Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

65/100 · High — first weekly snapshot.

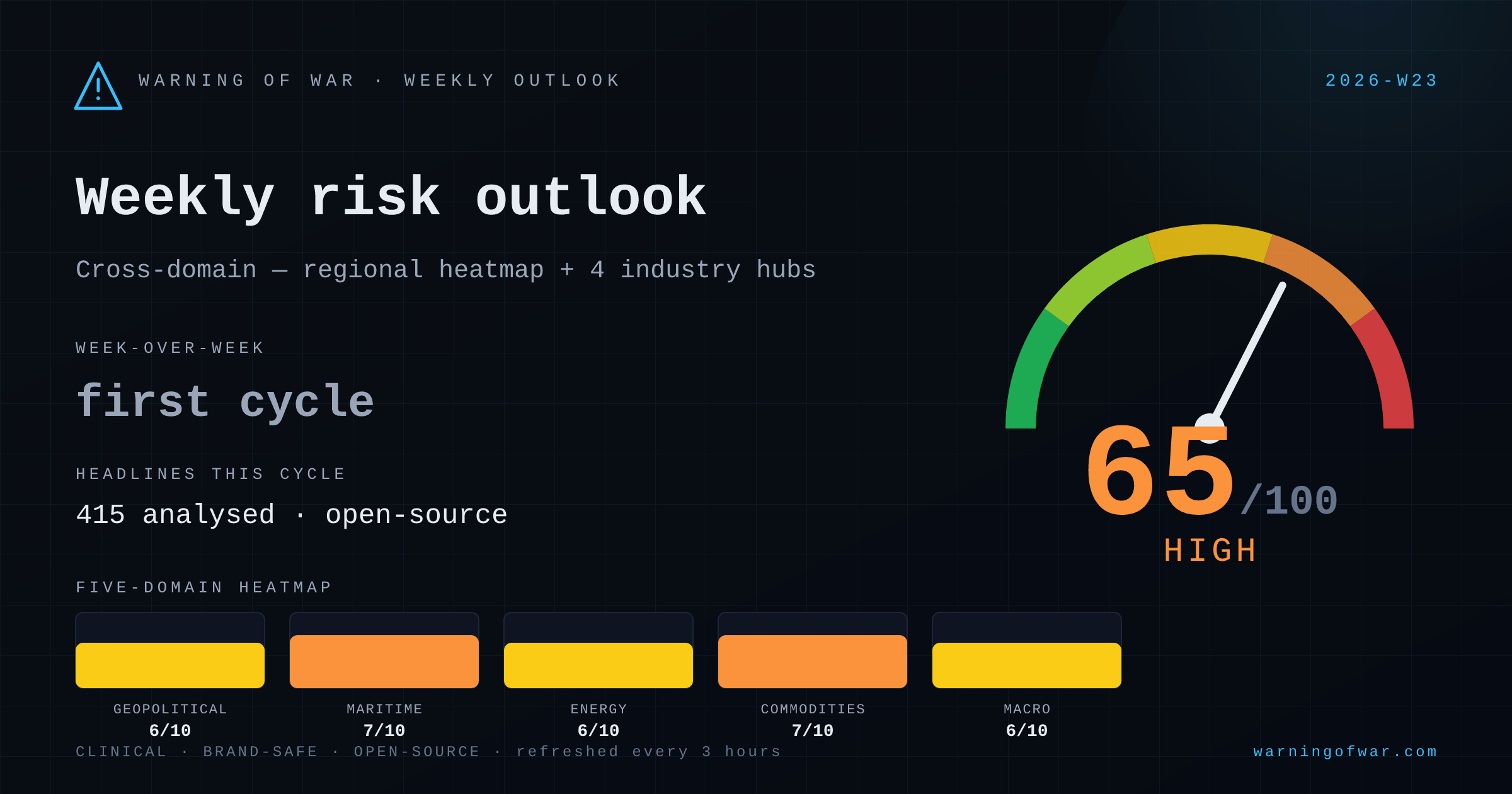

Cross-domain composite holds at 65/100 (High) for the week ahead, blended evenly across the regional heatmap and the maritime, energy, commodities, and macro hubs. Commodities & Materials leads the picture at 69/100; Geopolitical & Regional is the least-stressed domain at 59/100. 415 open-source headlines were analysed across all domains this cycle.

| Domain | Score | Band | WoW |

|---|---|---|---|

| Geopolitical & Regional | 6/10 | Elevated | · — |

| Maritime & Supply Chain | 7/10 | High | · — |

| Energy Markets | 6/10 | Elevated | · — |

| Commodities & Materials | 7/10 | High | · — |

| Macro & Sovereign | 6/10 | Elevated | · — |

(no prior week)

Regional risk is concentrated in Middle East, Europe, South America. The cross-region composite sits at 59/100, blended from maritime, energy, commodities, and macro exposure across 7 monitored regions.

