Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

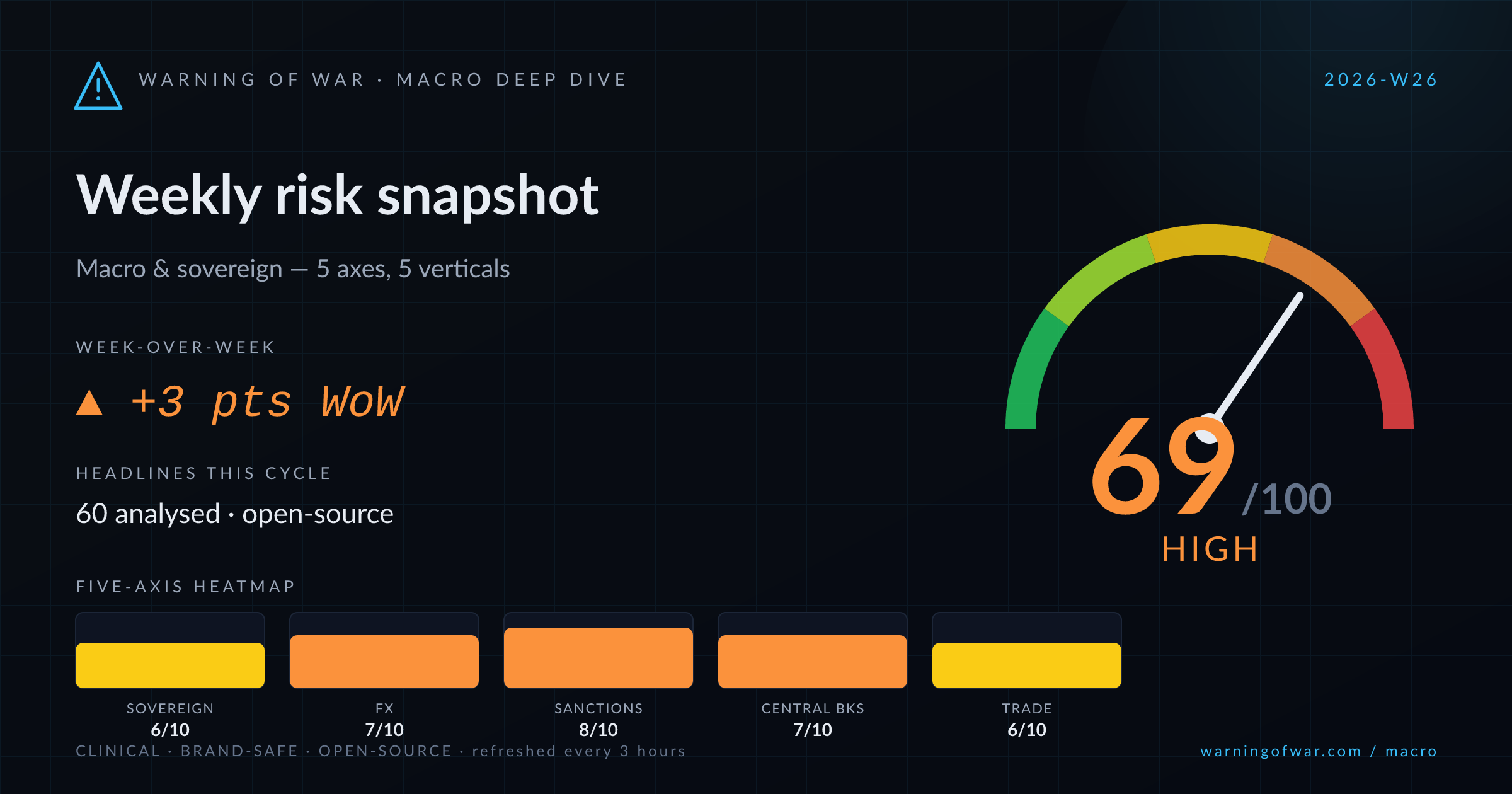

69/100 · High — +3 pts WoW.

