Ctrl+A to select everything, then Ctrl+C to copy, then paste into a new Substack post. Headings, the table, the hero image and links convert to native Substack blocks. (This yellow hint is outside the article — you can leave it selected; Substack drops it on paste.)

63/100 · High — +1 pts WoW.

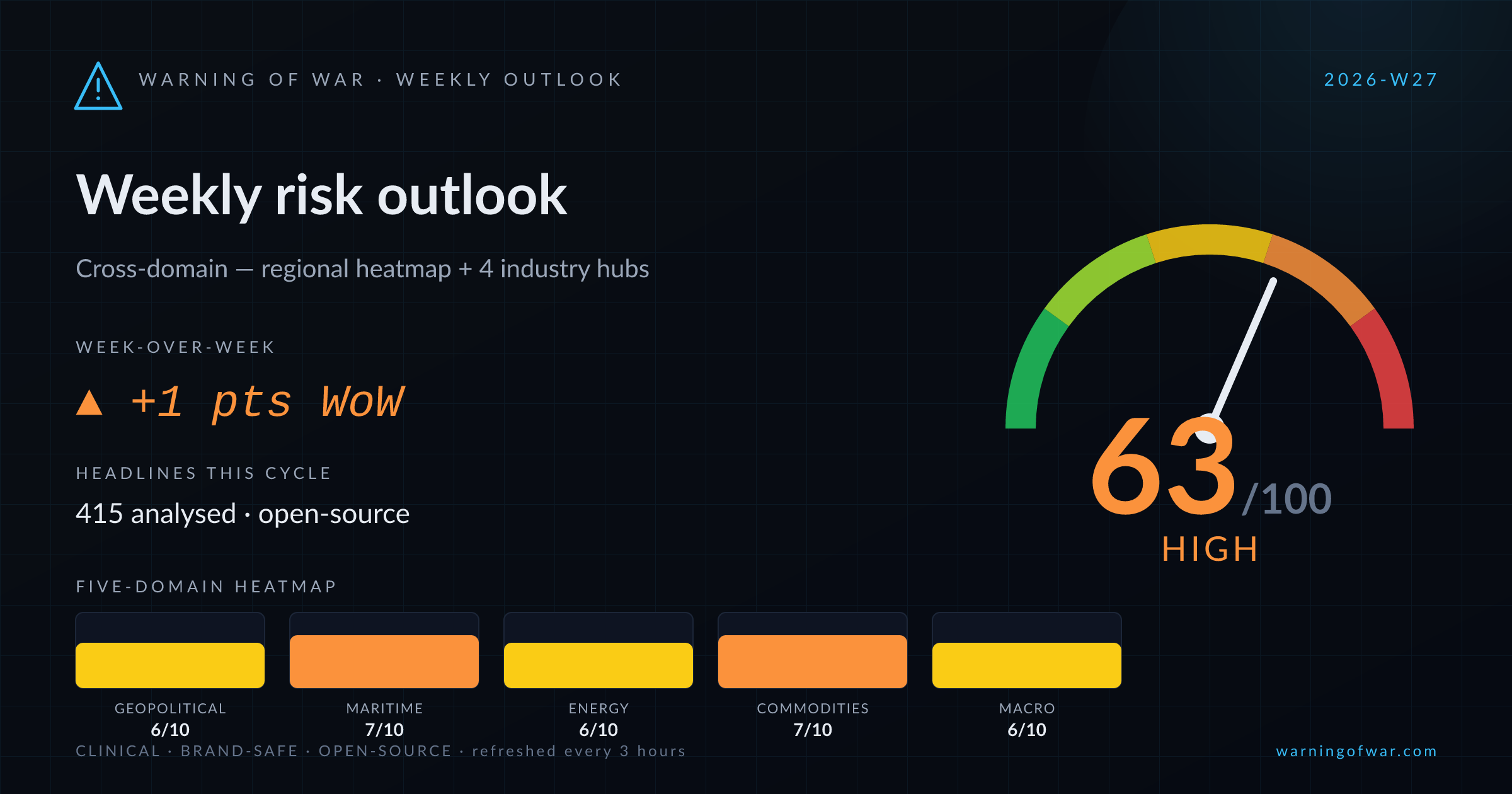

Cross-domain composite holds at 63/100 (High) for the week ahead, blended evenly across the regional heatmap and the maritime, energy, commodities, and macro hubs. Maritime & Supply Chain leads the picture at 65/100; Macro & Sovereign is the least-stressed domain at 60/100. 415 open-source headlines were analysed across all domains this cycle.

| Domain | Score | Band | WoW |

|---|---|---|---|

| Geopolitical & Regional | 6/10 | Elevated | → no change |

| Maritime & Supply Chain | 7/10 | High | ▲ +1 |

| Energy Markets | 6/10 | Elevated | ▼ -1 |

| Commodities & Materials | 7/10 | High | → no change |

| Macro & Sovereign | 6/10 | Elevated | → no change |

→ no change

Regional risk is concentrated in Middle East, South America, North America. The cross-region composite sits at 62/100, blended from maritime, energy, commodities, and macro exposure across 7 monitored regions.

