Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

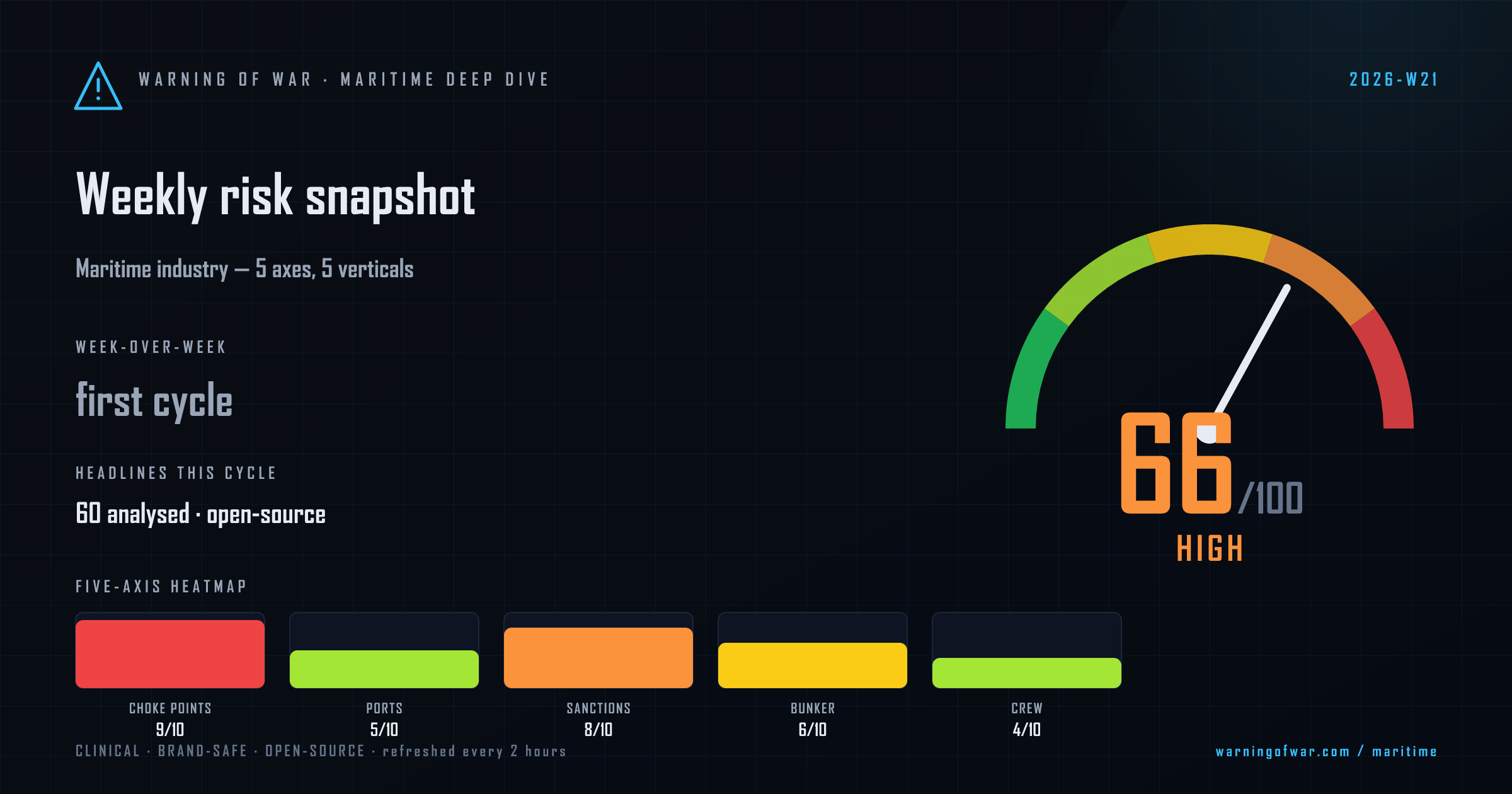

66/100 · High — first weekly snapshot.

The Strait of Hormuz dominates this scoring cycle as the single most consequential commercial-risk vector in global shipping. Iran's newly established Persian Gulf Strait Authority (PGSA) has formalised a state-administered transit-toll regime, with per-voyage fees reported at up to USD 2 million settled in CNY and Bitcoin. Three VLCCs detained for over two months have begun exiting the strait, and Iran claims to have coordinated passage of 26 vessels in a single 24-hour window. U.S. naval forces have boarded multiple Iranian-flagged tankers, sustaining elevated war-risk premiums across the Persian Gulf corridor. Tanker resale premiums are soaring as owners accelerate delivery timelines. VLGC spot rates have reached USD 6 million per month on scarce availability. On dry-bulk, the Baltic Dry Index recorded a fourth consecutive decline. ARA bunker fuel terminals report loading delays that have stretched lead times to approximately 10 days. The UAE's Hormuz-bypass crude pipeline reached 50% completion. Indonesia has imposed new commodity export controls, adding compliance complexity for dry-bulk and container operators across Southeast Asian trade lanes.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Choke Point Stress | 9/10 | Critical | · — |

| Port Congestion | 5/10 | Guarded | · — |

| Sanctions & Compliance | 8/10 | High | · — |

| Bunker Volatility | 6/10 | Elevated | · — |

| Crew & Labour | 4/10 | Guarded | · — |

(no prior week)

The tanker segment is operating under critical stress centred on the Strait of Hormuz. Iran's PGSA has imposed a formalised per-transit fee structure, with three VLCCs carrying approximately 6 million barrels exiting after an extended detention period. A South Korean tanker became the first to exit fee-free in 81 days under diplomatic coordination. VLGC spot rates have reached USD 6 million per month amid scarce vessel availability. Tanker resale premiums are rising sharply as owners chase faster delivery to capitalise on elevated freight returns. U.S. naval boardings of Iranian-flagged vessels sustain war-risk insurance premium pressure across the Persian Gulf. ADNOC's Hormuz-bypass pipeline at 50% completion offers a medium-term partial relief valve for Gulf crude exports.

