Critical Minerals & Rare Earths

8/10Critical

DRC cobalt quota withdrawal and Indonesian nickel investment wave reshape battery-metals supply structure.

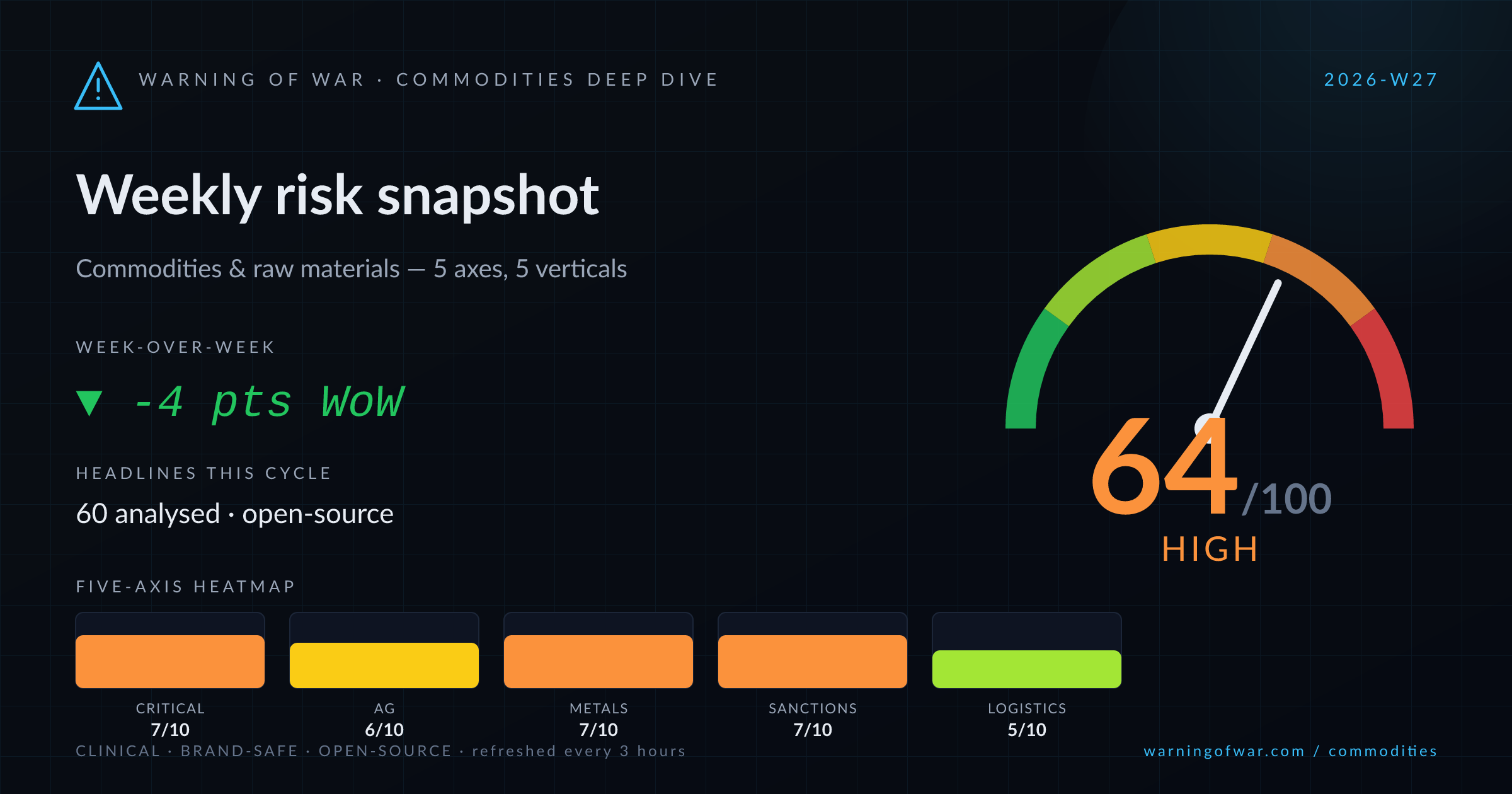

WEEKLY REPORT · 2026-W27 · Jun 29 – Jul 5, 2026

Weekly commodities & raw materials risk snapshot — composite 64/100 (High), ◆ first weekly snapshot.

