Tanker Markets

9/10Critical

Hormuz blockade conditions and IRGC-related EU sanctions are driving war-risk premium spikes and significant rerouting costs for crude, product, and LNG tankers.

WEEKLY REPORT · 2026-W24 · Jun 8 – Jun 14, 2026

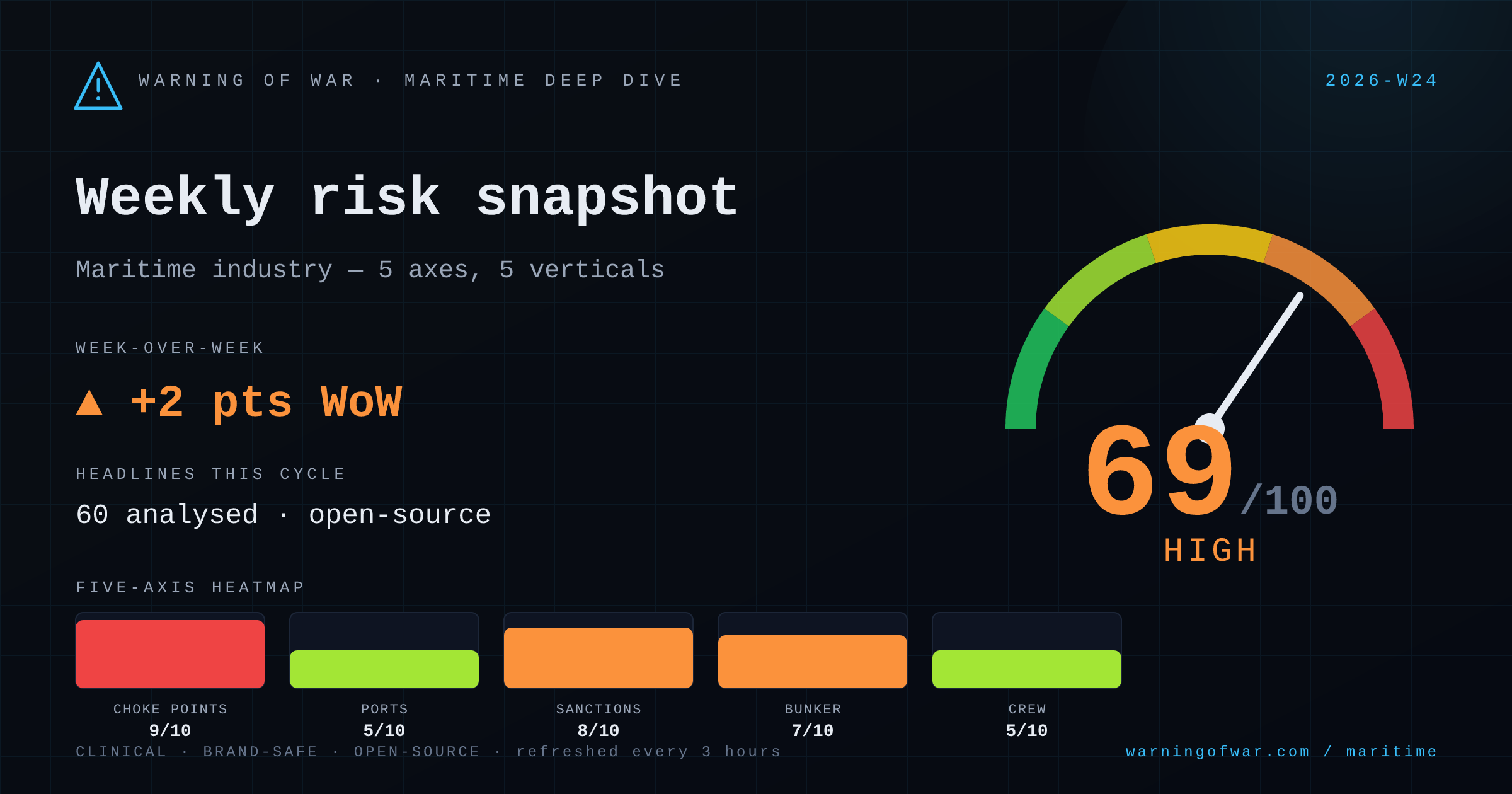

Weekly maritime industry risk snapshot — composite 69/100 (High), ◆ first weekly snapshot.

The Strait of Hormuz is the dominant commercial risk signal this cycle. Iran has signalled a conditional reopening with proposed transit fees; QatarEnergy-controlled LNG carriers are transiting, while ADNOC has tendered 14 million barrels under blockade conditions. EU sanctions on IRGC-linked entities have tightened compliance obligations across tanker and LNG operators. Houthi interdiction activity continues to suppress Bab-el-Mandeb / Red Sea traffic, sustaining rerouting via Cape of Good Hope and elevating war-risk premiums. Suez Canal steeper transit charges take effect mid-July. Singapore VLSFO pricing shows mixed signals. The VLCC orderbook has reached a record high amid the supply-route disruption environment.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

Critical

Hormuz blockade conditions and IRGC-related EU sanctions are driving war-risk premium spikes and significant rerouting costs for crude, product, and LNG tankers.

Elevated

Dry-bulk exposure to Hormuz and Red Sea disruption is indirect but material, with Cape-of-Good-Hope rerouting adding voyage days and bunker cost for grain and commodity trades.

High

Container freight rates are signalling a cyclical peak while the containership orderbook approaches 40%, and Suez Canal fee increases from mid-July add structural cost pressure.

High

European offshore wind survey activity is expanding with TGS securing multiple site-characterisation contracts, while Middle East geopolitical stress elevates operational risk for Gulf-based OSV and FPSO operators.

Elevated

Red Sea and Hormuz disruption is materially curtailing superyacht and cruise transit on the Egypt–Suez–Red Sea corridor, while Suez Canal fee increases and Houthi interdiction threats deter leisure routing.

No named disruption events reported in this cycle.

Outlook pending.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.