Critical Minerals & Rare Earths

7/10High

Ex-China rare earth re-shoring accelerates as Indonesia's nickel-nationalism framework faces structural erosion and lithium industry gatherings signal heightened investor focus.

WEEKLY REPORT · 2026-W25 · Jun 15 – Jun 21, 2026

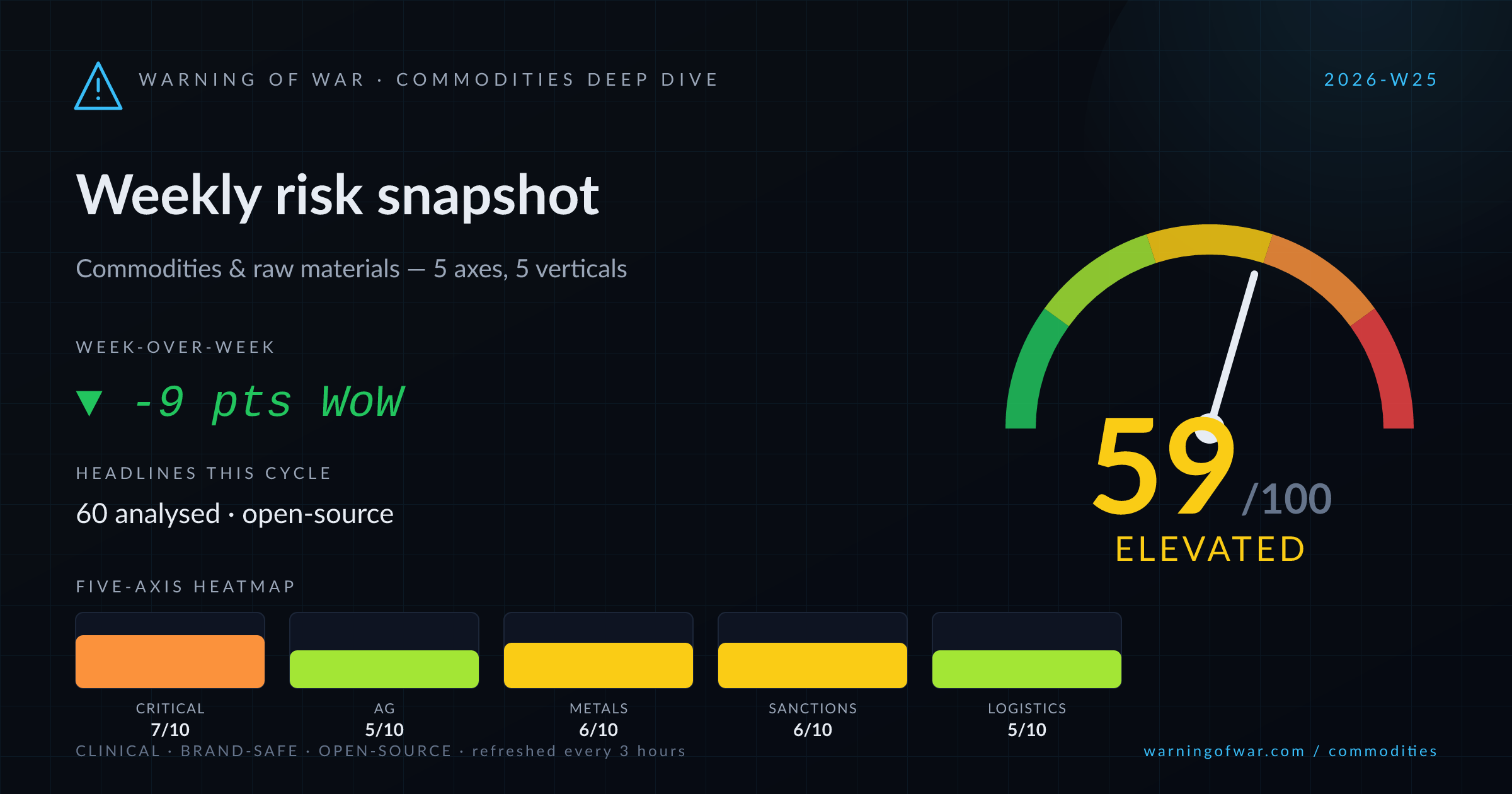

Weekly commodities & raw materials risk snapshot — composite 59/100 (Elevated), ◆ first weekly snapshot.