DRC's 2026 cobalt export-quota withdrawal tightens critical-mineral supply just as CATL restarts its Jiangxi lithium mine and EcoPro commits ~$1.75 bn across Indonesian nickel smelter stakes. Goldman Sachs projects a sustained copper price rally through 2027 while aluminium retreats to a four-month LME low on fading Gulf risk premiums. Russia's wheat harvest faces a fuel-supply crunch and adverse weather, lifting CBOT grain benchmarks post-USDA. The Trump administration has declared a fertilizer emergency, elevating import-dependency risk. Hormuz partial de-escalation leaves iron-ore steelmaking supply chains — notably BHP, Rio Tinto, and Fortescue Pilbara shipments — structurally exposed.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

Critical

DRC cobalt quota withdrawal and Indonesian nickel investment wave reshape battery-metals supply structure.

High

Russian wheat harvest stress and Ohio frost damage lift CBOT grain benchmarks; Philippine rice price caps add import-policy risk.

Guarded

Softs complex sees limited new commercial signal this cycle; no major supply or price disruptions reported.

High

Copper rally, aluminium retreat, and structurally evolving iron-ore trade flows dominate base-metals price action.

High

US fertilizer emergency declaration and Nepal's 210,000-tonne import programme highlight acute supply-security concerns.

DRC's withdrawal of unused 2026 cobalt export quotas reduces spot tonnage availability and tightens sovereign control over battery-metal feedstock, exerting upward pressure on cobalt benchmark prices.

The Trump administration's formal fertilizer emergency declaration elevates US import-dependency risk and may accelerate domestic procurement programmes and tariff-policy review across urea, potash, and phosphate channels.

Concurrent fuel-supply constraints and adverse precipitation across Russian wheat-growing regions introduce material downside risk to Q3 2026 export volumes and exert upward pressure on CBOT wheat benchmarks.

While Strait of Hormuz tensions have partially eased, Fastmarkets' Iron Ore Decoded 2026 analysis confirms that steelmaking supply-chain normality — including Pilbara-origin shipments from BHP, Rio Tinto, and Fortescue — has not been fully restored.

EcoPro's ~$1.75 bn investment commitment to Indonesian nickel smelting coincides with a BYD battery breakthrough that challenges the economic rationale for Indonesia's nickel-supply cartel, creating competing structural forces in the NMC versus LFP cathode market.

Goldman Sachs projects sustained copper price appreciation through 2027, prompting documented industrial substitution towards LME aluminium, which itself has retreated to a four-month low as Gulf risk premiums fade.

Over the 60–90 day forward window, the fertilizer vertical faces the greatest near-term policy volatility: the US emergency declaration is likely to trigger executive procurement actions and potential tariff reviews on urea and potash imports, while Nepal's mid-August tender deadline will test spot-market availability. Grain markets will remain sensitive to weekly updates on the Russian wheat harvest — any further fuel-logistics deterioration or precipitation shortfall could push CBOT wheat above near-term resistance and compress import margins for Egypt and Southeast Asian sovereign buyers. In critical minerals, the DRC cobalt quota tightening will compound with Indonesia's evolving nickel-investment landscape; EcoPro's smelter commissioning timelines and BYD's LFP adoption curve will be the key variables to monitor. Copper's Goldman Sachs-backed bull case through 2027 makes end-user hedging decisions increasingly urgent, particularly as aluminium substitution — now a documented industrial response — begins to stress LME aluminium inventories. Iron ore faces a structural bifurcation: India's high-grade import deficit will support premium-grade ore differentials (65% Fe and above), while China's sub-consensus PMI and property-sector drag cap upside on standard 62% Fe Pilbara benchmarks. Confidence across all verticals is conditioned on continued availability of open-source procurement, benchmark, and policy data.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.