Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

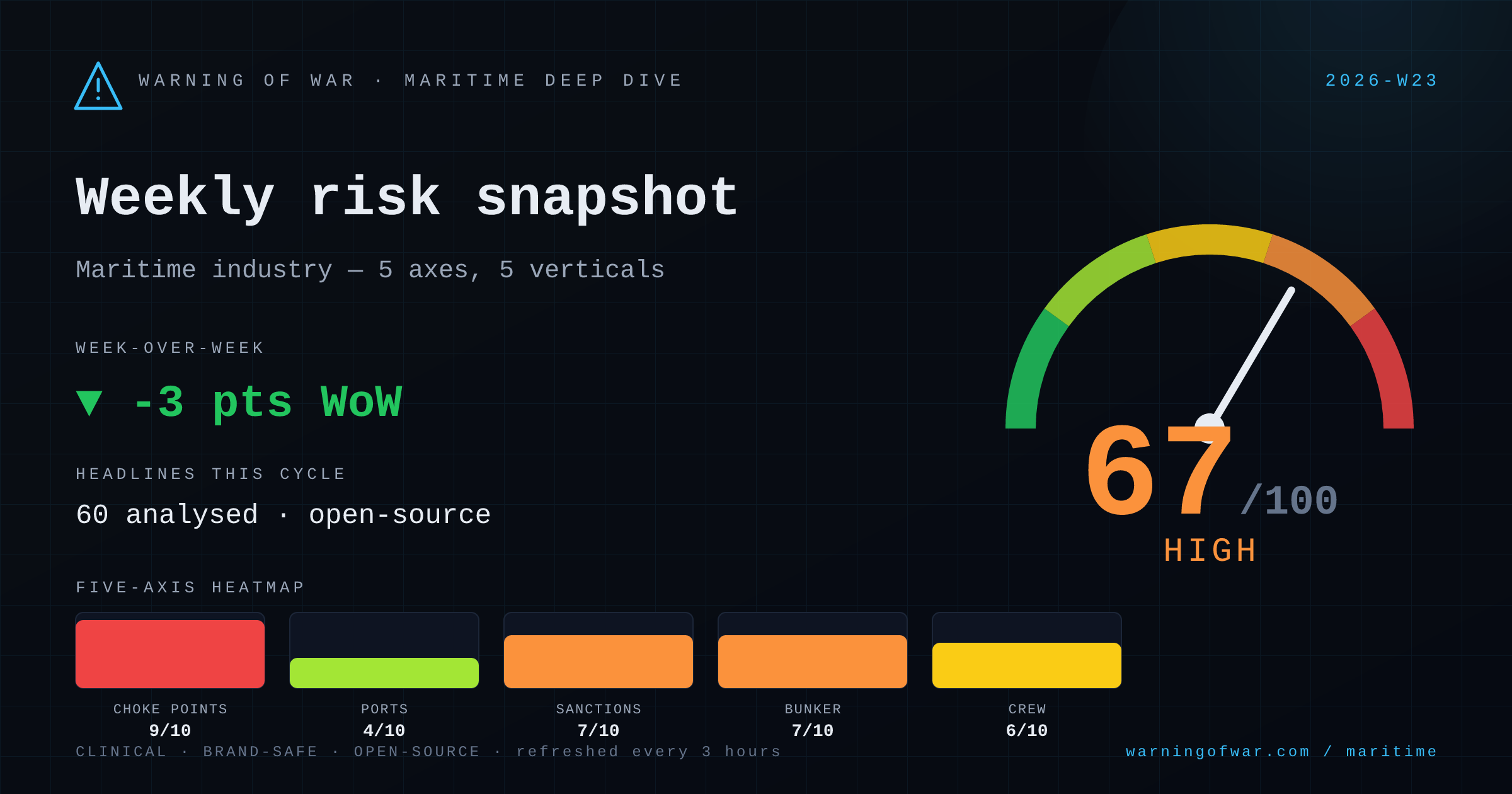

67/100 · High — -3 pts WoW.

