Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

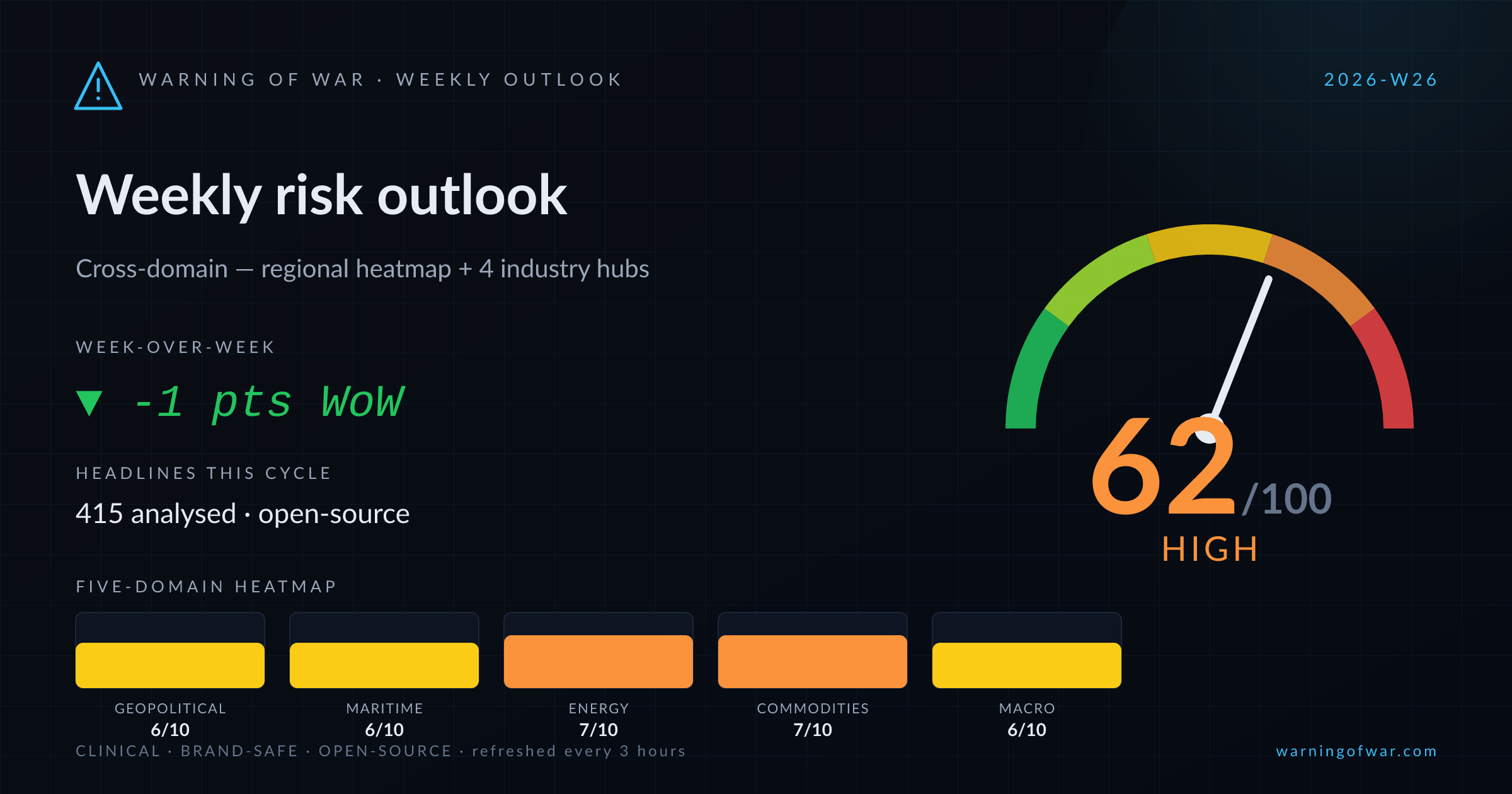

62/100 · High — -1 pts WoW.

Cross-domain composite holds at 62/100 (High) for the week ahead, blended evenly across the regional heatmap and the maritime, energy, commodities, and macro hubs. Commodities & Materials leads the picture at 68/100; Maritime & Supply Chain is the least-stressed domain at 57/100. 415 open-source headlines were analysed across all domains this cycle.

| Domain | Score | Band | WoW |

|---|---|---|---|

| Geopolitical & Regional | 6/10 | Elevated | → no change |

| Maritime & Supply Chain | 6/10 | Elevated | → no change |

| Energy Markets | 7/10 | High | ▲ +1 |

| Commodities & Materials | 7/10 | High | → no change |

| Macro & Sovereign | 6/10 | Elevated | ▼ -1 |

→ no change

Regional risk is concentrated in Middle East, Africa, South America. The cross-region composite sits at 61/100, blended from maritime, energy, commodities, and macro exposure across 7 monitored regions.

