Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

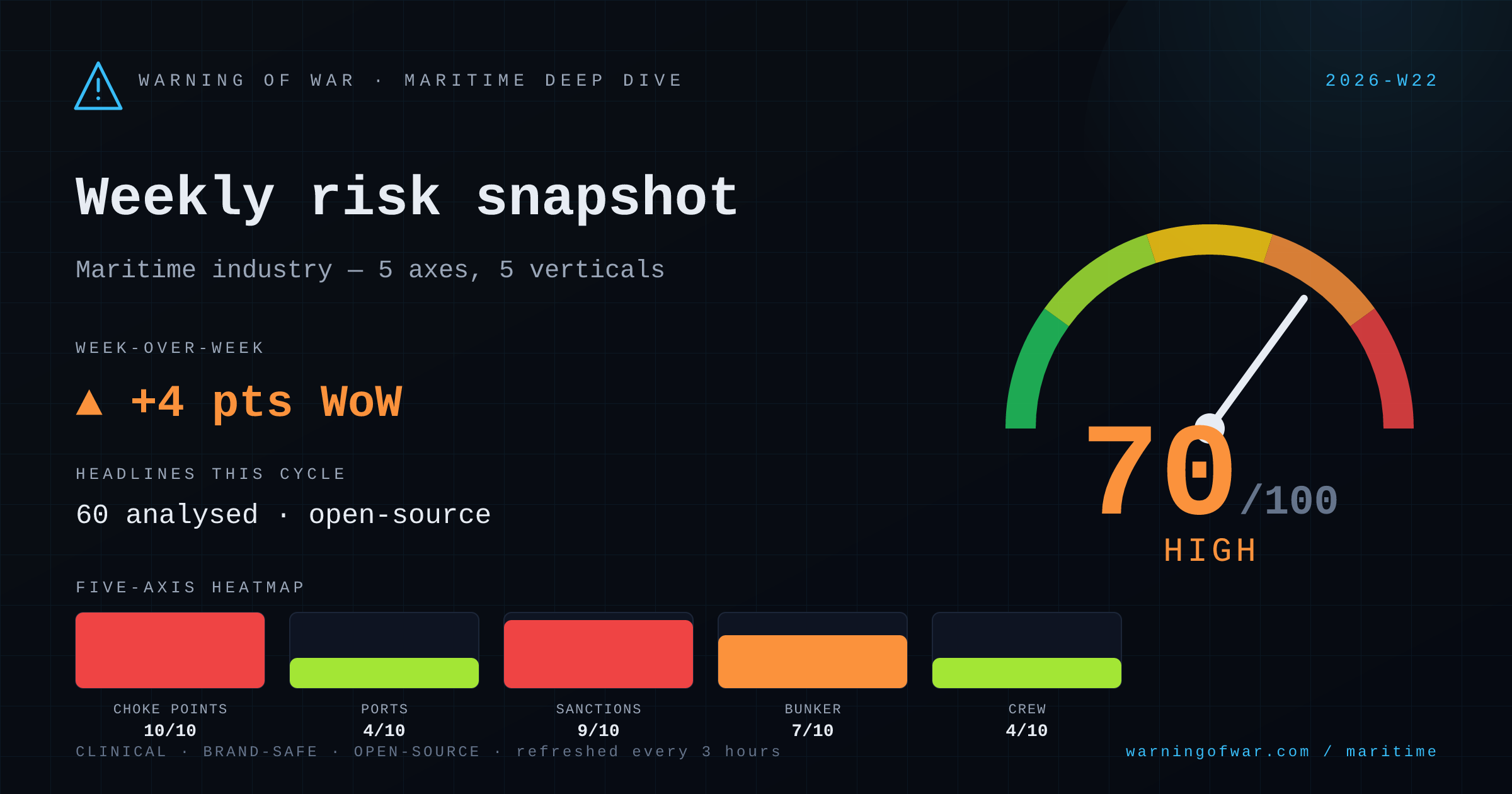

70/100 · High — +4 pts WoW.