Global macro conditions are materially elevated across multiple axes this cycle. The Federal Reserve faces rate-path uncertainty as 2-year Treasury yields signal possible tightening, while the Bank of Japan's Tamura advocates incremental rate hikes and the ECB contends with weak German data. OFAC's partial authorisation of Iran crude transactions—with EU and OFSI sanctions remaining in force—creates layered compliance divergence. The Korean won has breached post-financial-crisis highs against the dollar, Libya's central bank deployed a $6 billion dinar stabilisation intervention, and China is marketing a record €5 billion sovereign Eurobond. Moody's cut Gabon's outlook to negative, and Bangladesh and an unnamed sovereign have approached the IMF for fresh programme support.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Sovereign Credit & Default | 6/10 | Elevated | ▲ +1 |

| FX & Currency | 7/10 | High | → no change |

| Sanctions & Capital Flows | 8/10 | High | ▲ +1 |

| Central Bank Policy | 7/10 | High | ▼ -1 |

| Trade & BoP | 6/10 | Elevated | → no change |

▲ +1 WoW

Moody's has revised Gabon's outlook to negative, citing rising debt risk—a signal of widening spreads for sub-Saharan frontier credits. Bangladesh has approached the IMF for a fresh loan while the World Bank simultaneously extends a $450 million banking-reform facility, indicating overlapping multilateral engagement. Brazil is planning its largest-ever panda bond issuance to diversify sovereign funding into CNY markets, a structurally significant capital-market development. China's marketing of a record €5 billion sovereign Eurobond reinforces its effort to diversify reserve currency exposure. The IMF's Article IV consultation for Switzerland and ongoing Nigeria IMF prescription discourse round out the cycle's sovereign-credit signals.

Operational signals

Headlines this cycle

→ no change

The Korean won has breached the 1,540 level against the dollar for a second consecutive session—the weakest reading since the global financial crisis—prompting acute investor caution and domestic retail-sector repricing. Libya's central bank executed a $6 billion foreign-exchange injection to arrest dinar depreciation pressure. The naira's daily exchange-rate reporting reflects persistent NGN volatility. The dollar-yen rate is stalling on mixed BOJ signalling, with market participants withdrawing momentum exposure. Costa Rica's colón may be stabilising at a floor, while the euro is softening against the yen on weak German data and ECB caucus tension. Vietnam's reference rate is trending upward. The dollar is holding steady ahead of key US inflation data.

Operational signals

Headlines this cycle

▲ +1 WoW

OFAC has issued authorisation for certain Iran crude oil and petroleum product transactions, but EU and OFSI sanctions remain fully operative, creating a tripartite regulatory divergence that imposes complex compliance obligations on energy traders, tanker operators, and correspondent banks. Concurrently, the WSJ reports a crypto exchange serving as a conduit for illicit Iranian capital flows, a vector now directly within OFAC's enforcement lens. The US has removed sanctions on seven Russian nationals, two Turkish companies, and two vessels—a calibrated easing with geopolitical linkage. OFAC has also designated ISIS crypto-financing operators under its SDN regime. ICC judges have filed suit against the US administration over sanctions listings, escalating institutional friction. The UK is entering a new enforcement era for its own sanctions regime.

Operational signals

Headlines this cycle

▼ -1 WoW

The US 2-year Treasury yield is signalling potential Fed rate hike optionality, complicating the consensus rate-cut narrative and tightening financial conditions for EM sovereigns. The BOJ's board member Tamura has explicitly called for rate increases every few months, while a Japanese government blueprint is simultaneously nudging the BOJ toward demand stimulus—clouding the rates path further. Japan's 20-year bond auction recorded its lowest demand since May 2025, a fiscal-funding stress indicator. The PBOC is advancing overnight reverse repo operations as the next stage of its policy shift. The Federal Reserve's balance sheet has risen to $6.74 trillion. Australia's labour market strength keeps RBA hike risk live. The NY Fed has played down new FOMC reserve-system language.

