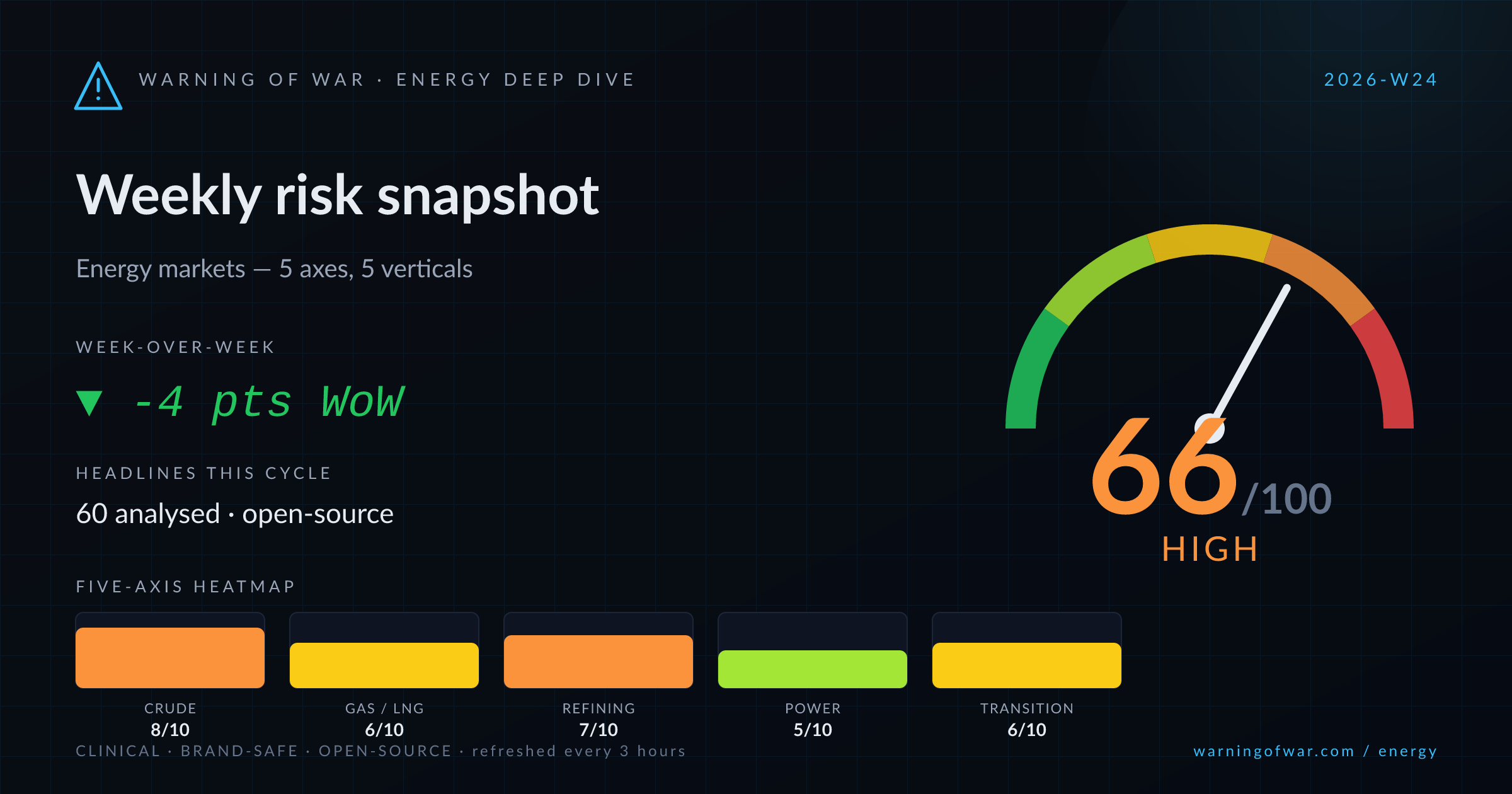

66/100 · High — -4 pts WoW.

Brent crude has breached $92/bbl following fresh US strikes on Iranian military assets near the Strait of Hormuz, with Iran retaliating against US forward bases in Jordan and Kuwait. China is drawing down commercial crude stockpiles to buffer Hormuz-related supply risk. Russian refining capacity at Kuibyshev (Samara) and Novokuibyshevsk is operationally impaired following drone strikes, with Dagestan gas pipeline infrastructure also affected. OPEC+ is conducting a capacity review and raising output. JERA–Petronas ink a landmark 20-year LNG supply agreement from 2028. WTI bears are testing the 100-day SMA near $87.50, creating near-term price dispersion across hubs.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Crude Oil Supply | 8/10 | High | ▼ -1 |

| Natural Gas & LNG | 6/10 | Elevated | ▼ -1 |

| Refining & Products | 7/10 | High | → no change |

| Power & Grid | 5/10 | Guarded | → no change |

| Transition & Policy | 6/10 | Elevated | → no change |

▼ -1 WoW

US–Iran military exchanges near the Strait of Hormuz have pushed Brent above $92/bbl, elevating Hormuz transit-risk premiums materially. China is drawing on commercial stockpiles, signalling physical tightness. OPEC+ is raising output following a capacity review, with Nigeria publicly backing the move. Kazakh Kashagan plans a 35–40 day maintenance window in 2027. Azerbaijan liquid-hydrocarbons output forecasts have been revised upward. Aker BP is advancing exploration productivity via a Viridien partnership. Algerian upstream field development is actively tendering.

Operational signals

▼ -1 WoW

The JERA–Petronas 20-year LNG offtake agreement (commencing 2028) is the cycle's defining long-term gas-security signal, locking Malaysian volumes into the Japanese power sector amid regional geopolitical uncertainty. Lithuania's Klaipėda terminal has allocated long-term regas capacities, reinforcing European LNG infrastructure diversification. Samsung Heavy is in direct talks for two additional FLNG vessels, indicating continued capex commitment. A fire on a Dagestan gas pipeline introduces spot-market and transit uncertainty for Caspian corridor flows.

Operational signals

→ no change

Multiple drone strikes have operationally impaired the Kuibyshev refinery in Samara and the Novokuibyshevsk refinery, reducing Russian crude-processing throughput. These outages reduce Russian product-export availability (diesel, naphtha, fuel oil) into global trade flows, exerting upward pressure on European and Mediterranean crack spreads. The supply tightening compounds the crude price spike from Hormuz tensions. No equivalent offsetting refinery capacity additions are visible in the current headlines.

Operational signals

→ no change

The UK's Labour government has achieved grid connection offers for more than half of clean energy schemes required for its 2030 target, a meaningful infrastructure milestone. Australia's energy minister is pressing data centres on renewables uptake amid blackout risk, reflecting demand-growth stress on the NEM grid. FERC's approval of SPP non-firm service for large loads signals regulatory adaptation to rising industrial demand in the US Mid-continent. India's Odisha state is deploying 180 MWh battery storage to enhance grid flexibility.

Operational signals

→ no change

China's solar manufacturing sector is under structural stress: 1,000 GW of installed capacity, 40+ producers entering insolvency, and modules priced below cost create a deflationary supply glut. US solar installations have crossed 6 million units, with Qcells completing a major US manufacturing hub. Meta–CleanMax are commissioning 900 MW of solar/wind in India. Norway is reviewing floating-wind subsidies, introducing project-economics uncertainty. Cenovus's CEO labelled a carbon-capture pipeline plan 'unfinanceable', signalling CCS financing headwinds. Barron's flags structural demand-side headwinds for oil.

Operational signals

No named disruption events reported in this cycle.

Outlook pending next cycle.