Underlying signals

Headlines this cycle

→ no change

The Strait of Hormuz remains the dominant commercial risk signal this cycle, with alternating closure declarations and partial reopenings creating navigational uncertainty for tankers, LNG carriers, and bulkers transiting the Persian Gulf. Hundreds of vessels are staged outside the Gulf awaiting confirmation of sustained access. The US–Iran Switzerland talks have produced a provisional roadmap, with a bilateral crisis hotline established, yet MOL's CEO projects at least one month before transit normalises. Shadow-fleet tonnage is flagged for contraction under elevated OFAC scrutiny. Fujairah VLSFO stocks are 9% below May averages, applying modest upward pressure on bunker costs in the region. Venezuelan crude exports have more than doubled, partially offsetting Middle East supply disruption for Atlantic-basin refiners.

Underlying signals

Headlines this cycle

▲ +1 WoW

Global energy markets are navigating elevated cross-vertical stress this cycle. The Ras Laffan LNG complex operational incident has constrained Qatari export capacity, with QatarEnergy recalling empty carriers to accelerate restart. Hormuz transit risk is amplified by Iran-US tension and Iranian crude surge flows, while India is absorbing record Russian crude volumes under OFAC waiver cover. Antipinsky refinery in Siberia sustained drone-related operational interruption. Baku's SOCAR refinery reported a contained process-unit release. WTI is testing the $75 support level as Brent trades below $80 on prospective Iran deal signals. Dangote refinery now covers 87% of Nigeria's petrol demand, reshaping West African product flows.

Underlying signals

Headlines this cycle

→ no change

China's Ministry of Commerce has added MP Materials, USA Rare Earth, and eight additional U.S. defence-adjacent firms to its export-control list, materially restricting rare earth and graphite flows to U.S. end-users. EU CRMA re-shoring policy is accelerating: a £50 m UK critical-minerals programme, EU–Brazil strategic partnership talks, and G7's $64 bn push signal structural diversification spend. Lithium benchmarks hit 10-week lows on CATL mine re-activation speculation. BHP iron ore stocks re-enter focus on China steel signals, offset by a long structural plateau in Chinese property-driven steel demand. Strait of Hormuz reopening eases fertilizer freight risk; Indonesia's first 47,250-tonne urea shipment reaches Australia.

Underlying signals

Headlines this cycle

▼ -1 WoW

Global macro conditions this cycle reflect moderate-to-elevated stress across multiple axes. The World Bank's USD 1.5 bn India disbursement and an IMF mission to Sri Lanka signal continued multilateral engagement with EM sovereigns. Moody's has revised Philippines banking sector outlook to negative, while Fitch affirmed Kazakhstan at BBB/Stable. The Bank of England has finalised a softened stablecoin regulatory framework. The ECB faces a public debate on the pace of quantitative tightening. Kevin Warsh's prospective leadership of the Federal Reserve introduces forward-guidance uncertainty. China's People's Bank held LPRs unchanged for a 13th consecutive month. Hungary's threatened veto of the EU's 20th Russia sanctions package introduces cohesion risk for OFAC-aligned Western regimes.

Underlying signals

Headlines this cycle

| Event | Domain | Status | Description |

|---|---|---|---|

| Tyumen Refinery Operational Disruption | energy | ACTIVE | Disruption to Tyumen refinery throughput is constraining Russian refined fuel output, with secondary tightening of fuel availability and sales restrictions observable in adjacent Crimea markets. |

| EU Carbon Border Adjustment Mechanism (CBAM) Friction | commodities | ACTIVE | CBAM is generating measurable competitiveness friction for energy-intensive commodity exporters into the EU, raising effective import costs for aluminium and potentially other carbon-intensive materials. |

| GBP Macro Pressure — BoE Pause & Political Uncertainty | macro | ACTIVE | A combination of the Bank of England's rate pause and political leadership uncertainty is compressing GBP against EUR and USD, elevating FX risk for UK-EU cross-border commercial contracts. |

| US-Iran Hormuz crisis hotline establishment | maritime | ACTIVE | The US and Iran have operationalized a dedicated bilateral communication channel to manage Hormuz shipping security incidents, reducing immediate escalation risk for vessel operators. |

| Cryptocurrency sanctions wrinkle in Iran diplomacy | macro | ACTIVE | Cryptocurrency-related sanctions provisions have emerged as a complicating technical factor in US-Iran diplomatic negotiations, potentially affecting how Iran accesses or deploys released financial assets. |

| China retaliatory sanctions on U.S. defense & rare-earth firms | commodities | ACTIVE | Beijing has sanctioned ten U.S. defense and rare-earth entities and restricted rare-earth exports to American defense firms, disrupting critical-minerals supply pipelines for defense, aerospace, and energy-transition manufacturing. |

The week ahead is led by Commodities & Materials and Energy Markets risk. Detailed five-axis decompositions follow in this week's sector deep dives — Maritime on Tuesday, Commodities and Energy on Wednesday, and Macro on Thursday. This outlook synthesises the live regional heatmap with all four industry hubs, refreshed every three hours from open-source signals.