Underlying signals

Headlines this cycle

(no prior week)

The Strait of Hormuz dominates this cycle as the single most operationally disruptive choke point globally, with confirmed mine sightings in Omani waters, limited transits under a US-Iran ceasefire extension, and a US interdiction of a blockade-running vessel. War-risk premiums and rerouting costs are materially elevated for VLCCs, LNG carriers, and product tankers transiting the Persian Gulf. Separately, France has intercepted multiple sanctioned Russian shadow-fleet tankers in the Atlantic, escalating EU enforcement pressure. Singapore residual fuel stocks have declined 6%, tightening bunker supply in a critical hub. Container markets face a rate spike on structural empty-box imbalances and ongoing route disruption.

Underlying signals

Headlines this cycle

(no prior week)

Global crude markets are under material upside price pressure: Brent has breached $93/bbl and WTI near $88.50, driven by active US-Iran military exchange and expanded Israeli operational posture affecting Strait of Hormuz transit risk. Kazakhstan's Tengiz field is recovering from an operational incident; Kashagan has been ordered to revise its turnaround plan and continue output. Ukrainian drone strikes have repeatedly targeted Russian pipeline infrastructure, refineries, and fuel depots, prompting Moscow to ban jet-fuel exports. France's Navy has boarded a Russia-linked shadow-fleet tanker. Goldman Sachs flags bilateral price risk: Iran-supply upside offset by demand-destruction downside. China crude import volumes are slumping on economic drag. Canada's oil-sands face seasonal wildfire disruption risk.

Underlying signals

Headlines this cycle

(no prior week)

This cycle's dominant signals are concentrated in critical minerals and base metals. Tesla's resolution of a graphite supply default with Syrah Resources (Mozambique) stabilises near-term anode supply, while rare earth shortages continue pressuring semiconductor and defence supply chains — Solvay's Viridis LOI targets 2028 relief. Copper commands multi-bank upgrades: Goldman Sachs and Citi both raised LME end-year forecasts by 10%+ as US stockpiling and pending 15% refined-copper tariffs tighten the global concentrate market. DRC's proposed tripling of lithium royalties signals upward cost pressure. China's stainless steel production cuts and Japan's anti-dumping probes on Chinese, Korean, and Taiwanese steel add further bilateral friction. Australia's wheat harvest is forecast down nearly 50%, tightening Southern Hemisphere grain balances.

Underlying signals

Headlines this cycle

(no prior week)

This cycle's macro signal is driven by five concurrent dynamics: (1) Fed independence tensions and Kevin Warsh's prospective regime shift pressuring U.S. rate expectations; (2) the EU's 20th–21st Russia sanctions packages and France's French Navy interdiction of a sanctioned shadow-fleet tanker escalating enforcement intensity; (3) multi-frontier sovereign stress—Ghana post-IMF revenue reform, Malawi IMF programme uncertainty, Sri Lanka's USD 695 million EFF disbursement, and Moody's negative-outlook revision on Mali; (4) elevated EM FX pressure across the Korean Won, Vietnamese Dong, Nigerian Naira, and Japanese Yen amid geopolitical safe-haven dollar demand; and (5) South Korea's four-decade export highs and China's outbound investment restrictions reshaping Asia-Pacific trade-flow dynamics.

Underlying signals

Headlines this cycle

| Event | Domain | Status | Description |

|---|---|---|---|

| Russia jet fuel export ban | energy | ACTIVE | Russia has imposed a ban on aviation fuel exports through 30 November, constraining European jet-A1 supply and driving procurement reallocation costs for regional buyers. |

| Russian refinery throughput disruption | energy | ACTIVE | Infrastructure disruption to Russian refinery operations is constraining domestic output and contributing to the jet fuel export restriction, with downstream effects on European refined product supply chains. |

| US-Iran kinetic exchange cycle | energy | ACTIVE | Ongoing US-Iran exchange of strikes is sustaining a supply-disruption risk premium in oil markets and elevating operational risk ratings for Gulf-region energy infrastructure. |

| Kuwait regional disruption exposure | maritime | ACTIVE | Kuwait has been drawn into the regional disruption perimeter, generating new port-approach risk ratings and logistics uncertainty for GCC-hub operators. |

| Gulf equity market risk-off retreat | macro | ACTIVE | Most Gulf equity markets are easing as institutional participants reprice escalation risk, compressing valuations across financial and energy-linked indices. |

| Canada-U.S. Steel & Aluminum Tariff Escalation | macro | ACTIVE | Canada has imposed 25% reciprocal tariffs on U.S. steel and aluminum exports, elevating input costs across North American manufacturing and construction supply chains. |

The week ahead is led by Commodities & Materials and Maritime & Supply Chain risk. Detailed five-axis decompositions follow in this week's sector deep dives — Maritime on Tuesday, Commodities and Energy on Wednesday, and Macro on Thursday. This outlook synthesises the live regional heatmap with all four industry hubs, refreshed every three hours from open-source signals.