Upstream Oil & Gas

9/10Critical

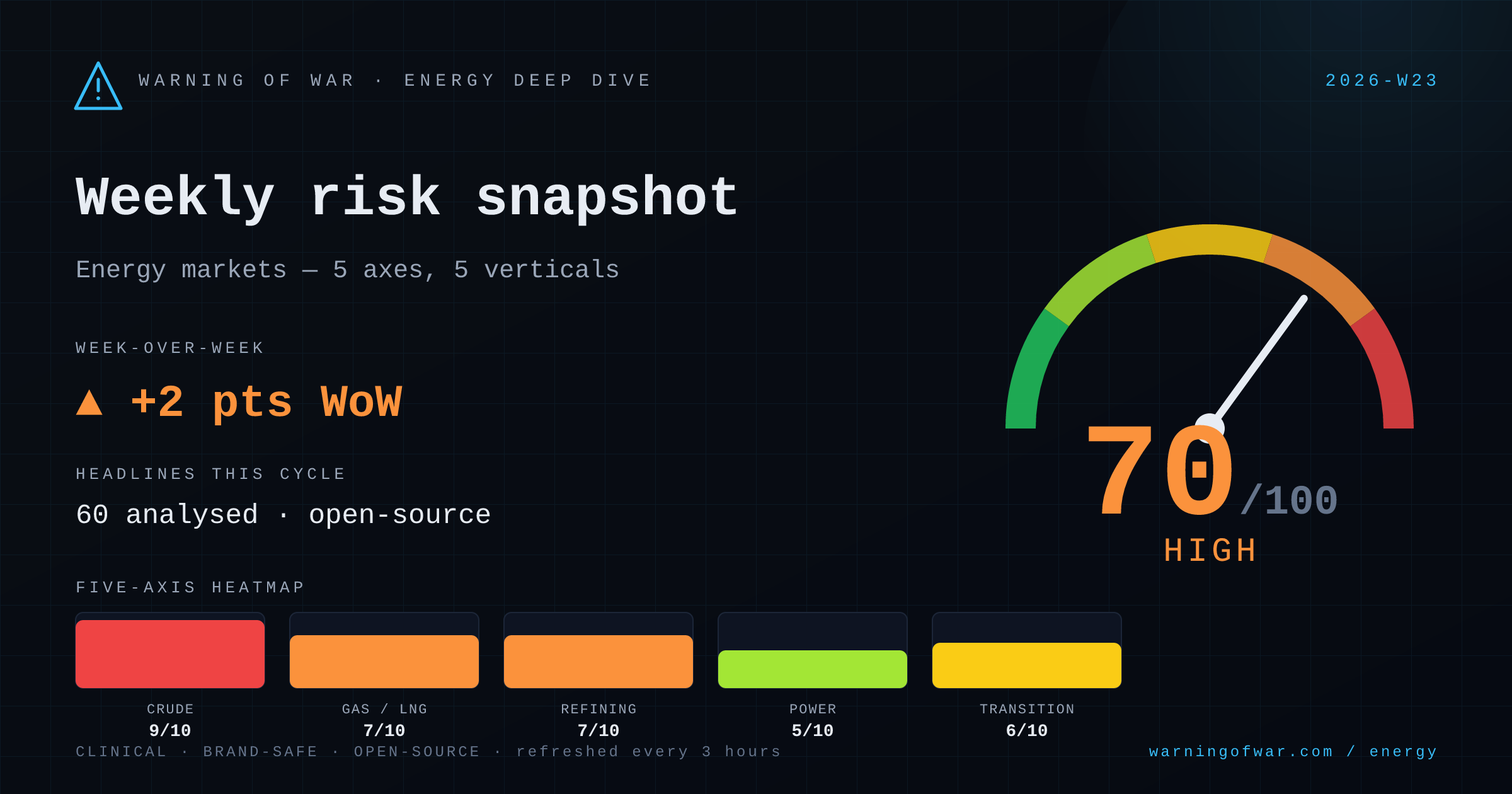

Hormuz closure and Iran-Gulf hostilities push crude toward USD 100/bbl with material rerouting underway.

WEEKLY REPORT · 2026-W23 · Jun 1 – Jun 7, 2026

Weekly energy markets risk snapshot — composite 70/100 (High), ◆ first weekly snapshot.

The Strait of Hormuz closure is the dominant supply-side shock this cycle: Iraq is routing incremental barrels via Kirkuk–Ceyhan to Turkey's Mediterranean coast, while Kharg Island saw its first VLCC call in nearly a month, signalling partial Iranian export resumption under ceasefire fragility. WTI and Brent are pressing toward USD 100/bbl on US inventory drawdown and Iran-Gulf tensions. Russia–Saudi rapprochement is reshaping OPEC+ quota architecture as the UAE exits the bloc. US Secretary Rubio's signal on ending Russian oil sanction waivers adds secondary supply-side risk. The Novoshakhtinsk refinery in Russia sustained Neptune-missile-related unit outages, tightening Russian product export capacity. Centrica–Peyto and INEOS–Marubeni long-term LNG offtake deals point to continued European and Asian gas diversification away from Russian supply.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

Critical

Hormuz closure and Iran-Gulf hostilities push crude toward USD 100/bbl with material rerouting underway.

High

European and Asian LNG diversification accelerates via multi-year Canadian and UK offtake deals amid ongoing Russian gas sanction risk.

High

Novoshakhtinsk refinery unit outages and Middle East product-flow disruption tighten global distillate and product margins.

Elevated

EU data-centre efficiency mandates and India battery storage tenders signal demand-side and grid-balancing pressures.

High

IRA-era and EU transition investment flows active, but Brazil grid-curtailment risk freezes USD 1 billion in solar investment.

No named disruption events reported in this cycle.

Outlook pending.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.