Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

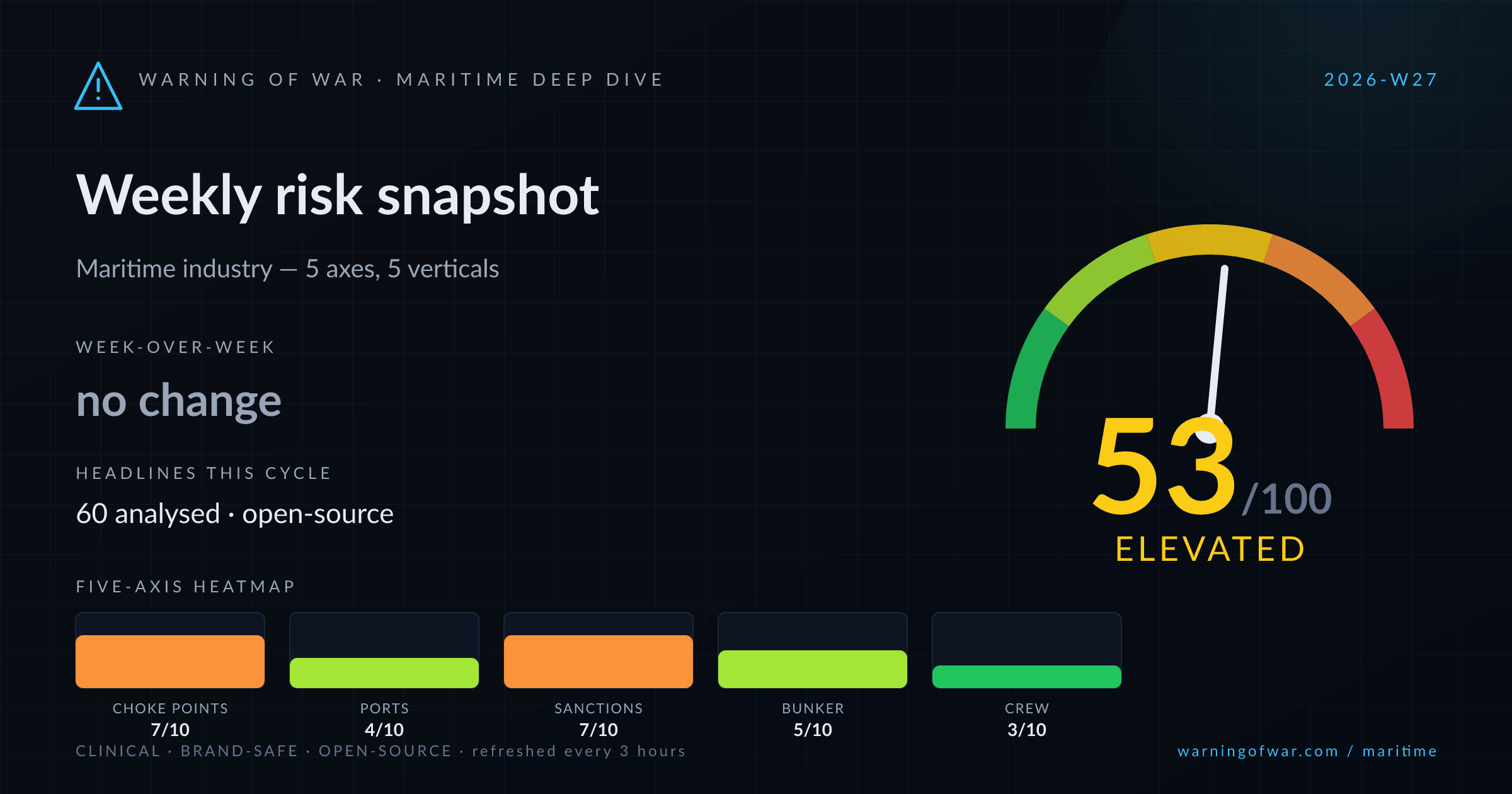

53/100 · Elevated — no change WoW.

The Strait of Hormuz dominates this scoring cycle: traffic is recovering following a period of elevated transit risk, with supertankers re-entering the Persian Gulf as US–Iran talks resume in Doha. War-risk premium pressure persists, and Oman's rejection of mandatory transit fees adds a regulatory dimension. Russia's price-cap ban extension through 2027 sustains shadow-fleet compliance scrutiny in the Baltic. Container markets are tightening — Maersk upgrades full-year 2026 guidance on Far East demand strength, while global shipping costs are reported at their highest level since the Red Sea disruption. Singapore bunker prices are rising, and B100 biofuel premiums are narrowing on EU routes, signalling active fuel-switch cost pressure.

| Axis | Score | Band | WoW |

|---|---|---|---|

| Choke Point Stress | 7/10 | High | → no change |

| Port Congestion | 4/10 | Guarded | ▲ +1 |

| Sanctions & Compliance | 7/10 | High | → no change |

| Bunker Volatility | 5/10 | Guarded | ▼ -1 |

| Crew & Labour | 3/10 | Normal | → no change |

▲ +1 WoW

Strait of Hormuz traffic is climbing as supertankers re-enter the Persian Gulf following a period of restricted access, with US–Iran diplomatic engagement in Doha providing conditional commercial relief. War-risk insurance premiums remain elevated. Russia's price-cap ban extension to end-2027 sustains sanctions-compliance cost for tanker operators. Newbuilding appetite is robust — Pan Ocean and J Ocean Heavy are adding VLCCs — while NAT insiders are adding exposure, signalling forward rate confidence. Product tanker leadership transition at Hafnia adds operational uncertainty.

