Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

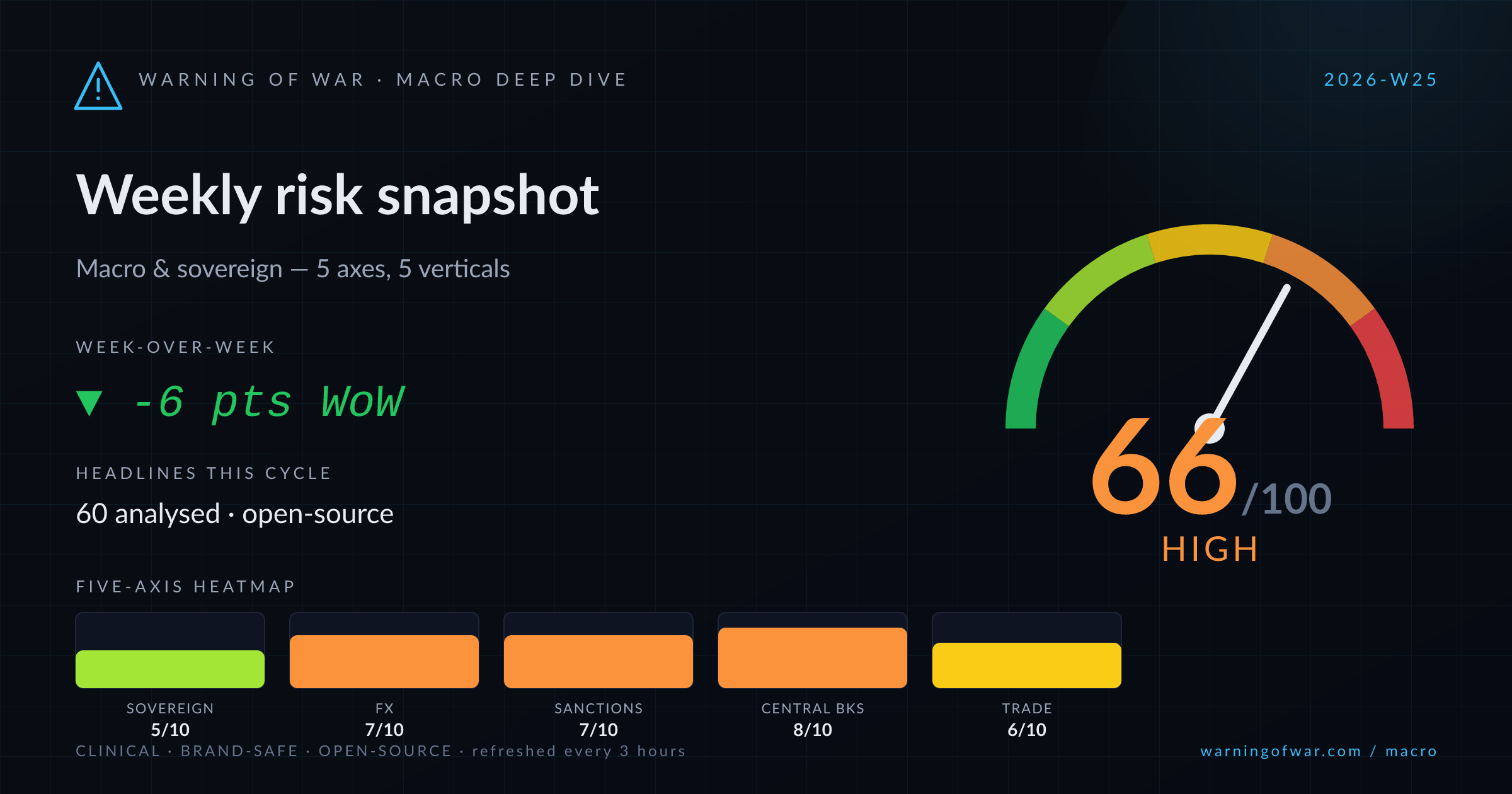

66/100 · High — -6 pts WoW.

