Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

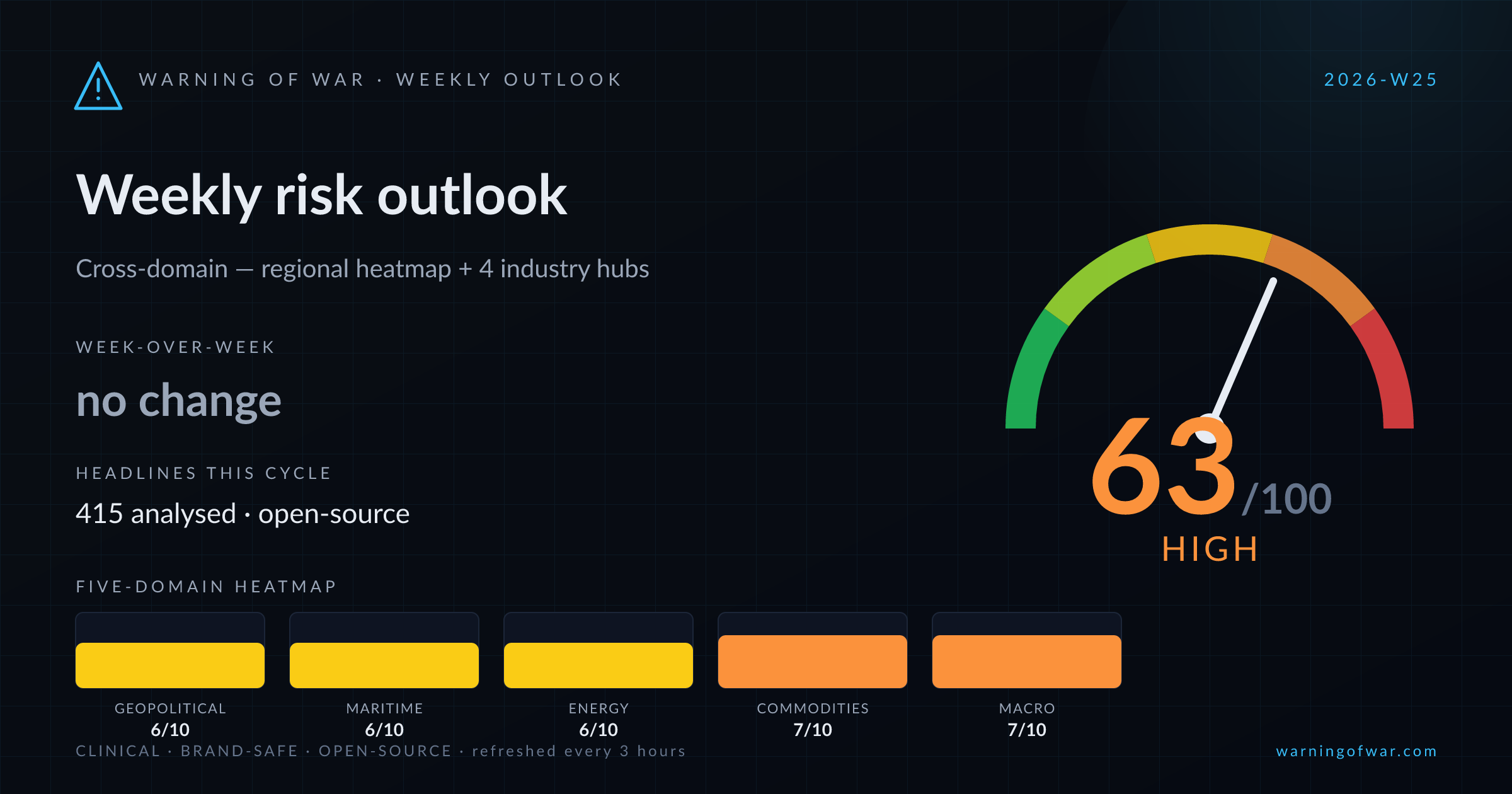

63/100 · High — no change WoW.

Cross-domain composite holds at 63/100 (High) for the week ahead, blended evenly across the regional heatmap and the maritime, energy, commodities, and macro hubs. Commodities & Materials leads the picture at 66/100; Energy Markets is the least-stressed domain at 59/100. 415 open-source headlines were analysed across all domains this cycle.

| Domain | Score | Band | WoW |

|---|---|---|---|

| Geopolitical & Regional | 6/10 | Elevated | → no change |

| Maritime & Supply Chain | 6/10 | Elevated | → no change |

| Energy Markets | 6/10 | Elevated | → no change |

| Commodities & Materials | 7/10 | High | ▲ +1 |

| Macro & Sovereign | 7/10 | High | → no change |

→ no change

Regional risk is concentrated in Middle East, Pacific, Europe. The cross-region composite sits at 64/100, blended from maritime, energy, commodities, and macro exposure across 7 monitored regions.

