Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

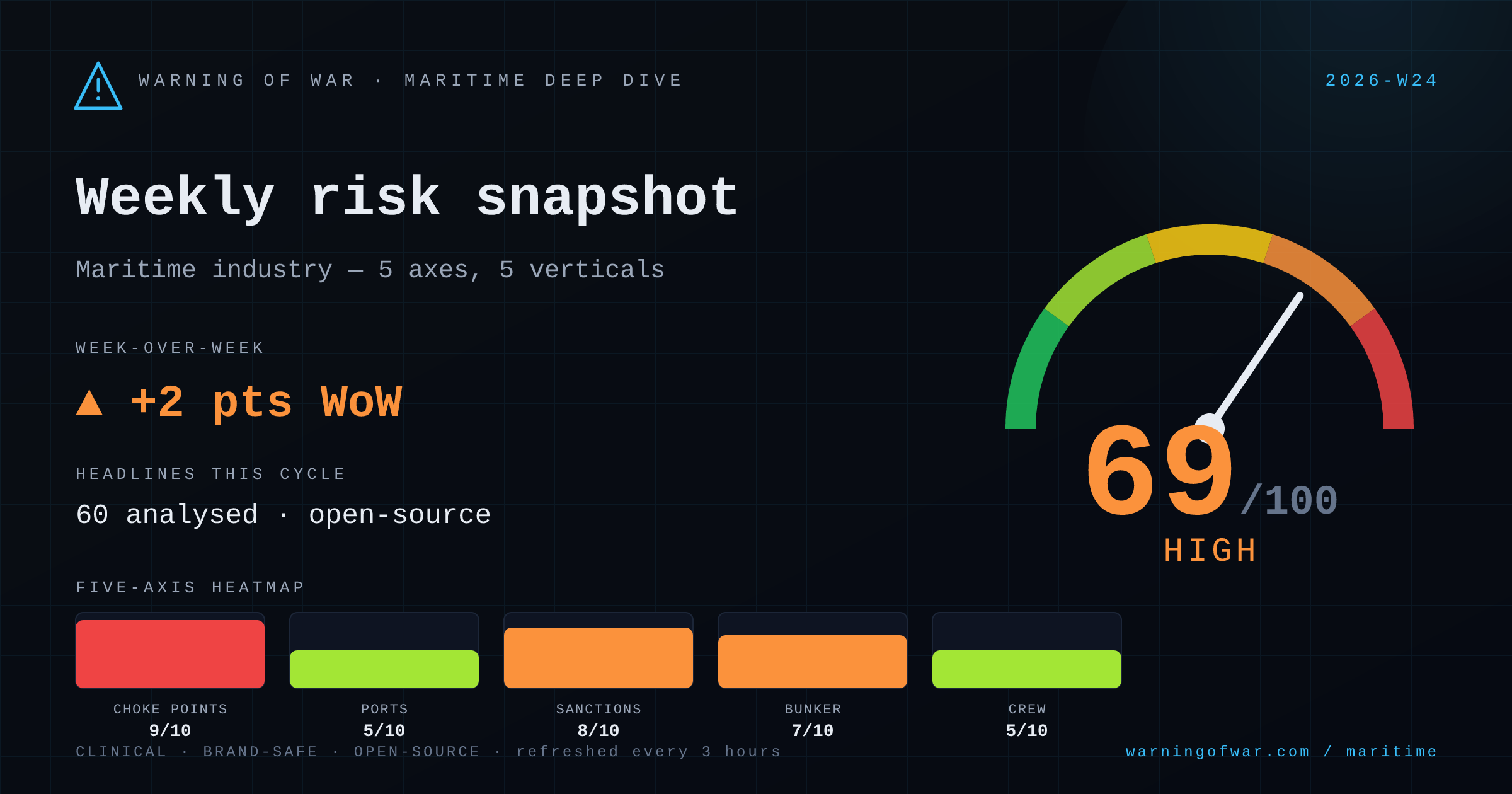

69/100 · High — +2 pts WoW.