Operational signals

Headlines this cycle

▼ -1 WoW

Fortescue's 200-million-tonne iron ore shipping milestone from Port Hedland signals robust Capesize throughput in the Australia–China corridor. However, copper futures are tracking a 4%-plus monthly loss on Fed tightening expectations and weak Chinese domestic demand, dampening industrial-metals freight demand. China's manufacturing PMI barely held expansion territory in June. Nissen Kaiun's accelerated bulker sell-off suggests some Japanese owners are reducing fleet exposure at current asset values, a moderate bearish signal for secondhand dry-bulk pricing.

Operational signals

Headlines this cycle

▲ +1 WoW

Maersk's full-year 2026 EBITDA guidance upgrade, driven by sustained Far East demand and rising spot rates, confirms that the container sector is operating well above prior expectations. Global shipping costs are reported at their highest since the Red Sea blockade period. Schedule reliability hit a 2026 high in May per Sea-Intelligence, though blank sailings remain a carrier capacity-management lever. MSC's $1.4bn entry into India's Vizhinjam transshipment terminal and Hapag-Lloyd's Hamburg and Tangier Med terminal deals signal alliance-level infrastructure consolidation accelerating.

Operational signals

Headlines this cycle

▼ -1 WoW

Skyborn Renewables takes full control of Germany's Nordergründe offshore wind farm, advancing European offshore wind asset consolidation. Korea's offshore wind programme is scaling — bid ratios doubled — but a Chinese-linked turbine supply deal in the Hanbit project is generating regulatory and supply-chain scrutiny. Shell's 65% LNG demand growth forecast to 2050 provides long-horizon support for offshore gas development and FPSO demand. AD Ports and IRH Global Trading are exploring a marine fuel partnership that could support offshore bunkering infrastructure in the Gulf.

Operational signals

Headlines this cycle

→ no change

No material disruption signals are present for the yacht and leisure vertical this cycle. The EcoMarine Index launch covering the Black and Caspian Seas introduces a new ESG benchmarking framework relevant to leisure and expedition operators active in those regions. Elevated war-risk sentiment around the Strait of Hormuz and Middle East broadly may discourage superyacht transits through the Arabian Gulf and Red Sea corridors in the near term, but no specific commercial events are recorded in this headline set.

Operational signals

Headlines this cycle

| Event | Vertical | Status | Description |

|---|---|---|---|

| Strait of Hormuz Transit Recovery | tanker | RISING | Supertanker traffic through the Strait of Hormuz is recovering incrementally as US–Iran diplomatic talks resume in Doha, reducing acute rerouting frequency while war-risk insurance premiums remain above pre-disruption baseline. |

| Russia Price-Cap Oil Ban Extension to 2027 | tanker | ACTIVE | President Putin extended Russia's ban on supplying oil subject to G7/EU price-cap mechanisms through end-2027, sustaining elevated sanctions-compliance cost and shadow-fleet activity across Baltic and dark-fleet tanker trades. |

| Global Container Rate Surge | container | ACTIVE | Global shipping costs have reached their highest level since the Red Sea blockade period, driven by sustained Far East demand strength and carrier capacity discipline, prompting Maersk's full-year 2026 earnings guidance upgrade. |

| Russian LNG Carrier Armament in Baltic | tanker | ACTIVE | A Russian civilian LNG carrier operating in the Baltic has been identified carrying heavy machine guns, raising war-risk and compliance scrutiny for vessels sharing Baltic transit corridors with Russian-flagged or Russian-chartered tonnage. |

| Oman Strait of Hormuz Transit Fee Rejection | general | STABLE | Oman has formally rejected mandatory transit fees for the Strait of Hormuz while indicating openness to maritime service charges, creating regulatory uncertainty for commercial operators planning Persian Gulf transits. |

| MSC–Adani Vizhinjam Transshipment Deal | container | ACTIVE | MSC's Terminal Investment Limited agreed to acquire a 49% stake in Adani Ports' Vizhinjam transshipment terminal for $1.4bn, accelerating Indian Ocean hub infrastructure consolidation and reshaping South Asia container routing. |

Over the next 60–90 days, the Strait of Hormuz will remain the primary commercial variable: if US–Iran negotiations in Doha produce a durable framework, war-risk premiums on Persian Gulf tanker trades should compress and crude/LNG loadings from Oman, Iraq, and Qatar will normalise, providing a meaningful tailwind to VLCC and LNG carrier earnings. Conversely, any diplomatic breakdown re-elevates rerouting cost and war-risk premia across the tanker and LNG verticals. Container markets are likely to sustain elevated freight rates through Q3 2026 on Far East demand momentum and carrier blank-sailing discipline, though the risk of sudden demand softening — particularly if Fed tightening accelerates and Chinese domestic consumption remains weak — is non-trivial. Russia's 2027 price-cap ban extension will keep sanctions-compliance costs structurally elevated for tanker operators with CIS or Baltic exposure. Biofuel adoption dynamics, particularly B100 premium compression on Singapore–EU routes, will sharpen fuel-strategy decisions for operators preparing for FuelEU Maritime compliance. Offshore wind M&A in Europe and supply-chain scrutiny in Korea's tender programme are expected to generate further asset and regulatory activity through the quarter.