Critical minerals supply chains are under active strategic realignment: Nickel Industries (ASX: NIC) posted a near-5% share price surge, Indonesia's nickel-nationalism policy framework faces structural pressure from Chinese processing dominance, and Paladin is expanding ex-China rare-earth recovery nodes in South Korea and the Netherlands. Rio Tinto's Oyu Tolgoi copper export corridor in Mongolia faces a protest-driven operational blockade. Iron ore has breached the $100/t floor on abundant supply and subdued Chinese steel demand, while BHP and Rio Tinto pivot iron ore marketing toward Indian steel growth. An interim US–Iran accord is easing Hormuz transit risk, softening wheat and Middle East crude benchmarks, and loosening fertilizer-flow logistics.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

High

Ex-China rare earth re-shoring accelerates as Indonesia's nickel-nationalism framework faces structural erosion and lithium industry gatherings signal heightened investor focus.

Elevated

Global wheat prices are softening on new-harvest supply arrivals and easing Hormuz transit risk, while corn trades near key CBOT resistance levels amid weather and acreage uncertainty.

Elevated

Cocoa prices are retreating sharply — described by Tony's Chocolonely as a 'massive blow' to margins — while climate-driven coffee price appreciation is attracting new corporate farming entrants.

High

Iron ore has broken below $100/t on abundant supply and a clouded Chinese demand outlook, copper faces a protest-driven export blockade at Rio Tinto's Oyu Tolgoi, and steel benchmarks are at two-month lows.

Elevated

Fertilizer prices are declining but the timing offers limited benefit to US agricultural users already past peak application windows, with Hormuz easing set to improve ammonia and urea logistics.

Protesters have blocked copper export shipments from Rio Tinto's Oyu Tolgoi mine in Mongolia to China, creating a near-term operational tonnage disruption in an already tightening global copper supply outlook.

An interim US–Iran accord and associated tanker movement data indicate a progressive reopening of Hormuz transit lanes, reducing freight risk premiums for Middle East-origin urea, ammonia, and LNG cargoes.

Indonesia's nickel downstream-processing nationalism framework is showing structural erosion as Chinese smelting technology maintains dominant operational control over in-country processing capacity, undermining policy objectives.

Iron ore spot benchmarks have declined below $100/t on abundant seaborne supply and a clouded Chinese steel-demand outlook, with BHP and Rio Tinto redirecting commercial focus toward Indian consumption growth.

Cocoa prices have experienced a significant reversal from recent highs, with manufacturer Tony's Chocolonely characterising the fall as a major commercial setback for supply-chain participants dependent on elevated price floors.

Paladin is advancing allied-supply-chain rare earth recovery infrastructure in South Korea and the Netherlands, reflecting accelerating G7-aligned policy momentum to diversify processing capacity away from Chinese facilities.

Over the next 60–90 days, the dominant commercial theme across commodities markets will be the structural aftermath of Hormuz normalisation: wheat, fertilizer (urea/ammonia), and Middle East crude benchmarks are expected to recalibrate lower as freight risk premiums unwind, benefiting grain importers and downstream fertilizer users while compressing margins for producers in high-cost corridors. Copper supply tightness risks will intensify entering 2026 — the Oyu Tolgoi blockade, broader mine-disruption signals, and accelerating data-centre demand combine to keep LME copper structurally supported despite near-term China demand uncertainty. Iron ore is likely to remain range-bound below $100/t absent a material Chinese infrastructure stimulus announcement, with BHP and Rio Tinto's India pivot providing a longer-dated but not near-term demand offset. In critical minerals, G7 policy alignment on ex-China rare earth and nickel supply chains — visible in Paladin's European/Korean expansion and South Korean presidential G7 agenda items — will drive incremental capital allocation toward allied-supply projects, potentially tightening financing conditions for non-allied processing assets. Cocoa's price reversal warrants monitoring for second-order effects on West African producer revenues and soft-commodity fund positioning.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.