Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

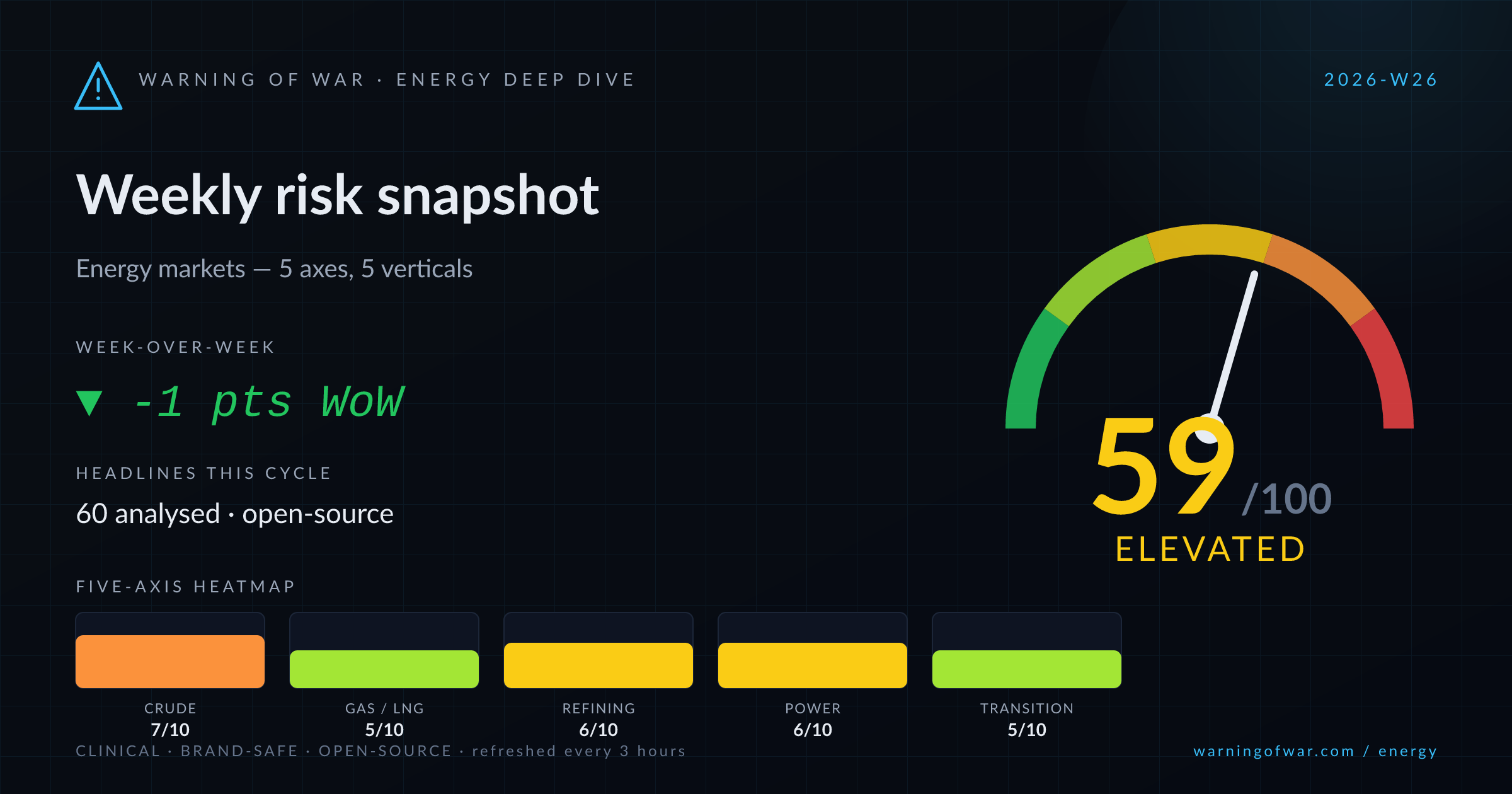

59/100 · Elevated — -1 pts WoW.

Global crude markets face simultaneous bearish pressure from Hormuz transit normalisation — stranded VLCC fleets re-entering supply — and Middle East production acceleration, pushing Brent below $75 and WTI to its lowest since March. OPEC cohesion is structurally weakening with UAE exit rhetoric threatening a 4-percentage-point share drop per EIA modelling. The Moscow Kapotnya refinery remains offline through at least 2026, forcing Russia to source gasoline imports from India and Kazakhstan. ExxonMobil's Antwerp refinery faces a full shutdown 29 June–3 July due to labour action. Cheniere's Corpus Christi Train 6 adds incremental US LNG capacity. J.P. Morgan cuts H2-2026 Brent forecasts; Dan Yergin anchors fair-value at $70–$85.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Crude Oil Supply | 7/10 | High | → no change |

| Natural Gas & LNG | 5/10 | Guarded | ▼ -1 |

| Refining & Products | 6/10 | Elevated | ▼ -1 |

| Power & Grid | 6/10 | Elevated | ▲ +2 |

| Transition & Policy | 5/10 | Guarded | → no change |

→ no change

The partial reopening of Hormuz transit routes under a US-Iran MOU has released a wave of stranded tanker cargo, adding volumes to already-pressured physical crude markets. Middle East NOCs are ramping output, the oil spread has flipped to contango, and OPEC cohesion is eroding as UAE exit speculation points to a potential structural 4pp market-share loss. J.P. Morgan and S&P Global (Yergin) both anchor price expectations in a $70–$85 corridor, capping upstream reinvestment signals.