Global macro conditions are shaped this cycle by three dominant forces: the Kevin Warsh-led Federal Reserve signalling a hawkish rate-hike trajectory, injecting significant uncertainty into G10 and EM rate expectations; a US–Iran diplomatic agreement altering Strait of Hormuz supply-route calculus and affecting oil-linked sovereign fiscal positions; and an active multi-jurisdictional sanctions environment featuring the UK's 21st Russia package, OFAC enforcement against Cuba-linked JVs, and Bulgarian resistance to EU restrictive measures. Fitch's sovereign upgrade of South Africa — with a pass-through to Eskom — and the IMF's fifth Jordan programme review provide counterbalancing positive sovereign signals. PBOC bond-market expansion and Bank of Korea FX repatriation guidance add EM monetary complexity.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Sovereign Credit & Default | 5/10 | Guarded | ▼ -2 |

| FX & Currency | 7/10 | High | → no change |

| Sanctions & Capital Flows | 7/10 | High | ▼ -1 |

| Central Bank Policy | 8/10 | High | → no change |

| Trade & BoP | 6/10 | Elevated | → no change |

▼ -2 WoW

The sovereign-credit landscape this cycle presents a bifurcated picture. On the constructive side, Fitch's upgrade of South Africa's sovereign rating — with a direct pass-through to Eskom's credit profile — signals improving fiscal credibility in sub-Saharan Africa's largest economy. Gabon's issuance of a $1.5 billion Eurobond marks a meaningful re-entry to international capital markets for a frontier sovereign. The IMF's fifth review of Jordan's reform programme, unlocking $188 million in financing, affirms programme compliance. Offsetting these improvements, the World Bank flags Iraq's heavy commodity-revenue dependence as a structural vulnerability, while Nigeria's federal government publicly rebuffs IMF fiscal-reform recommendations on fuel and telecom taxation.

Operational signals

Headlines this cycle

→ no change

The hawkish pivot from the new Federal Reserve under Chairman Warsh is the dominant FX catalyst this cycle, driving USD appreciation across G10 and EM pairs. The Korean won weakened 13.7 won against the dollar on rate-hike expectations, prompting the Bank of Korea to explicitly link won depreciation to outbound equity investment flows and to advocate for repatriation of overseas income as a stabilisation tool. The Swiss National Bank, through Governor Schlegel, has signalled readiness for FX intervention should the safe-haven CHF appreciate excessively. The Nigerian naira–dollar rate continues to attract domestic policy attention amid IMF engagement. The US–Iran diplomatic agreement provided a transient safe-haven unwind, with Treasury yields and the dollar briefly retreating before re-strengthening on Fed signals.

Operational signals

Headlines this cycle

▼ -1 WoW

Sanctions and capital-flow risk is elevated across multiple jurisdictions. The UK has expanded enforcement against Russia-linked financial networks, including a newly designated Nigeria-linked entity — adding a cross-jurisdictional compliance dimension for Africa-focused financial institutions. OFAC's Cuba sanctions have frozen Antilles Gold's JV, illustrating the capital-allocation risk for extractive-sector investors operating in OFAC-listed jurisdictions. The expiry of the US sanctions waiver on Russian oil creates material supply-chain and pricing uncertainty for buyers and intermediaries. Separately, Bulgaria's sustained opposition to components of the EU's 21st Russia sanctions package represents an intra-EU cohesion risk with implications for the package's ultimate enforcement perimeter. Iran diplomatic engagement introduces potential future sanctions-relief variables.

Operational signals

Headlines this cycle

→ no change

Central bank policy is the highest-conviction macro signal this cycle. Incoming Federal Reserve Chairman Kevin Warsh's debut has been interpreted by markets as a structurally hawkish recalibration: his inflation-hawk positioning, restructuring of internal working groups, and withholding of dot-plot submissions signal a departure from the prior forward-guidance framework, increasing rate-path uncertainty for fixed-income and EM positioning. The Philippine central bank's independent rate hike to address above-target inflation demonstrates EM monetary tightening pressure beyond the Fed cycle. The PBOC's strategic tilt from loan-based to bond-based monetary transmission broadens its easing toolkit. The SNB retains conditional FX intervention language. The Bank of Korea is navigating the intersection of Fed-driven external pressure and domestic investment outflows.