Operational signals

Headlines this cycle

(no prior week)

Dry-bulk markets face moderate headwinds this cycle. The Baltic Dry Index declined for a fourth consecutive session to 3,005 points — its lowest since mid-May — with Capesize rates under particular pressure. Bauxite trade flows are shifting materially: India is emerging as a key destination as Arabian Gulf risk rises, while UAE import volumes are reported 72% lower year-on-year for April 2026. Guinea supply-side constraints threaten to cap growth in China-bound bauxite flows despite a 26% year-on-year volume increase in April. Indonesia's new commodity export controls add documentation and compliance friction for dry-bulk operators serving Southeast Asian routes. INTERCARGO's new STS standard for dry bulk provides an operational framework as STS transfer volumes increase in constrained port environments.

Operational signals

Headlines this cycle

(no prior week)

Container operators face high commercial pressure on Asia-Europe corridors. Ongoing Cape of Good Hope diversions — driven by Middle East corridor instability — are producing significant total-landed-cost uncertainty, with freight forwarders increasingly settling final bills in transit rather than at booking. The continuation of Hormuz disruption has compounded supply-chain risk modelling for corporates with Persian Gulf export exposure. South Korea's tentative selection of a small container line for an Arctic test voyage signals early-stage route diversification interest. ARA bunker loading delays of up to 10 days add cost unpredictability for Europe-calling boxship operators. Digital port infrastructure and Port Community Systems are gaining strategic prioritisation as operators seek real-time visibility tools to manage re-routing complexity.

Operational signals

Headlines this cycle

(no prior week)

The offshore segment presents a mixed picture. OSV ordering remains structurally subdued despite oil prices elevated by Hormuz-driven supply uncertainty — a structural legacy of the 2015–2020 cycle downturn continues to suppress speculative ordering. Crew transfer vessel (CTV) construction for offshore wind is advancing, with Strategic Marine securing a repeat order for its largest Supa Swath vessels to date from Mainprize Offshore, signalling continued CTV fleet investment. Golar LNG's Q1 2026 results show robust FLNG performance — USD 106 million adjusted EBITDA, with the Hilli unit recording its 150th cargo offload. DLR's keel-laying of the Modularis research platform at FSG Flensburg reflects incremental investment in maritime technology infrastructure. Arctic barge operations for Agnico Eagle's Hope Bay Mine represent an emerging niche offshore logistics corridor.

Operational signals

Headlines this cycle

(no prior week)

The yacht and leisure segment registers low stress this cycle with no direct disruption signals from the supplied headline set. Belfast's announcement of a USD 1.75 billion 25-year port growth plan provides a positive long-horizon infrastructure signal for the leisure and superyacht berth market in Northern Europe. Piraeus Port's strategic growth narrative — bridging Europe, Middle East, and Africa — offers a constructive medium-term outlook for Mediterranean leisure traffic. The broader Hormuz disruption does not directly affect leisure routing at this stage, though elevated fuel costs from ARA terminal delays and VLSFO supply tightness could translate into modestly higher marina and charter operating costs in European waters.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| Iran PGSA Hormuz Transit-Toll Regime | tanker | ACTIVE | Iran's newly established Persian Gulf Strait Authority has formalised a state-administered per-transit fee structure of up to USD 2 million per voyage, settled in CNY and Bitcoin, with bilateral carve-outs for select flag states — fundamentally altering the commercial calculus for all vessels transiting the Strait of Hormuz. |

| VLCC Hormuz Detention & Release | tanker | EASING | Three VLCCs carrying approximately 6 million barrels of Middle East crude were detained in the Persian Gulf for over two months before commencing southbound Hormuz transit, with a South Korean tanker completing the first fee-free exit in 81 days under diplomatic coordination. |

| US Naval Boarding of Iranian-Flagged Tankers | tanker | ACTIVE | U.S. naval forces have conducted multiple boardings of Iranian-flagged oil tankers suspected of circumventing enforcement measures, sustaining elevated war-risk insurance premiums across Persian Gulf tanker routing. |

| ARA Bunker Terminal Loading Delays | container | RISING | Bunker fuel loading lead times at ARA hub terminals have approximately doubled to 10 days, tightening VLSFO supply availability and adding cost and scheduling uncertainty for vessel operators bunkering in Northwest Europe. |

| Baltic Dry Index Four-Session Decline | dry-bulk | RISING | The Baltic Dry Index fell for a fourth consecutive session to 3,005 points — its lowest level since mid-May 2026 — with Capesize softness leading the decline amid shifting bauxite trade flows and Indonesia export-control headwinds. |

| Asia-Europe Container Freight Cost Volatility | container | ACTIVE | Persistent Cape of Good Hope rerouting driven by Middle East corridor instability is generating material total-landed-cost uncertainty on Asia-Europe lanes, with freight forwarders increasingly unable to lock in final costs at the point of booking. |

Outlook pending next cycle.