Operational signals

Headlines this cycle

→ no change

The reopening of the Strait of Hormuz is flooding global oil markets with supply, pushing prices back to pre-escalation levels and materially altering the terms of trade for Gulf-dependent sovereigns and commodity-indexed debt. US-Iran talks are making headway, contributing to oil-futures retreat and creating optionality for further OFAC sanction relief on Iranian petroleum—a shift with major BoP implications for Iran and ripple effects on competing oil exporters. A $35 billion US missile-defense procurement and a Turkish arms-sale dispute between the Trump administration and Congress introduce defence-industrial trade tensions. Brazil's panda bond and China's Eurobond issuance also signal bilateral capital-market trade-flow diversification away from USD-denominated channels. The World Bank has raised India's growth forecast to 6.6%, reinforcing South Asia's relative BoP resilience.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| OFAC Iran Crude Partial Authorisation | sanctions-capital-flows | ACTIVE | OFAC has authorised certain Iran crude oil and petroleum product transactions, while EU and OFSI sanctions remain fully operative, creating a tripartite compliance divergence that directly affects energy traders, tanker operators, and correspondent banks. |

| Korean Won Post-Financial-Crisis Depreciation | fx-currency | ACTIVE | The Korean won has weakened to the 1,540 per dollar range for a second consecutive session, reaching its softest level since the global financial crisis and prompting heightened caution among institutional FX participants. |

| BOJ Rate-Path Divergence vs. Government Blueprint | central-banks-policy | RISING | BOJ board member Tamura's public call for rate hikes every few months is in direct tension with a Japanese government policy blueprint urging the central bank to support domestic demand, materially clouding the rates-path outlook and suppressing JGB auction demand. |

| Gabon Sovereign Outlook Cut to Negative | sovereign-credit | ACTIVE | Moody's has revised Gabon's sovereign credit outlook to negative, citing rising debt risk and signalling potential spread widening for sub-Saharan frontier-market credits in the near term. |

| Hormuz Reopening Oil Supply Normalisation | trade-policy | EASING | The reopening of the Strait of Hormuz is rapidly restoring Gulf oil supply flows, driving oil futures back to pre-escalation price levels and materially altering the terms of trade and BoP trajectories for Gulf sovereign exporters and energy-importing EMs. |

| Libya Central Bank FX Stabilisation Intervention | fx-currency | ACTIVE | The Central Bank of Libya has injected $6 billion into the foreign-exchange market to arrest dinar depreciation, representing a large-scale unilateral FX stabilisation operation with implications for Libya's reserve adequacy and sovereign external balance. |

Over the next 60–90 days, the most consequential pressure points are the Federal Reserve's rate-path optionality and the BOJ's policy ambiguity, both of which will drive volatility in USD/JPY, Korean won, and broader EM FX crosses. If the Fed's 2-year yield signal materialises into explicit hawkish forward guidance, EM sovereigns with high external-debt rollover needs—including Bangladesh and sub-Saharan frontier credits such as Gabon—face widening spreads and constrained Eurobond access. The OFAC partial Iran crude authorisation will be closely monitored by EU and UK compliance functions; any broadening of waivers risks secondary-sanctions friction for European energy majors. China's €5 billion Eurobond and Brazil's panda bond issuance mark an accelerating structural shift in sovereign funding away from USD channels, a trend that will attract further CFIUS and EU FDI-screening scrutiny. The Hormuz supply normalisation is disinflationary for oil-importing EMs but deflationary for Gulf sovereign revenue; Saudi Aramco and ADNOC BoP trajectories will require reassessment. Japan's deteriorating JGB auction demand, if sustained, may force the MOF to offer concessions that complicate the BOJ's balance-sheet normalisation. Sanctions compliance teams should prepare for expanded OFAC enforcement in the crypto-Iranian financing nexus and escalating UK OFSI enforcement activity under its new regime.