The Strait of Hormuz has entered a period of severe commercial disruption. U.S. Treasury has sanctioned Iran's Persian Gulf Strait Authority (PGSA), and multiple U.S. military strikes on Iranian military infrastructure near Hormuz have followed IRGC interdiction of commercial vessels, including a documented halt of a U.S.-flagged tanker. Flexport and ICIS confirm Hormuz transit remains severely disrupted, with at least three oil and LNG tankers exiting with AIS transponders off. Oil prices have surged materially. The shadow-fleet sanctions landscape is tightening, with GMS receiving U.S. approval to recycle sanctioned container tonnage. Rotterdam's first ethanol bunkering and PIL's inaugural Shanghai LNG bunkering trial mark incremental alternative-fuel milestones.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Choke Point Stress | 10/10 | Critical | ▲ +1 |

| Port Congestion | 4/10 | Guarded | ▼ -1 |

| Sanctions & Compliance | 9/10 | Critical | ▲ +1 |

| Bunker Volatility | 7/10 | High | ▲ +1 |

| Crew & Labour | 4/10 | Guarded | → no change |

▲ +1 WoW

The Strait of Hormuz, through which approximately 20% of global oil and LNG flows, is severely disrupted following IRGC interdiction of commercial vessels, U.S. strikes on Iranian drone and missile infrastructure, and PGSA sanctions. At least three oil and LNG tankers have transited with transponders off. A Korean-flagged vessel sustained an Iranian anti-ship missile strike. U.S. Strategic Petroleum Reserve crude is being rerouted to California, underscoring the redrawing of Middle East trade flows. War-risk insurance premiums for Hormuz-transiting tonnage are at exceptional levels.

Operational signals

Headlines this cycle

→ no change

Direct Hormuz exposure for dry-bulk is lower than tanker, but secondary effects via elevated bunker costs and altered routing around the Arabian Gulf are commercially material. The ongoing Diana Shipping bid for Genco Shipping signals sector M&A activity and potential fleet restructuring pressure. Ship recycling markets remain soft, limiting fleet capacity reduction. Commodity demand signals from the broader Iran conflict impact are yet to fully price into Capesize and Panamax rates.

Operational signals

Headlines this cycle

→ no change

Box carriers transiting the Arabian Gulf or calling at Gulf ports face acute schedule unreliability from Hormuz disruption. U.S. approval for GMS to scrap four sanctioned Iranian-linked container ships signals active enforcement of OFAC measures against shadow-fleet tonnage. PIL's LNG bunkering trial in Shanghai's Waigaoqiao Port and Rotterdam's inaugural ethanol bunkering on Eco Levant (X-Press Feeders) mark operational alternative-fuel milestones relevant to container operators managing decarbonisation compliance.

Operational signals

Headlines this cycle

▲ +1 WoW

Arabian Gulf FPSO and OSV operators face direct commercial exposure from the Hormuz crisis, with vessel positioning and contractor mobilisation constrained by elevated war-risk premiums and IRGC interdiction risk. Outside the Gulf, offshore wind continues to attract capital: EDP Renováveis is rotating toward offshore wind assets, and Wärtsilä's 30% production capacity expansion signals strong OEM order backlogs. Floating nuclear power feasibility studies for Greek islands by 2035 represent a nascent but noted energy-infrastructure signal.

Operational signals

Headlines this cycle

▲ +1 WoW

The yacht-leisure and cruise sectors are not directly exposed to Hormuz transit, but elevated oil prices — crude up 3%+ on Iran escalation — translate into higher VLSFO and MGO bunker costs for large cruise vessels and superyachts. Oman and UAE remain popular superyacht wintering destinations; the deteriorating diplomatic environment around Gulf access may necessitate revised itinerary planning. Greek island floating nuclear feasibility studies are a longer-term infrastructure signal for Eastern Mediterranean leisure-port energy security.

Operational signals

Headlines this cycle

No named disruption events reported in this cycle.

Outlook pending next cycle.