Underlying signals

Headlines this cycle

▲ +1 WoW

The Strait of Hormuz remains the dominant commercial risk vector this cycle. Fresh vessel attacks and renewed U.S.-Iran exchanges have suppressed transit volumes to sub-50% of pre-conflict levels, with IMO estimating residual mine threats constraining underwriter appetite. War-risk insurance premiums are elevated. Oman's signalling of potential transit fees adds a structural cost layer. VLCC loadings at Saudi Arabia's key Gulf terminal have resumed after a four-month suspension. Singapore VLSFO inventories contracted 18% through June, tightening bunker supply in Asia-Pacific. Norwegian offshore drilling faces operational disruption from an escalating labour lockout. LNG shipping rates are trending lower as West-to-East arbitrage closes.

Underlying signals

Headlines this cycle

▼ -1 WoW

Global energy markets are navigating simultaneous stress across crude, LNG, and refining this cycle. Strait of Hormuz transit risk has resurfaced, prompting Pakistan to seek emergency spot LNG and crude tanker insurance premiums to rise. Russian refining capacity has been materially impaired across 50+ regions, tightening domestic product supply. Arctic LNG 2 continues eastward shadow-fleet routing despite OFAC/EU sanctions. Middle East crude output has rebounded toward 15 million bpd post-ceasefire. WTI is oscillating around the $70 threshold, with Brent testing $73. OPEC+ cohesion is fraying as Gulf producers signal extracartel output routing. Indonesia has capped industrial LNG at $13/MMBTU to protect manufacturing employment.

Underlying signals

Headlines this cycle

→ no change

This cycle presents elevated commercial pressure across multiple commodity verticals. Copper markets are directionally bullish — Jefferies and Goldman Sachs revised forecasts upward, while Chinese smelters resist spot-indexed ore pricing at SHFE-linked benchmarks. Graphite project advancement at Blencowe (Uganda) and International Graphite signals critical-mineral supply-chain build-out. Fortescue faces iron ore margin compression. India's kharif season fertilizer intake via Hormuz is secured. Egypt's new 10% nitrogen-fertilizer export duty and Kazakhstan's wheat-import ban tighten regional grain and fertilizer trade flows. A tanker incident near the Middle East Strait tightens freight and oil-linked input costs.

Underlying signals

Headlines this cycle

→ no change

Global macro conditions this cycle are characterized by elevated but contained stress across multiple axes. Ethiopia has reached a preliminary Eurobond restructuring agreement with bondholders, while Nigeria advances a fresh Eurobond offering and Egypt progresses IMF-backed privatizations. Fed Governor Williams reaffirms a hold-oriented stance, while the BoE's Pill signals Brexit-amplified inflation persistence. The PBOC has debuted a new overnight liquidity operation. Strait of Hormuz shipping disruption is pressuring energy trade flows and BOP dynamics across oil-importing sovereigns. The BIS has flagged systemic risks from AI-sector leverage and stablecoin proliferation. India's sovereign rating outlook remains stable per Moody's despite fiscal headroom consumption.

Underlying signals

Headlines this cycle

| Event | Domain | Status | Description |

|---|---|---|---|

| Russia Arctic LNG eastward diversion | energy | ACTIVE | Russian operators are rerouting Arctic LNG volumes to Asian markets under sanctions pressure, structurally reducing spot LNG supply available to European import terminals and supporting TTF price floors. |

| Baltic Sea armed vessel transit | maritime | ACTIVE | A Russian gas vessel reported to be transiting the Baltic Sea under armed escort elevates war-risk insurance assessments and compliance screening requirements for maritime operators on Nordic-Baltic routes. |

| Russia gasoline & aviation fuel export ban | energy | ACTIVE | Russia's government-imposed ban on gasoline and aviation fuel exports tightens global refined product supply, supporting European refinery margins and regional jet fuel spot pricing. |

| Strait of Hormuz Naval Mine Hazard | maritime | ACTIVE | IMO estimates approximately 80 naval mines remain present in or proximate to the Strait of Hormuz, constraining commercial vessel transit and sustaining elevated war-risk insurance premiums across all transiting vessel classes. |

| Iranian Cyberattack Escalation on Israeli Infrastructure | macro | ACTIVE | Israeli cyber authorities report a significant surge in Iranian cyberattack activity targeting Israeli digital and industrial infrastructure, elevating operational risk for enterprise IT systems and financial institutions with Israeli exposure. |

| Global Ocean Freight Rate Spike | maritime | ACTIVE | US tariff-driven cargo front-loading has pushed global ocean shipping rates to a two-year high, increasing import landed costs across North American supply chains. |

The week ahead is led by Maritime & Supply Chain and Commodities & Materials risk. Detailed five-axis decompositions follow in this week's sector deep dives — Maritime on Tuesday, Commodities and Energy on Wednesday, and Macro on Thursday. This outlook synthesises the live regional heatmap with all four industry hubs, refreshed every three hours from open-source signals.