Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

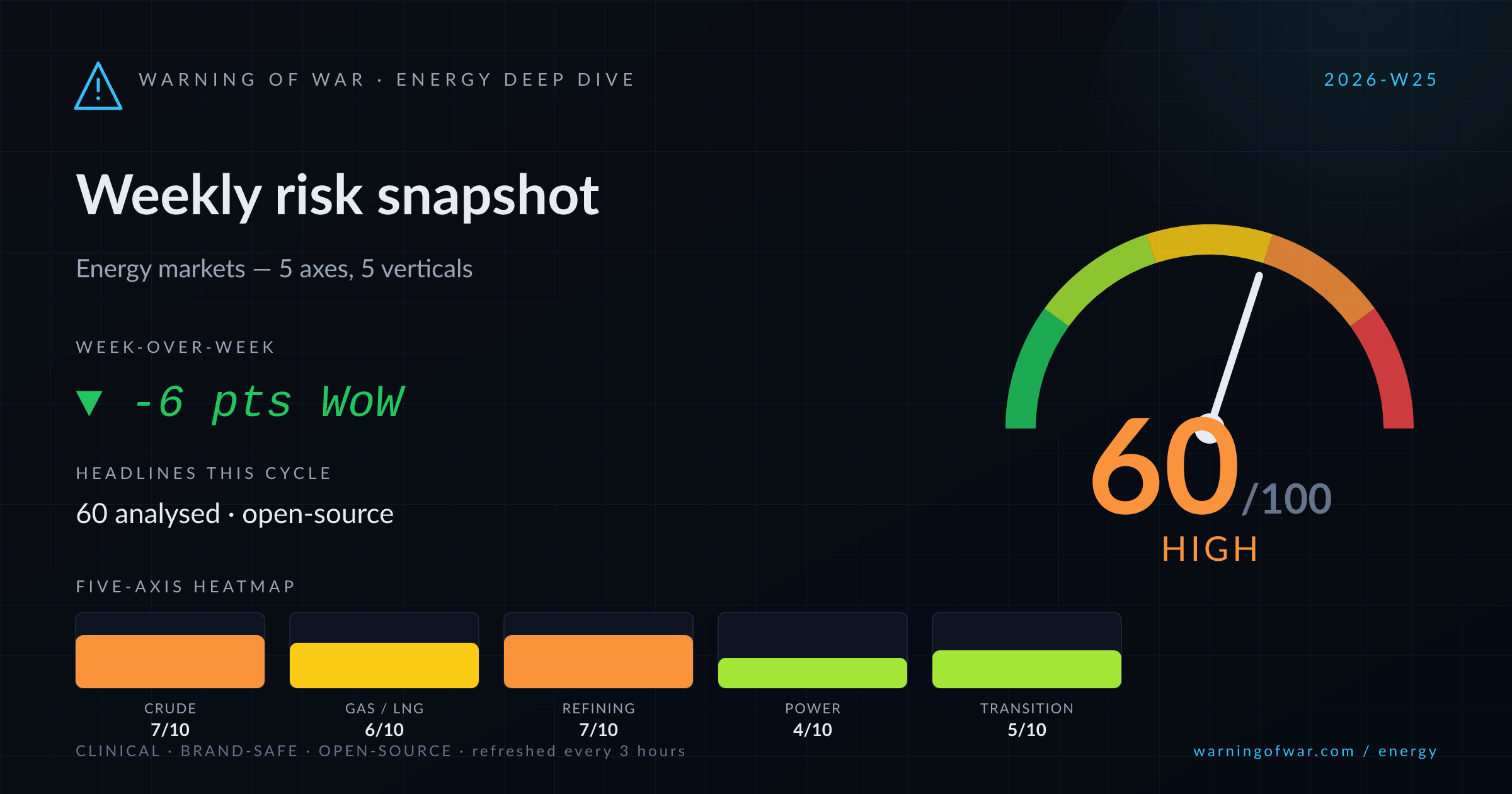

60/100 · High — -6 pts WoW.

A tentative U.S.-Iran peace agreement has triggered a rapid unwind of the Hormuz risk premium, with Brent falling below $80/bbl and WTI targeting the $73 range. Iranian crude exports have resumed, Murban and Dubai spot premiums have collapsed, and the IEA projects a significant 2027 oil surplus as Gulf supply recovers. However, shipping firms remain reluctant to transit Hormuz at full capacity, OECD oil reserves sit at 1990 lows, and a major Saudi refinery — cited by TotalEnergies CEO Patrick Pouyanné — will not return to full output until early 2027. The Ichthys LNG strike in Australia has resolved, easing short-term JKM pressure, while Qatar is repositioning tankers for Hormuz restart. ECB officials caution that Europe's energy price shock will persist for months despite the deal.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Crude Oil Supply | 7/10 | High | ▼ -1 |

| Natural Gas & LNG | 6/10 | Elevated | → no change |

| Refining & Products | 7/10 | High | → no change |

| Power & Grid | 4/10 | Guarded | ▼ -1 |

| Transition & Policy | 5/10 | Guarded | ▼ -1 |

▼ -1 WoW

The U.S.-Iran deal has shifted the crude oil price narrative from scarcity to prospective glut, with the IEA projecting significant 2027 surplus once Gulf output normalises. Iranian barrels are already moving past the former U.S. blockade. UAE output is forecast to exceed 5 million bpd post-OPEC quota constraints. OPEC+ compliance fell short in May. US commercial crude inventories drew 8.3 million barrels in the week to June 12, keeping near-term balances tight. OECD reserves have fallen to their lowest since 1990. Latin America, led by Rystad-tracked frontier plays, is emerging as the primary non-OPEC growth vector.

