Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

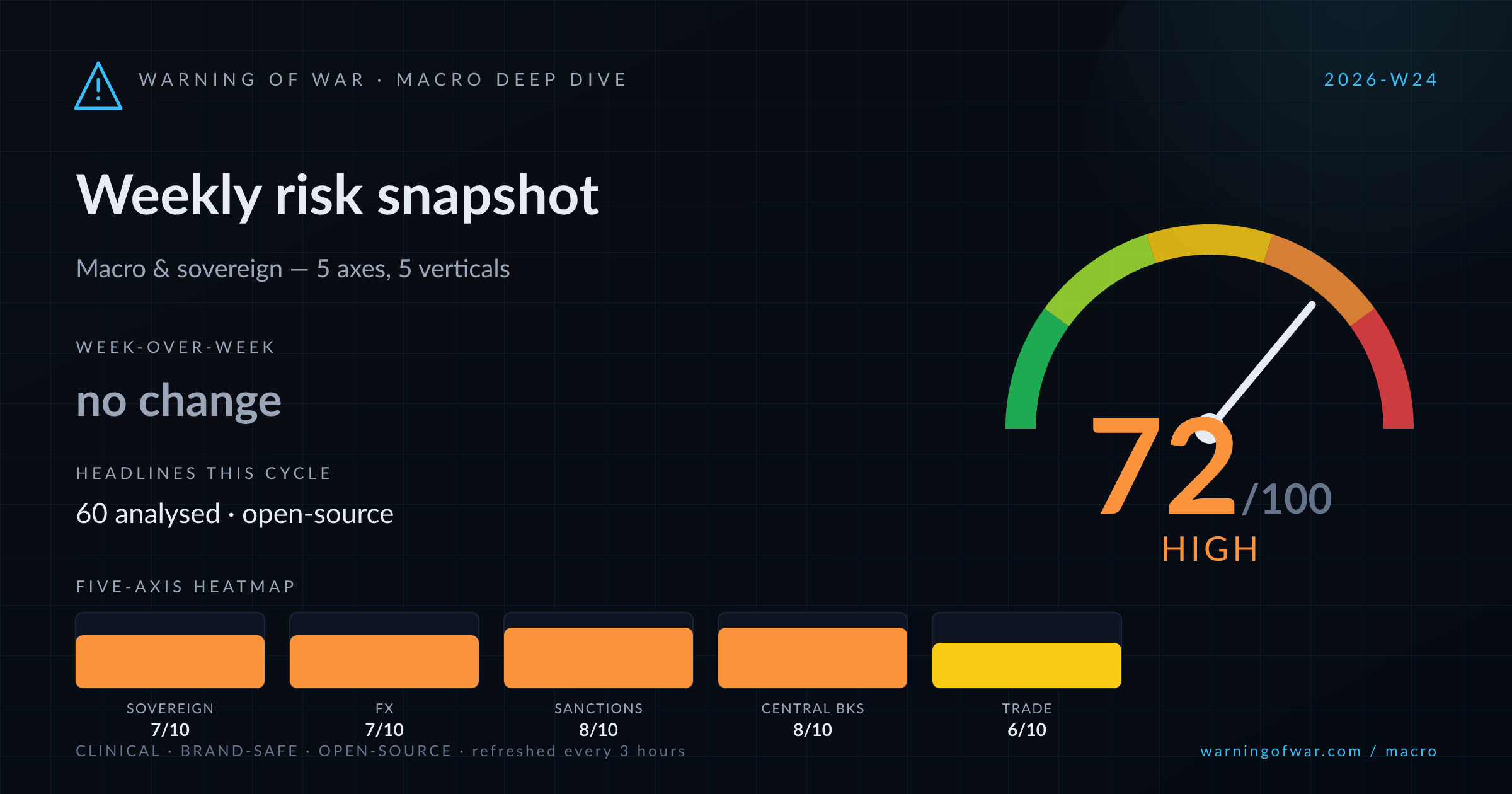

72/100 · High — no change WoW.