Underlying signals

Headlines this cycle

→ no change

The dominant signal this cycle is the tentative US–Iran peace framework and the anticipated reopening of the Strait of Hormuz, through which approximately 500 vessels are reported to be awaiting safe passage. War-risk premiums are beginning to ease but industry caution persists pending mine-clearance operations and formal transit-fee clarification. Concurrently, coordinated EU and UK enforcement actions against Russia's shadow fleet — including the first Royal Navy boarding of vessel SMYRTOS — materially elevate sanctions-compliance pressure. Singapore residual fuel oil stocks have slumped 25% in June, tightening bunker availability at a critical juncture as Gulf trade routes prepare to reopen.

Underlying signals

Headlines this cycle

→ no change

The US-Iran framework agreement to reopen the Strait of Hormuz has triggered a significant repricing cycle: Brent fell below $83/bbl and WTI slumped ~5% intraday, while European TTF gas prices dropped over 6%. LNG carrier Disha — carrying Qatari cargo — became the first vessel to transit Hormuz post-deal, though Japanese shipowners and LNG players remain cautious pending formalisation. Mine-clearance timelines of several weeks and a backlog of ~600 vessels constrain immediate flow normalisation. QatarEnergy's concurrent force majeure declaration and an OPEC+ output delay expectation are partially offsetting bearish crude pressure. Russia's domestic gasoline shortage is a separate refining signal.

Underlying signals

Headlines this cycle

▲ +1 WoW

A US–Iran memorandum has partially reopened the Strait of Hormuz to commercial traffic, easing acute choke-point risk for fertilizer and energy flows, though analysts caution that full normalization of Hormuz trade may require months. Copper on the LME surged on the de-escalation signal, while Anglo American lifted the FTSE 100 mining index. Indonesia's nickel-ore price data faced a government-website publication delay, and China publicly criticised Jakarta's investment climate over nickel curbs. On critical minerals, a North America–Japan rare-earth pact targeting high-performance magnets and Iondrive's 93.5% dysprosium-recovery benchmark reinforce Western re-shoring. USDA trimmed its winter-wheat forecast on persistent Plains drought. Sugar and biofuel benchmarks retreated on Hormuz re-opening pricing.

Underlying signals

Headlines this cycle

→ no change

This cycle is dominated by three concurrent macro themes. First, the EU has advanced its 20th Russia sanctions package — adding 34 individuals and 47 entities, tightening energy-revenue restrictions, and targeting the shadow fleet — while Sweden presses for a 21st package. Second, a US–Iran ceasefire and Hormuz reopening agreement has driven oil-price compression, Eurozone bond-yield declines, and KRW depreciation, materially shifting G10 and EM central-bank policy calculus. Third, Fitch affirmed China's sovereign 'A' rating and Côte d'Ivoire's 'BB', while the IMF reached a $690 million staff-level disbursement agreement with Ukraine and the World Bank committed $750 million in programme lending to Kenya. ECB governing council members Lagarde and Kazimir signal persistent second-round inflation effects, while the Bank of England is expected to hold rates, diverging from the ECB's recent hike.

Underlying signals

| Event | Domain | Status | Description |

|---|---|---|---|

| Gazprom Gas Import Ban Legal Challenge | energy | ACTIVE | A Gazprom subsidiary has formally challenged the EU's ban on Russian gas imports, introducing prolonged legal and arbitration risk that sustains uncertainty over contracted gas supply instruments in European markets. |

| ECB Frontloaded Rate Hike Cycle | macro | ACTIVE | The ECB continues to front-load interest rate increases while simultaneously cutting its eurozone growth forecast, compressing corporate refinancing conditions and dampening FDI appetite across the bloc. |

| Vessel backlog clearance — Hormuz queue | maritime | ACTIVE | Approximately 500 commercial vessels are queued for Hormuz passage, creating a concentrated operational backlog that will strain port scheduling and charter markets upon lane clearance. |

| Forced-Labour Tariff Framework Relaunch | commodities | ACTIVE | The administration is relaunching a tariff enforcement campaign citing forced-labour concerns, elevating customs compliance and landed-cost risk for North American importers across multiple product categories. |

| USMCA Trade Agreement Uncertainty | macro | ACTIVE | USMCA continuity remains unresolved and is absent from the G7 agenda, sustaining agri-commodity contract and cross-border investment uncertainty for North American operators. |

| Cuba Energy Sector Sanctions (Unión Cuba-Petróleo) | energy | ACTIVE | US sanctions imposed on Cuba's state-owned energy company Unión Cuba-Petróleo restrict access to international energy markets and financing, constraining the entity's operational capacity. |

The week ahead is led by Commodities & Materials and Macro & Sovereign risk. Detailed five-axis decompositions follow in this week's sector deep dives — Maritime on Tuesday, Commodities and Energy on Wednesday, and Macro on Thursday. This outlook synthesises the live regional heatmap with all four industry hubs, refreshed every three hours from open-source signals.