The Strait of Hormuz is the dominant commercial risk signal this cycle. Iran has signalled a conditional reopening with proposed transit fees; QatarEnergy-controlled LNG carriers are transiting, while ADNOC has tendered 14 million barrels under blockade conditions. EU sanctions on IRGC-linked entities have tightened compliance obligations across tanker and LNG operators. Houthi interdiction activity continues to suppress Bab-el-Mandeb / Red Sea traffic, sustaining rerouting via Cape of Good Hope and elevating war-risk premiums. Suez Canal steeper transit charges take effect mid-July. Singapore VLSFO pricing shows mixed signals. The VLCC orderbook has reached a record high amid the supply-route disruption environment.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Choke Point Stress | 9/10 | Critical | → no change |

| Port Congestion | 5/10 | Guarded | ▲ +1 |

| Sanctions & Compliance | 8/10 | High | ▲ +1 |

| Bunker Volatility | 7/10 | High | → no change |

| Crew & Labour | 5/10 | Guarded | ▼ -1 |

→ no change

The Strait of Hormuz remains under severe commercial stress: Iran's conditional reopening proposal, including new transit fees, adds an operating-cost layer for VLCC and LNG operators. QatarEnergy LNG carriers are transiting under elevated war-risk conditions. ADNOC's 14-million-barrel tender signals continued crude export pressure. EU sanctions on IRGC-linked entities impose fresh compliance screening obligations on tonnage providers, P&I clubs, and charterers. The VLCC orderbook reaching a record high suggests owners are positioning for a prolonged high-rate environment.

Operational signals

Headlines this cycle

→ no change

Dry-bulk operators face secondary pressure from the Hormuz and Bab-el-Mandeb disruptions. Rerouting via the Cape of Good Hope adds 10–14 transit days and materially increases bunker expenditure on Middle East–Asia and Europe–Asia commodity routes. No direct dry-bulk regulatory action is visible this cycle, but Singapore VLSFO price shifts and marine fuel cost pressures — as flagged in the German fishery context — signal broader cost-of-voyage increases for Panamax and Supramax operators.

Operational signals

Headlines this cycle

→ no change

Container freight rates are reported to be peaking this cycle, creating near-term revenue risk for boxship operators and schedule-reliability challenges for alliances. The containership orderbook is set to breach 40% — predominantly from smaller Chinese yards — which will intensify supply-side pressure once deliveries accelerate. Suez Canal steeper transit charges from mid-July represent a direct per-voyage cost increase. Ongoing Houthi activity in the Red Sea and Bab-el-Mandeb continues to force Cape rerouting, inflating nominal voyage costs and distorting schedule reliability.

Operational signals

Headlines this cycle

→ no change

TGS has secured multiple European offshore wind site-characterisation contracts utilising the Ramform Vanguard, confirming sustained survey demand in the Atlantic and North Sea corridors. AD Ports' 22-vessel, $350 million newbuild order indicates significant OSV fleet expansion in the Middle East/Gulf region. FPSO and OSV operators in the Persian Gulf are managing elevated transit-permission uncertainty and war-risk insurance costs amid the Hormuz disruption environment. Oil-price softening following the Israel–Iran strike suspension may reduce near-term upstream capex urgency.

Operational signals

Headlines this cycle

▲ +1 WoW

The Red Sea and Suez Canal corridor, a key superyacht and cruise transit route connecting the Mediterranean to the Indian Ocean, faces compounded commercial disruption: Houthi interdiction threats persist, Suez Canal imposes steeper charges from mid-July, and regional geopolitical uncertainty suppresses demand for Egypt and Gulf cruise itineraries. Superyacht owners and cruise operators are expected to continue favouring Cape of Good Hope routing or extended Mediterranean positioning, increasing operating costs and charter-day losses. The Suez Canal cruise initiative highlighted in Egypt signals institutional efforts to recover maritime tourism confidence.

Operational signals

Headlines this cycle

No named disruption events reported in this cycle.

Outlook pending next cycle.