Global macro risk is materially elevated this cycle. Fitch has revised its 2026 global sovereign outlook to "Deteriorating," citing geopolitical-linked inflation spillovers. The ECB is pricing an insurance rate hike as energy-price pressures broaden across the euro zone. The Bank of Japan faces acute governance uncertainty following Governor Ueda's hospitalization ahead of the June policy meeting. The EU's 21st Russia sanctions package targets cryptocurrency platforms in Georgia and Russian cod imports, while the US has sanctioned 13 Iran-Belarus-China entities supplying the IRGC. Iran's Strait of Hormuz closure announcement compounds oil supply and sovereign-spread risk across multiple emerging-market corridors.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Sovereign Credit & Default | 7/10 | High | ▲ +1 |

| FX & Currency | 7/10 | High | ▼ -1 |

| Sanctions & Capital Flows | 8/10 | High | ▲ +1 |

| Central Bank Policy | 8/10 | High | ▲ +1 |

| Trade & BoP | 6/10 | Elevated | ▼ -2 |

(no prior week)

Fitch's downgrade of its 2026 global sovereign outlook to 'Deteriorating' — explicitly linking the revision to the Iran conflict's inflationary impact — sets a negative tone for sovereign credit broadly. Indonesia faces World Bank-flagged GDP deceleration to 5% with rising fiscal pressures, driving a renewed bond market sell-off. Nigeria's 2026 IMF Article IV consultation is active, and Moody's B3 affirmation of UBA anchors the sub-investment-grade frontier banking sector. Zambia's $1.36 billion Eurobond tender offer represents a post-restructuring market re-engagement, while Buenos Aires City's Moody's upgrade to AAA signals isolated bright spots within the EM credit landscape.

Operational signals

Headlines this cycle

(no prior week)

The Japanese Yen is testing exchange-rate levels that previously triggered Bank of Japan FX intervention, with Governor Ueda's hospitalization compounding governance uncertainty and forward-guidance opacity ahead of the June BoJ meeting. The EUR/JPY cross is range-bound as ECB guidance and intervention fears cap directional moves. Sterling's near-term trajectory is externally driven, reflecting broader risk-off conditions. The South Korean Won saw a surge in volatility prompting government-level monitoring. The Nigerian Naira recorded its first depreciation of the current cycle. The Indian Rupee erased RBI-supported gains on renewed corporate dollar demand. The WSJ Dollar Index edged higher to 96.58.

Operational signals

Headlines this cycle

(no prior week)

The EU's 21st Russia sanctions package advances to cover Russian cryptocurrency platforms operating through Georgia and introduces a ban on Russian cod imports, while BIMCO has issued new Russia-tanker resale restriction clauses for ship sale-and-purchase agreements. Separately, the US designated 13 entities across Iran, Belarus, and China for IRGC supply-chain support. An EU court ruling that US OFAC SDN-list status alone is insufficient grounds to deny EU bank-account access creates a compliance bifurcation between US and EU sanctions regimes. The US also sought to drop the Iran-related sanctions case against Turkish lender Halkbank. China's Hengli is redirecting crude procurement to West African and Middle Eastern suppliers following prior sanctions exposure.

Operational signals

Headlines this cycle

(no prior week)

The ECB is advancing toward an 'insurance hike,' citing Iran-conflict-linked euro zone inflation as the primary driver, with peace-process developments providing partial offset. The Bank of Japan faces an acute governance void after Governor Ueda's hospitalization means he will miss the June policy meeting, injecting forward-guidance uncertainty at a moment when the yen is near intervention territory. US bond markets are repricing a 2026 Fed rate hike even after soft core CPI, with equity futures responding positively to the CPI print. Sri Lanka's Central Bank Governor has briefed parliament directly on monetary policy and exchange-rate developments, signaling heightened institutional transparency in a post-program environment. Gold's monetary-hedge demand outlook remains supported.

Operational signals

Headlines this cycle

(no prior week)

Iran's announced closure of the Strait of Hormuz — the world's most critical oil chokepoint — directly threatens global energy trade flows and sovereign BoP positions for oil-importing emerging markets. The US has simultaneously affirmed its status as the world's leading oil exporter, repositioning its trade and current-account dynamics. China's cancellation of high-level EU meetings introduces trade-relationship uncertainty at a sensitive moment for EU-China economic ties. SLB's deal with Venezuela's PDVSA for AI-enabled sector modernization signals tentative FDI activity in a sanctioned-economy context. The AIIB's USD 200 million financing commitment for Philippine reforms supports BoP resilience in Southeast Asia.

Operational signals

Headlines this cycle

No named disruption events reported in this cycle.

Outlook pending next cycle.