Operational signals

Headlines this cycle

→ no change

Trade and balance-of-payments dynamics this cycle are anchored to the US–Iran agreement and its oil-market implications. The prospect of a rapid Strait of Hormuz reopening and Iranian supply restoration is driving oil-price declines, which will exert negative fiscal and current-account pressure on commodity-dependent sovereigns including Iraq, Nigeria, and Gabon. European automakers — flagged by BMW — face mounting margin compression from Chinese competitive pressure, a structural trade-balance headwind for the EU. India's government is tapping World Bank and ADB facilities amid West Asia-related infrastructure spending constraints, signalling BoP financing pressure. The G7 gathering introduces a multilateral coordination backdrop for trade-policy signalling. Sri Lanka's IMF-backed recovery trajectory offers a frontier-market trade-stabilisation reference point.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| Warsh Fed Hawkish Recalibration | central-banks-policy | ACTIVE | Incoming Federal Reserve Chairman Kevin Warsh's debut signals a structurally hawkish monetary policy shift — withholding dot-plot guidance and restructuring internal working groups — materially raising rate-hike expectations and EM capital-flow volatility. |

| US–Iran Diplomatic Agreement | sanctions-capital-flows | ACTIVE | A US–Iran diplomatic agreement has been signed, triggering a Strait of Hormuz supply-route normalisation outlook, driving oil-price declines and creating potential future sanctions-relief variables for Iranian sovereign and energy-sector assets. |

| EU Russia Sanctions Package 21 — Bulgarian Resistance | sanctions-capital-flows | ACTIVE | Bulgaria's sustained opposition to specific provisions of the EU's 21st Russia sanctions package — notably over Patriarch Kirill-related designations — is creating intra-EU enforcement cohesion risk and delaying the package's full implementation perimeter. |

| UK Russia-Network Sanctions Expansion | sanctions-capital-flows | RISING | The UK has expanded its Russia-network sanctions enforcement with the designation of a Nigeria-linked entity, extending cross-jurisdictional compliance exposure for African-corridor financial institutions and correspondent banks. |

| Korean Won Depreciation Pressure | fx-currency | ACTIVE | The Korean won is under material depreciation pressure driven by Fed rate-hike expectations and structural outbound equity investment flows, with the Bank of Korea formally urging capital repatriation as a stabilisation mechanism. |

| Fitch South Africa Sovereign Upgrade | sovereign-credit | STABLE | Fitch Ratings has upgraded South Africa's sovereign credit rating, with a direct positive pass-through to Eskom's credit profile, marking an improvement in the country's fiscal credibility trajectory under the current administration. |

Over the 60–90 day forward window, the dominant macro pressure vector is the Federal Reserve's policy-path uncertainty under Chairman Warsh: markets should anticipate continued USD strength, elevated US Treasury yield volatility, and sustained EM capital-flow headwinds — particularly for KRW, NGN, and other current-account-deficit currencies. The US–Iran agreement, if it progresses toward sanctions relief and full Strait of Hormuz normalisation, will suppress oil prices further, compressing fiscal revenues for commodity-dependent sovereigns including Iraq, Nigeria, and Gabon — partially offsetting Gabon's positive Eurobond re-entry signal. The EU's 21st Russia sanctions package remains at risk of delayed or partial implementation pending Bulgarian consensus resolution; compliance desks should monitor the intra-EU negotiation timeline closely. OFAC enforcement activity — as evidenced by the Cuba JV freeze and Russian-oil waiver expiry — suggests a sustained extraterritorial enforcement posture. The PBOC's bond-market pivot and Philippine BSP rate hike signal divergent EM monetary conditions that will affect regional fixed-income allocations. Sovereign-credit analysts should monitor Nigeria's IMF engagement trajectory, Sri Lanka's IMF programme milestone delivery, and the World Bank's Iraq fiscal-diversification assessments as leading indicators of EM sovereign stress or resilience.