Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

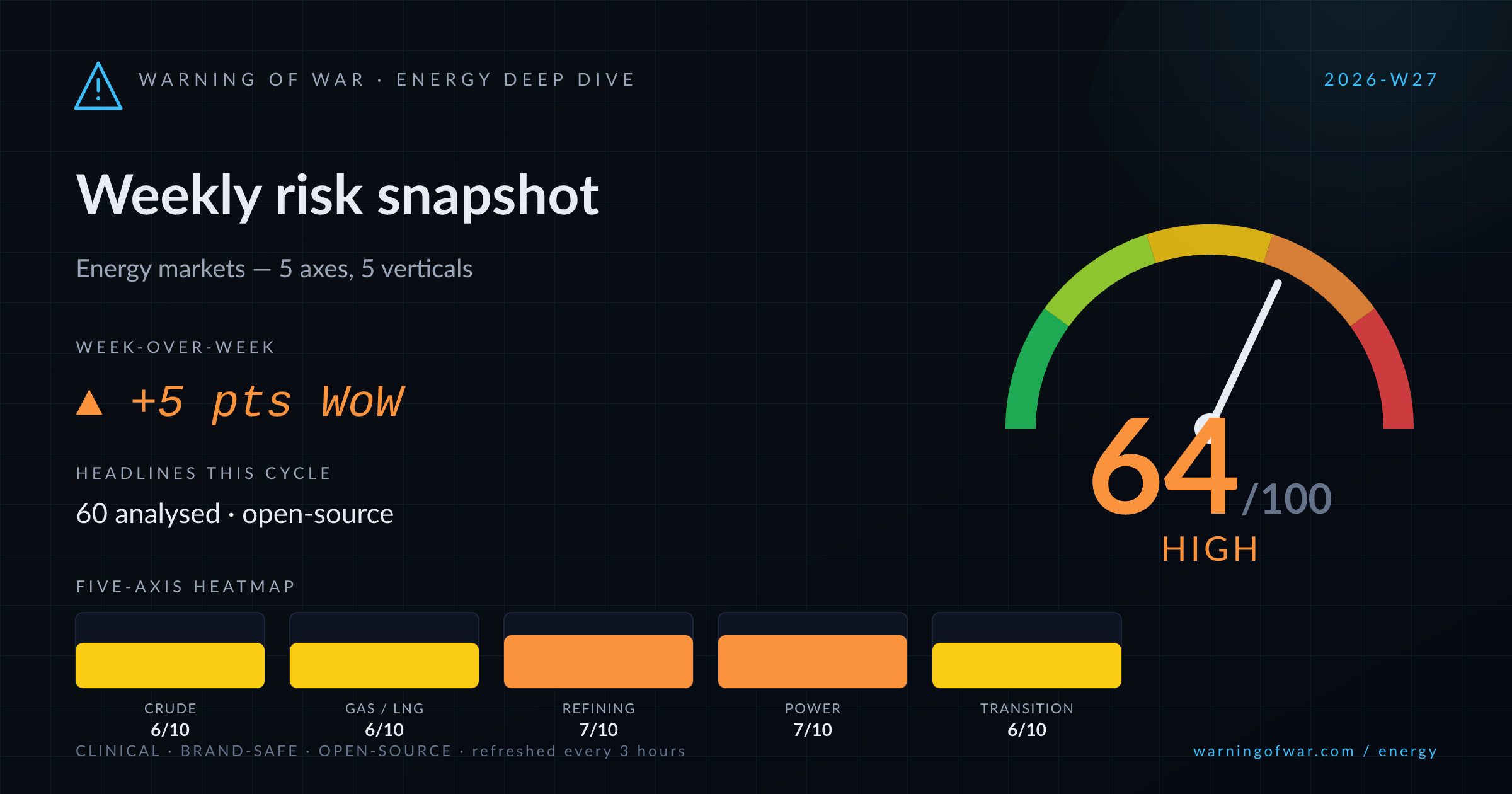

64/100 · High — +5 pts WoW.

WTI has slipped below $70/bbl — its weakest level since late February — as OPEC+ prepares a further 188,000 bpd output increase for August, Saudi Aramco moves rare spot cargoes, and US-Iran diplomatic talks in Doha ease geopolitical risk premiums. A 3.8 million-barrel EIA drawdown partially offsets bearish supply pressure. Russia's Slavyansk-na-Kubani and Ufa refinery complexes have sustained operational disruptions, tightening Russian product balances and prompting Indian gasoline imports. Iraq's West Qurna 2 NDA with Chevron signals near-term upstream capacity ambitions. JERA's new Singapore trading arm and the India-Japan LNG security pact signal structural LNG demand growth in Asia.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Crude Oil Supply | 6/10 | Elevated | ▼ -1 |

| Natural Gas & LNG | 6/10 | Elevated | ▲ +1 |

| Refining & Products | 7/10 | High | ▲ +1 |

| Power & Grid | 7/10 | High | ▲ +1 |

| Transition & Policy | 6/10 | Elevated | ▲ +1 |

▼ -1 WoW

WTI has breached $70/bbl to multi-month lows, pressured by a confirmed OPEC+ August quota hike of ~188,000 bpd and Saudi Aramco's rare entry into spot sales to accelerate shipment volumes. EIA data shows a 3.8 mb drawdown to 408.4 mb, providing partial support. Iraq's NDA with Chevron over West Qurna 2 operatorship signals meaningful upstream capacity ambitions in the Basra basin. US-Iran technical talks reduce near-term Hormuz risk premium.

