Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

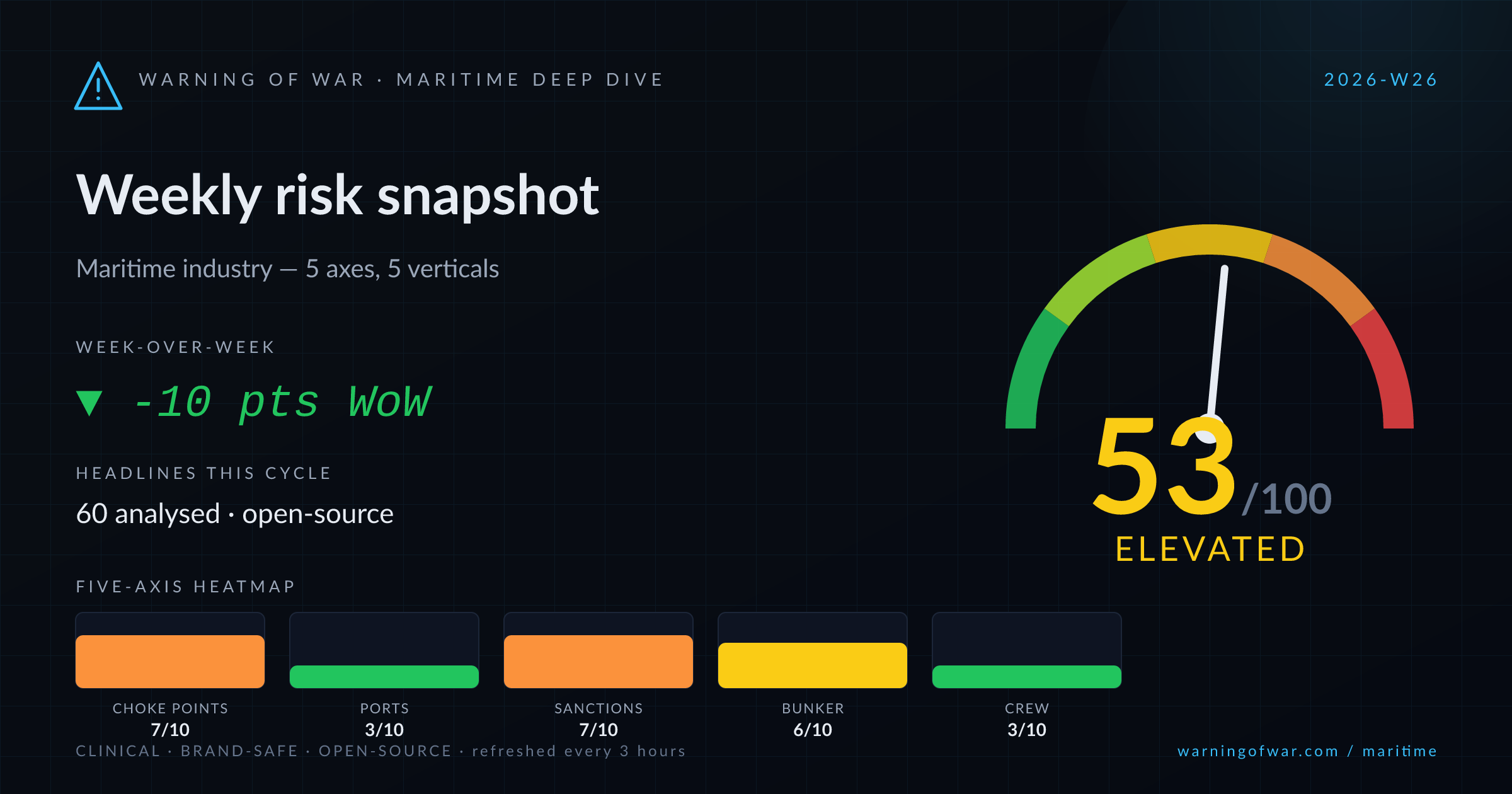

53/100 · Elevated — -10 pts WoW.

The Strait of Hormuz dominates this scoring cycle. Transit volumes are recovering following U.S.-Iran diplomatic engagement and a 14-point MOU, yet conflicting navigation directives from Washington and Tehran — including Iran's proposed insurance/toll scheme condemned by Maersk's CEO — sustain elevated war-risk premiums and operational uncertainty. Oil prices are trending lower as Brent reacts to renewed Iranian crude flows, compressing tanker spot earnings. The Russia shadow-fleet faces renewed EU/French-German legislative pressure. A sweeping 2026 Jones Act waiver reshapes U.S. cabotage. Transpetro's $427M MR1 newbuild order and Pan Ocean's $1.62Bn VLCC programme signal long-term tanker demand confidence despite near-term rate softness.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Choke Point Stress | 7/10 | High | ▼ -1 |

| Port Congestion | 3/10 | Normal | ▼ -1 |

| Sanctions & Compliance | 7/10 | High | ▼ -2 |

| Bunker Volatility | 6/10 | Elevated | → no change |

| Crew & Labour | 3/10 | Normal | ▼ -1 |

▼ -2 WoW

Hormuz traffic is recovering — 35 crossings in a single day at cycle peak — but Iran's proposed toll/insurance scheme and conflicting US-Iran navigation instructions are creating an unresolved compliance overlay for tanker operators. Brent falling toward $77 compresses TCE earnings. LNG shipping stocks (UP World LNG Index -3.88%) are pricing out the Hormuz risk premium. Asian refiners are limiting Iranian crude uptake, concentrating flows toward Chinese buyers. Transpetro's four MR1 newbuilds and Pan Ocean's four VLCC newbuilds on 20-year charters indicate sustained long-term demand confidence.