Operational signals

Headlines this cycle

→ no change

Resolution of the Ichthys LNG strike at Inpex's Australian facility removes a near-term supply overhang for Asian LNG markets. Qatar is repositioning tankers ahead of Hormuz reopening, signalling imminent QatarEnergy cargo flows into global LNG markets. ExxonMobil has committed to supply South Africa's first LNG import terminal via the Vopak-Transnet JV. Canada's $15.7 billion Kanata-Hanwha Ocean FLNG project advances. Bangladesh has approved three emergency LNG cargo imports. Europe's TTF-linked gas market continues to recover from the Hormuz shock per ECB assessment.

Operational signals

Headlines this cycle

→ no change

TotalEnergies CEO Patrick Pouyanné confirmed that a damaged Saudi refinery will not return to full operations until early 2027, sustaining product supply tightness independent of crude oil price moves. Collapsing Murban and Dubai crude premiums post-deal are opening arbitrage windows for Middle East crude into European and US refineries. Poland has legislated a 60% windfall tax on fuel companies that profited during the Hormuz crisis. Crack spreads remain structurally supported while Saudi refinery capacity sits below normal. Product trade flow re-orientation from Middle East crudes toward Atlantic Basin is accelerating.

Operational signals

Headlines this cycle

▼ -1 WoW

California's gas generation has fallen 60% relative to 2024 levels as utility-scale solar and interstate power imports displace gas-fired capacity, signalling structural demand erosion for gas in US power burn. The ECB's rate response to the European energy price shock adds financial stress to utility balance sheets exposed to floating-rate debt. South Korea's G7 energy supply chain resilience call reflects utility-sector anxiety over import dependency. Puerto Rico LNG-to-power projects advance via CLNE. CLNE's LNG system delivery for two Puerto Rico power projects highlights ongoing fossil-fuel dependency in island grids.

Operational signals

Headlines this cycle

▼ -1 WoW

India's installed solar capacity reached 157 GW, with renewables now accounting for 42.55% of total power capacity — a structural demand signal for solar supply chains. India also added 4.6 GWh of battery storage in Q1. OMV Petrom has taken FID on the 415 MW / 600 MWh Gabare solar-plus-BESS project in Bulgaria. Taiwan ranks fifth globally in offshore wind capacity. Atome's 145 MW post-FID green hydrogen project in Paraguay faces cancellation risk following unexpected government intervention. North Sea hydrogen storage study advances the UK seasonal capacity case.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| Strait of Hormuz Closure & U.S.-Iran Deal | upstream-oil | EASING | A tentative U.S.-Iran peace agreement has nominally reopened the Strait of Hormuz to crude and LNG transit, but shipping industry operators cite full-capacity resumption as unlikely before 2026, sustaining freight rate and route-risk premiums in the near term. |

| Saudi Refinery Outage (TotalEnergies / Pouyanné Assessment) | refining-products | ACTIVE | A major Saudi Arabian refinery sustaining damage during the Iran conflict will not return to full operational capacity until early 2027, per TotalEnergies CEO Patrick Pouyanné, maintaining a structural gap in global refined product supply independent of crude oil price recovery. |

| OECD Oil Reserve Depletion | upstream-oil | ACTIVE | OECD commercial oil reserves have fallen to their lowest level since 1990 following the Hormuz crisis-driven supply disruption, removing the strategic buffer that historically moderates acute supply shocks. |

| Ichthys LNG Strike (Inpex, Australia) | lng-gas | EASING | A weeks-long industrial dispute at the Inpex-operated Ichthys LNG facility in Australia has been resolved via a pay agreement with Offshore Alliance, AWU, and ETU unions, restoring full LNG export capacity from the facility and relieving near-term JKM spot market tightness. |

| Qatar LNG Tanker Repositioning | lng-gas | RISING | QatarEnergy has begun repositioning LNG tankers toward the Middle East in anticipation of Hormuz reopening, signalling an imminent resumption of full Qatari LNG export volumes into Asian and European spot markets. |

| Iran Crude Export Resumption | upstream-oil | RISING | Iran's first observed crude oil exports in approximately two months have transited past the former U.S. naval blockade point, with the Iranian tanker fleet simultaneously gearing up to accelerate volumes ahead of formal deal signing, materially adding to Atlantic and Asian crude supply balances. |

Over the 60–90 day forward window, the dominant commercial variable is the pace and credibility of Hormuz normalisation. Shipping industry reluctance to return to full Hormuz transit capacity — with the lobbying group citing 2026 for full volume recovery — will sustain elevated freight rates and product-supply tightness even as crude oil spot prices deflate toward the $73–80/bbl range. The Saudi refinery outage (TotalEnergies-confirmed, operational by early 2027 at the earliest) will keep diesel and jet crack spreads structurally supported through the remainder of 2025 and into H1 2026. The IEA's 2027 oil surplus projection — anchored on UAE output exceeding 5 million bpd and broader Gulf supply restoration — will continue to suppress medium-term futures curves and investor appetite for high-cost upstream projects. On gas and LNG, Ichthys restart and Qatar's tanker repositioning should progressively relieve JKM and TTF spot tightness, though the ECB's concurrent interest-rate hike in response to the European energy price shock adds cost-of-capital pressure to utility and infrastructure balance sheets. OECD reserve levels at 1990 lows create a re-stocking demand impulse that may provide a price floor, limiting the downside for Brent in the near term. Poland's windfall tax precedent may prompt similar legislative action in other European jurisdictions, introducing margin risk for refining-integrated energy majors operating in the EU.