Operational signals

Headlines this cycle

▲ +1 WoW

LNG market signals are constructive on the demand side. JERA — Japan's largest LNG buyer — has established a standalone Singapore-based global trading subsidiary (JERA GES), expanding its upstream, shipping, and low-carbon fuel footprint. India and Japan are formalising an LNG security pact. LNG Canada's first operational year is tightening western Canadian gas supply. Oman LNG has launched its first Muscat export voyage. Shell projects 65% global LNG demand growth to 2050, while Hormuz risk is reframing the post-2027 supply outlook.

Operational signals

Headlines this cycle

→ no change

Multiple Russian refining assets — Slavyansk-na-Kubani and Ufa — have experienced operational interruptions, with Kyiv's strike campaign reportedly affecting eleven Russian refinery complexes in a single month. Russia has moved to source gasoline from India to address domestic supply shortfalls, a structurally significant trade-flow shift. ENI and Mercuria's new commodity trading joint venture adds a major new participant in European and global product arbitrage flows, potentially reshaping naphtha and middle-distillate routing.

Operational signals

Headlines this cycle

▲ +1 WoW

PJM, the largest US power grid operator spanning 13 states, has issued formal warnings ahead of anticipated record electricity demand this summer, underscoring generation adequacy and transmission stress risk. South Korea is developing a $1.3 billion renewable energy platform (KKR/SK Inc.) to address surging AI and semiconductor manufacturing load. These signals collectively point to structural demand acceleration outpacing committed generation and transmission capacity in key markets.

Operational signals

Headlines this cycle

▲ +1 WoW

Orica has reached FID on a $432 million renewable hydrogen project in NSW Hunter Valley, Australia. South Korea selected 1,786 MW of offshore wind in its 2026 fixed-price auction. UK rooftop solar is projected to nearly triple capacity by 2030, though consent rules may constrain the next CfD auction cycle. EU ETS overhaul faces industry pushback as carbon-market reform accelerates. Delhi's 2026 EV policy creates a regulatory pathway for hydrogen vehicles. Detroit OEMs face hybrid-transition risk. Co-located solar-plus-storage deployment faces UK policy gaps.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| Russian Refinery Strike Campaign | refining-products | ACTIVE | Kyiv's deep-strike operations have disrupted eleven Russian refinery complexes — including Slavyansk-na-Kubani and Ufa — within a single month, reducing available run rates and triggering Russian gasoline procurement from India. |

| OPEC+ August Output Quota Hike | upstream-oil | RISING | OPEC+ is likely to approve an additional 188,000 bpd output quota increase for August, continuing the accelerated unwind of voluntary production cuts and adding further downward price pressure to WTI and Brent. |

| WTI Sub-$70 Price Slide | upstream-oil | ACTIVE | WTI crude has declined below $70/bbl to its lowest level since late February, driven by OPEC+ supply expansion signals, Saudi Aramco spot sales, and easing US-Iran geopolitical risk premium. |

| PJM Record Demand Warning | power-utilities | RISING | PJM, the US's largest grid operator, has issued formal operational warnings ahead of projected record summer electricity demand, raising reserve margin and transmission adequacy concerns across its 13-state footprint. |

| US-Iran Doha Technical Talks | upstream-oil | RISING | US and Iran are engaged in technical talks in Doha aimed at a peace framework and shipping-lane normalisation, reducing near-term Hormuz risk premium but leaving core nuclear and sanctions disputes unresolved. |

| Hormuz Disruption LNG Supply Reframing | lng-gas | STABLE | Scenario analysis of a potential Hormuz disruption is actively reframing LNG supply routing and contracting strategies through 2027, with Shell noting global LNG trade at 422 million tonnes and demand projected to grow 65% by 2050. |

Over the next 60–90 days, crude oil prices face continued downward pressure as OPEC+ executes successive monthly quota increases — each increment approximately 188,000 bpd — while Saudi Aramco actively manages elevated output via spot market sales; WTI is likely to remain range-bound in the $65–$72/bbl corridor absent a breakdown in US-Iran Doha talks or an unexpected geopolitical supply shock at Hormuz. Russian refining capacity will remain constrained by ongoing operational disruptions, sustaining India–Russia product trade flows and marginally tightening regional diesel and naphtha balances outside Russia. In the LNG vertical, JERA GES's Singapore operations and the India-Japan security pact will accelerate Asian offtake consolidation and long-term contracting activity, supporting JKM price stability into the winter restock cycle. PJM's record demand warnings signal that US power capacity margins and merchant power prices will face acute stress through the August peak-load window, providing a near-term uplift signal for gas-fired generation dispatch and Henry Hub spot prices. On policy, EU ETS overhaul negotiations, the UK solar CfD auction cycle, and South Korea's offshore wind fixed-price contracts will be key watch points for renewable investment pipeline visibility in Q3–Q4 2025.