Operational signals

Headlines this cycle

→ no change

Aluminium commodity deficits persist even as Middle East tensions ease, sustaining minor bauxite/alumina routing complexity for Capesize and Panamax operators trading into Gulf destinations. China's tightened rare-earth export restrictions on 10 US companies threaten to bifurcate dry commodity trade lanes and reduce volumes on trans-Pacific corridors. India's SPR expansion programme via ONGC signals incremental petroleum-linked cargo demand on domestic coastal trades. UK steel-sector policy uncertainty under a new administration adds latent demand risk for iron-ore/coking-coal routes into European ports.

Operational signals

Headlines this cycle

▼ -1 WoW

Sea-Intelligence analysis this cycle highlights accelerating recovery speeds from major disruption events since 2012, but also notes that current Red Sea/Hormuz disruption recovery is delivering mixed results. Residual Hormuz uncertainty — conflicting navigation instructions, potential toll mechanisms — is maintaining Cape of Good Hope routeing as a fallback for box carriers with Middle East port calls. The Jones Act 2026 waiver continues to reshape US domestic container feeder economics. Strategic logistics priorities identified by Magaya/Adelante SCM underscore shippers' urgency on supply-chain resilience investments.

Operational signals

Headlines this cycle

▲ +1 WoW

Saipem and TechnipFMC secured combined offshore Angola contracts exceeding $1Bn for the Greater PAJ project (Azule Energy/Eni/BP JV), signalling robust deepwater capex appetite in West Africa. WINS acquired five DP crew transfer vessels via Fast Offshore Supply, targeting the growing offshore-wind CTV segment with deliveries in 2027-28. Cabship's Angola expansion ahead of AOG 2026 reflects active OSV and logistics market activity. India's SPR expansion tasked to ONGC adds incremental upstream infrastructure demand. Seacor Marine's shareholder pushing a $1Bn+ fleet sale adds M&A volatility to OSV equity valuations.

Operational signals

Headlines this cycle

→ no change

No material direct disruption signals affect the yacht and leisure segment this cycle. Seawork 2026 in Southampton recorded landmark attendance figures, reflecting broad commercial marine sector confidence that supports marina and refit-yard supply chains serving the superyacht segment. USD strength (dollar at one-year-plus high on hawkish Fed expectations) is a headwind for Euro-denominated superyacht orders and Mediterranean charter pricing for USD-invoiced clients. No cruise-sector operational disruptions or port-access issues are evident in current headlines.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| Strait of Hormuz Transit Resumption — Compliance Overlay | tanker | RISING | Vessel traffic through the Strait of Hormuz is recovering incrementally, but conflicting navigation and compliance directives from US and Iranian authorities — including Iran's proposed insurance scheme characterised as a transit fee — are sustaining elevated war-risk premium and operational uncertainty for tanker operators. |

| Iran Proposed Hormuz Transit Toll / Insurance Scheme | general | RISING | Iran's proposed mandatory insurance arrangement, publicly opposed by Maersk's CEO as a de-facto toll, represents an unresolved commercial-compliance risk that could add per-voyage cost for all vessel classes transiting the Strait of Hormuz. |

| Russia Shadow Fleet — EU Legislative Pressure | tanker | RISING | German and French parliamentarians are demanding concrete enforcement action against Russia's shadow-fleet tanker operations, raising the prospect of tighter EU port-access restrictions and enhanced AIS/flag-state scrutiny for non-compliant tonnage trading Russian crude. |

| Jones Act 2026 Waiver — US Cabotage Disruption | container | ACTIVE | A sweeping 2026 Jones Act waiver issued by the US Department of Homeland Security at DoD request has opened US domestic trades to foreign-flag tonnage, materially disrupting cabotage economics for Jones Act operators in container, tanker, and dry-bulk segments. |

| China Rare-Earth Export Restrictions on US Entities | dry-bulk | ACTIVE | China's Ministry of Commerce has placed 10 US companies under tightened rare-earth export controls, threatening to bifurcate trans-Pacific commodity trade flows and reduce dry-bulk cargo volumes on key US-bound corridors. |

| Angola Deepwater Capex Surge — Greater PAJ Project | offshore | RISING | Saipem and TechnipFMC have been awarded combined offshore Angola contracts exceeding $1Bn for the Greater PAJ project under Azule Energy, signalling a material step-up in West Africa deepwater activity that will tighten OSV and marine construction vessel supply in the region. |

Over the next 60–90 days, the Strait of Hormuz will remain the primary commercial risk axis. The US-Iran 14-point MOU and direct communications hotline reduce the probability of a hard closure, but Iran's proposed transit insurance/toll mechanism — if operationalised — will introduce a structurally new per-voyage cost item that war-risk underwriters, P&I clubs, and voyage-charter parties will need to address in contract language. Tanker spot rates are likely to remain suppressed as Brent softens on restored Iranian crude supply, though any diplomatic reversal would trigger a sharp rate spike. The Russia shadow-fleet enforcement campaign in the EU — if translated into port-state-control action and insurance blacklisting — could tighten effective tanker supply for Baltic and Black Sea trades. The 2026 Jones Act waiver will continue to reshape US domestic shipping economics, with competitive pressure on Jones Act operators likely to intensify until legislative clarity is restored. Offshore sector momentum in West Africa and the offshore-wind CTV market will sustain OSV demand, while the dry-bulk segment watches China's rare-earth trade restrictions and aluminium supply dynamics for demand-directional signals into Q4 2026.