Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

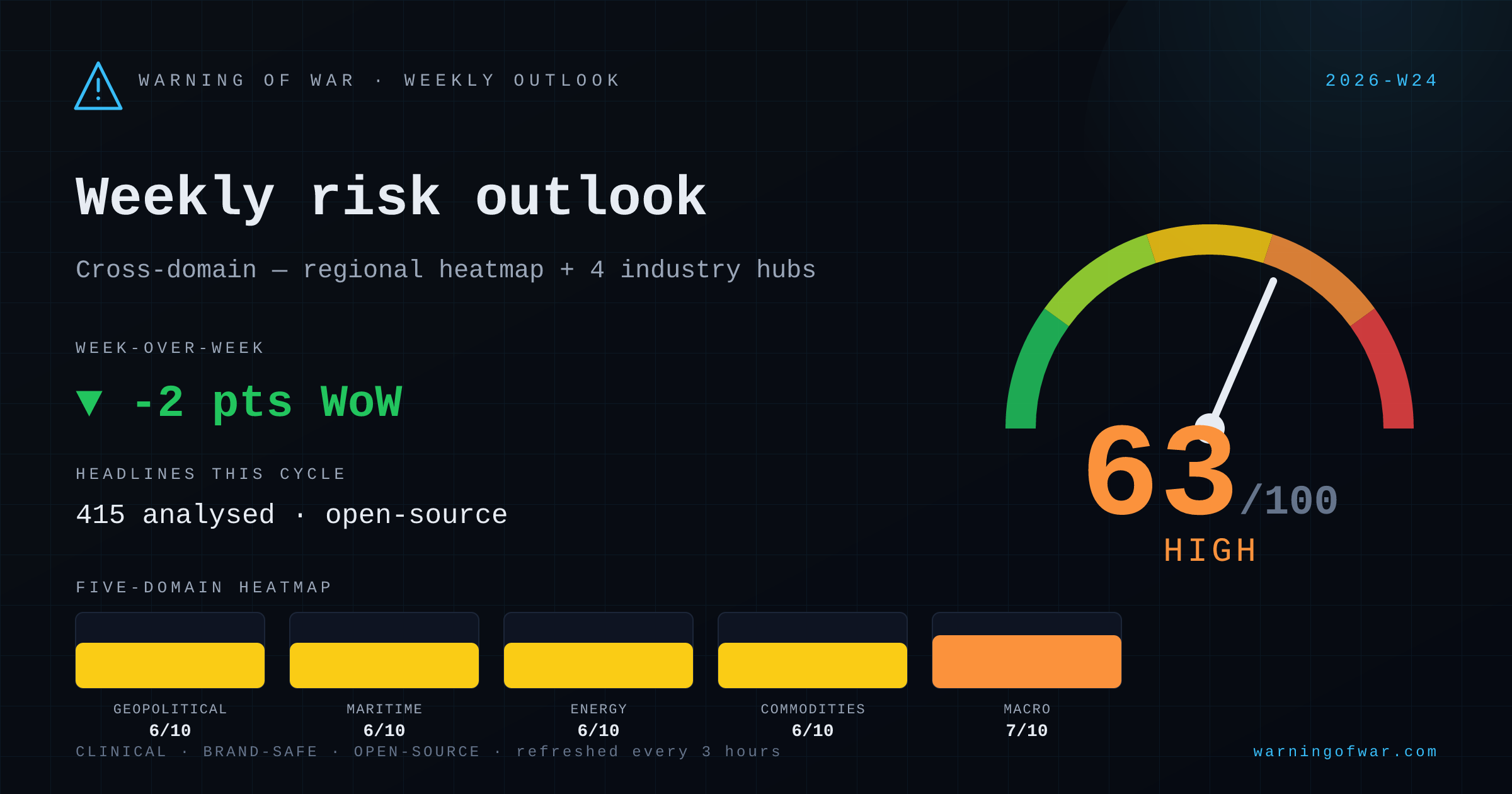

63/100 · High — -2 pts WoW.

Cross-domain composite holds at 63/100 (High) for the week ahead, blended evenly across the regional heatmap and the maritime, energy, commodities, and macro hubs. Macro & Sovereign leads the picture at 68/100; Energy Markets is the least-stressed domain at 60/100. 415 open-source headlines were analysed across all domains this cycle.

| Domain | Score | Band | WoW |

|---|---|---|---|

| Geopolitical & Regional | 6/10 | Elevated | → no change |

| Maritime & Supply Chain | 6/10 | Elevated | ▼ -1 |

| Energy Markets | 6/10 | Elevated | → no change |

| Commodities & Materials | 6/10 | Elevated | ▼ -1 |

| Macro & Sovereign | 7/10 | High | ▲ +1 |

→ no change

Regional risk is concentrated in Middle East, South America, Pacific. The cross-region composite sits at 60/100, blended from maritime, energy, commodities, and macro exposure across 7 monitored regions.