The Strait of Hormuz remains the dominant commercial risk signal this cycle, with the waterway operating under active blockade conditions and transit access contingent on evolving U.S.-Iran diplomatic negotiations. War-risk insurance premiums on Persian Gulf routes are elevated; vessel rerouting costs are compounding freight-rate pressure across tanker and container segments. Shadow-fleet enforcement activity in the Atlantic adds sanctions-compliance friction. Bab-el-Mandeb re-escalation risk is flagged in open-source commentary. Container schedule reliability improved marginally to 62.4% in April 2026. Crew-change restrictions in the Gulf persist per IMO guidance. Bunker costs are rising on oil-price pressure and alternative-fuel transition activity.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Choke Point Stress | 9/10 | Critical | ▼ -1 |

| Port Congestion | 4/10 | Guarded | → no change |

| Sanctions & Compliance | 7/10 | High | ▼ -2 |

| Bunker Volatility | 7/10 | High | → no change |

| Crew & Labour | 6/10 | Elevated | ▲ +2 |

▼ -1 WoW

The active Strait of Hormuz blockade has immobilised a significant portion of the VLCC and Suezmax fleet in the Persian Gulf, with operators reporting vessels unable to exit following cargo discharge. Venezuelan crude export recovery (1.25 mb/d in May, third consecutive monthly rise) provides a marginal Atlantic Basin offset. MR product tanker and chemical tanker newbuilding orders continue at Chinese yards, indicating medium-term fleet growth expectations remain intact despite near-term disruption.

Operational signals

Headlines this cycle

→ no change

The Baltic Dry Index is under downward pressure from slipping Capesize rates, with no material port congestion or route disruption directly impacting the dry-bulk segment this cycle. Indian iron ore import demand is identified as a positive demand signal, supporting Supramax and Panamax utilisation on Pacific trade lanes. The Hormuz closure has minimal direct operational impact on dry-bulk given limited dry cargo exposure through the strait, but elevated bunker costs are compressing TCE returns fleet-wide.

Operational signals

Headlines this cycle

→ no change

Global container schedule reliability improved to 62.4% in April 2026, the highest level since the Red Sea disruption cycle began, yet remains well below the 80%+ pre-disruption benchmark. The MSC Panama-flagged containership sustaining structural damage in two separate incidents off Iraq introduces fresh route-risk pricing for Middle East Gulf box trades. Feeder and intra-Asia newbuilding orders (Baozhou 2,700 TEU vessels at Zhejiang yards) reflect continued capacity investment. Hapag-Lloyd's first dual-fuel methanol conversion signals fleet decarbonisation momentum.

Operational signals

Headlines this cycle

→ no change

The BPCL/Petrobras SEAP-I FPSO contract award in Brazil demonstrates continued deepwater development momentum in the Atlantic Basin. DEME secured an offshore wind installation contract in Japan, and Fugro secured a multi-year environmental monitoring role for Irish offshore wind projects, indicating a healthy forward project pipeline for construction and survey vessels. Gulf of Mexico shipyard infrastructure investment (Davie/Gulf Copper $1 billion Galveston-Port Arthur modernisation) strengthens the domestic OSV and USCG newbuild supply chain.

Operational signals

Headlines this cycle

→ no change

Carnival Corporation's expansion of LNG bunkering operations to Latin America — including the Carnival Jubilee inaugural LNG bunkering call at Roatán, Honduras — marks a meaningful decarbonisation step for cruise operators on Western Caribbean itineraries. Hormuz disruption and associated oil-price increases will feed through to marine fuel and charter costs for the leisure segment with a lag, but no direct operational restrictions on superyacht or cruise itineraries are evidenced in current headlines. The Cold Lake marina development note reflects local infrastructure activity only.

Operational signals

Headlines this cycle

No named disruption events reported in this cycle.

Outlook pending next cycle.