Operational signals

Headlines this cycle

▼ -1 WoW

Cheniere Energy's Corpus Christi Train 6 completion adds incremental US LNG liquefaction capacity, reinforcing Atlantic Basin supply optionality. South Africa's Zululand FSU-based LNG terminal development advances infrastructure for sub-Saharan import demand. A Ukrainian strike on a Russian gas-processing plant near Kazakhstan poses a latent disruption risk to Central Asian pipeline gas flows. TTF day-ahead futures remain actively traded but no extreme price signal is visible this cycle.

Operational signals

Headlines this cycle

→ no change

ExxonMobil's Antwerp refinery (capacity ~100 kbd) will halt output 29 June–3 July due to a labour strike — a direct crack-spread support event in the ARA hub. The Moscow Kapotnya refinery is unlikely to resume operations in 2026 following drone-strike damage, forcing Russia into gasoline imports from India and Kazakhstan — an estimated 25% domestic production decline. China's Shandong teapot refiners have cut run rates to their lowest since 2017, tightening Asian product balances. Goldman Sachs cuts diesel margin forecasts but retains a structurally elevated crack view.

Operational signals

Headlines this cycle

▲ +2 WoW

A pan-European heatwave has triggered power grid stress events in France and Naples, Italy, surfacing near-term demand-side reliability risk for transmission operators and merchant generators. Structural grid demand growth signals are strengthening: AI data-centre load is projected to double power grid demand over the medium term per analysis from SMH. Adani Group targets 10 GW of private nuclear capacity in India by 2035 following sector liberalisation, a significant long-run generation-mix signal for South Asian grid planning.

Operational signals

Headlines this cycle

→ no change

Policy scaffolding for the energy transition continues to expand: the EU Hydrogen Bank announces its fourth auction round; Brazil schedules its first clean hydrogen subsidy auction for January 2027; Turkey publishes draft rules for a 1 GW offshore wind tender. First Solar is accelerating manufacturing capacity expansion. Petrobras approved FID on the RPBC biorefining project. The Philippines adds 422 MW of floating solar via the SunAsia-VinEnergo partnership. Ioneer advances lithium FID with a Hyundai offtake agreement, supporting battery-supply chain visibility.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| Hormuz Transit Normalisation | upstream-oil | EASING | US-Iran MOU framework has enabled stranded VLCC fleets to resume Hormuz transits, releasing backlogged Persian Gulf crude volumes into physical markets and flipping the key oil time-spread to contango. |

| UAE OPEC Exit Speculation | upstream-oil | RISING | UAE's potential departure from OPEC could reduce the organisation's global crude market share from 35% to 31% per EIA modelling, materially altering OPEC+ quota-management and price-support architecture. |

| ExxonMobil Antwerp Refinery Strike Shutdown | refining-products | ACTIVE | A labour strike forces full output cessation at ExxonMobil's Antwerp refinery from 29 June to 3 July, removing ARA-hub refining capacity and providing near-term crack-spread support for diesel and naphtha. |

| Moscow Kapotnya Refinery Extended Outage | refining-products | ACTIVE | The Moscow Kapotnya refinery is assessed as unlikely to resume operations before end-2026, potentially extending offline status to 2027, forcing Russia to source gasoline imports from India and Kazakhstan to offset a ~25% domestic production decline. |

| Ukrainian Strike on Russian Gas-Processing Plant | lng-gas | ACTIVE | Ukraine has struck a Russian gas-processing facility near the Kazakhstan border, introducing operational uncertainty for Central Asian pipeline gas flows and Russian upstream gas production volumes. |

| European Heatwave Grid Stress | power-utilities | ACTIVE | An intense summer heatwave across Europe has triggered power outages in France and Naples, Italy, exposing peak-demand vulnerability in transmission infrastructure and elevating near-term grid reliability risk for European utilities. |

Over the 60–90 day forward window, crude oil price action will hinge on the durability of the US-Iran MOU and whether Hormuz transit volumes normalise fully or face renewed restriction — any re-escalation would rapidly reverse the current contango structure and retest $80+ Brent levels. OPEC+ cohesion risk is the dominant structural overhang: a formalised UAE exit or accelerated quota-exempt production increases could entrench sub-$75 Brent, pressuring upstream E&P capex budgets for H2-2026 planning cycles. In refining, the Antwerp restart post-strike and the Russian gasoline import programme from India will be the key margin-directional signals for ARA and Asian product markets respectively, with Chinese teapot utilisation recovery contingent on Beijing export-quota liberalisation. European power grids face continued heatwave-season reliability risk through August, with AI-driven load growth adding a structural demand overhang that capacity markets have not yet priced. On the transition front, the EU Hydrogen Bank fourth auction and Brazil's 2027 clean hydrogen programme will advance project pipelines but near-term commercial impact remains limited pending final subsidy structures.