Underlying signals

Headlines this cycle

▼ -1 WoW

Choke-point stress is the dominant signal this cycle. Houthi forces have declared a renewed total ban on Israeli-affiliated shipping through Bab-el-Mandeb, extending Red Sea diversion pressure that has been in place since late 2023. Simultaneously, Iran signals new transit-fee conditions for the Strait of Hormuz, with reported levies of up to USD 2 million per vessel — a material cost event for tanker and LNG operators. Panama Canal Authority has reduced Neopanamax draft limits effective 1 July, echoing the 2023 drought disruption. US naval assets confirm interdiction operations near Hormuz. Taiwan Strait sees renewed Chinese government-vessel incursions. Combined choke-point pressure is the broadest seen in recent cycles.

Underlying signals

Headlines this cycle

→ no change

WTI is trading near $92–$93 with Brent testing $97, driven by Strait of Hormuz operational disruption and Iran–Israel geopolitical escalation. OPEC+ has approved a fourth consecutive monthly quota hike of 188,000 bpd for July — cumulative additions approaching 600,000 bpd since Hormuz closure — but market sentiment discounts quota increases given choke-point transit uncertainty. Iran is offering Basrah-competing crudes to Chinese buyers at discounts as demand softens. Saudi Aramco has cut July official selling prices to Asia, though pricing remains at historically elevated levels. Argentina's first LNG export project advances with Adani Ports/APSEZ securing a $70 million, 10-year marine services contract serving India-bound cargoes. Delfin Midstream has taken FID on America's first FLNG vessel.

Underlying signals

Headlines this cycle

▼ -1 WoW

Middle-East escalation between Iran and Israel has disrupted Strait of Hormuz transit expectations, driving oil higher and threatening fertilizer freight economics. Saudi Aramco cut July OSPs to Asia while Iranian crude is offered to Chinese refiners at discounted differentials. Copper rebounded on SHFE/LME China-buying flows after a technical slump, but Fed rate-hike fears and tightening liquidity cap upside. China coking-coal benchmarks hit a cycle-high on domestic safety-related mine shutdowns. Lithium ETFs rallied on policy floor signals and EV-demand optimism, while tungsten stockpiling escalates as the EU and US race to diversify away from China's dominant rare-earth and critical-mineral supply chains. Latvia-routed Russian fertilizer flows are under renewed political scrutiny.

Underlying signals

Headlines this cycle

▲ +1 WoW

Global macro conditions are elevated across multiple axes this cycle. The South Korean won has breached 17-year highs against the USD (1,550–1,560 range), triggering emergency meetings by Korean financial authorities, a joint FX speculation probe, and verbal intervention by Deputy Prime Minister Koo. Indonesia's foreign reserves are declining at the steepest rate since 2018, with Danantara launching a US bond roadshow amid deepening market pressure. Fitch revised its global growth outlook lower on Middle East supply-side energy disruption. The EU Commission is advancing a 21st Russia sanctions package, while China is tightening capital controls and Ethiopia's Eurobond market access has collapsed. The Fed's rate-hike path is reinforced by strong US labour data.

Underlying signals

Headlines this cycle

| Event | Domain | Status | Description |

|---|---|---|---|

| ECB Rate Tightening Cycle | macro | ACTIVE | The ECB is expected to raise its benchmark rate by 25 basis points, leading G7 central banks in tightening and materially repricing eurozone sovereign and corporate borrowing costs. |

| Middle East Conflict Inflation Pass-Through | energy | ACTIVE | Ongoing Middle East conflict is sustaining a cost premium on European energy imports routed through eastern Mediterranean and Red Sea corridors, feeding directly into ECB inflation deliberations. |

| Tata Steel UK Furnace Delay | commodities | ACTIVE | Tata Steel's £1.25bn electric arc furnace project faces a delay attributable to electrical grid connectivity constraints, deferring a significant uplift in domestic UK steel production capacity. |

| BALTOPS 26 Baltic Naval Exercise | maritime | ACTIVE | Multinational NATO naval exercise activity in the Baltic Sea is applying marginal upward pressure on regional maritime insurance risk classifications and route risk premiums. |

| Houthi Red Sea Israeli Shipping Ban | maritime | ACTIVE | Houthi forces have declared a formal ban on Israeli-linked vessel transits through the Red Sea, operationally restricting a key segment of Asia-Europe shipping traffic and increasing diversion to longer alternative routes. |

| Israel-Iran Aerial Exchange Escalation | energy | ACTIVE | Reciprocal aerial strike activity between Israel and Iran has introduced material operational uncertainty for energy infrastructure assets — including refinery, terminal, and grid capacity — in both countries. |

The week ahead is led by Macro & Sovereign and Maritime & Supply Chain risk. Detailed five-axis decompositions follow in this week's sector deep dives — Maritime on Tuesday, Commodities and Energy on Wednesday, and Macro on Thursday. This outlook synthesises the live regional heatmap with all four industry hubs, refreshed every three hours from open-source signals.