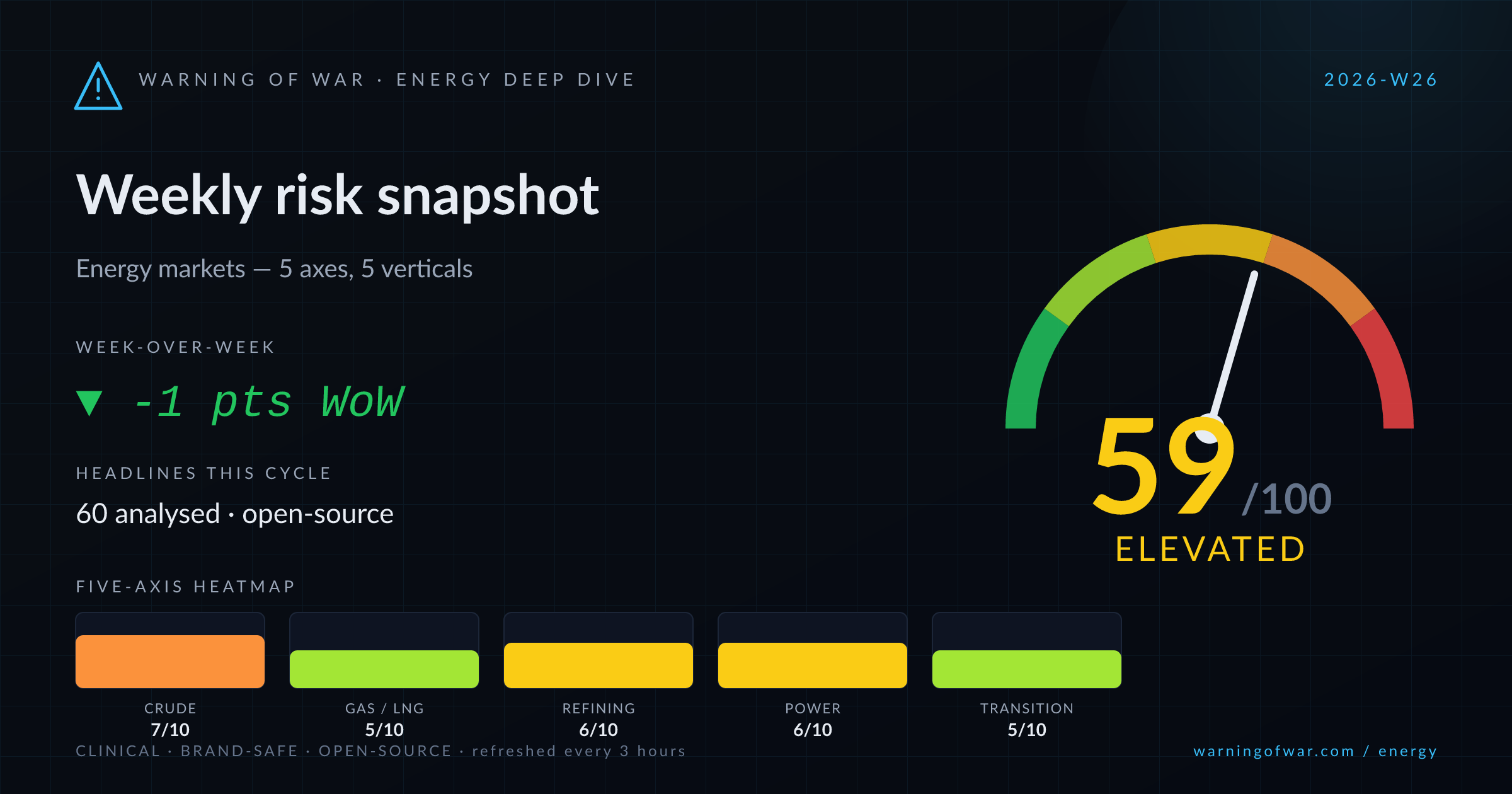

Upstream Oil & Gas

7/10High

Brent breaks below $75 as Hormuz normalises and Middle East supply surges, compressing upstream netbacks.

WEEKLY REPORT · 2026-W26 · Jun 22 – Jun 28, 2026

Weekly energy markets risk snapshot — composite 59/100 (Elevated), ▼ -1 pts WoW.

Global crude markets face simultaneous bearish pressure from Hormuz transit normalisation — stranded VLCC fleets re-entering supply — and Middle East production acceleration, pushing Brent below $75 and WTI to its lowest since March. OPEC cohesion is structurally weakening with UAE exit rhetoric threatening a 4-percentage-point share drop per EIA modelling. The Moscow Kapotnya refinery remains offline through at least 2026, forcing Russia to source gasoline imports from India and Kazakhstan. ExxonMobil's Antwerp refinery faces a full shutdown 29 June–3 July due to labour action. Cheniere's Corpus Christi Train 6 adds incremental US LNG capacity. J.P. Morgan cuts H2-2026 Brent forecasts; Dan Yergin anchors fair-value at $70–$85.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

High

Brent breaks below $75 as Hormuz normalises and Middle East supply surges, compressing upstream netbacks.

Elevated

Corpus Christi Train 6 expands US LNG export capacity while a Ukrainian strike on a Russian gas-processing facility near Kazakhstan introduces upstream gas supply risk.

High

ExxonMobil Antwerp shutdown, Moscow refinery extended offline status, and Chinese teapot run-rate lows collectively tighten global refined product supply.

High

European grid stress materialises as summer heatwave drives power outages in France and Italy, while AI-driven load-growth signals long-run grid capacity expansion requirements.

Elevated

EU Hydrogen Bank fourth auction, Brazil's clean hydrogen subsidy programme, Turkey offshore wind rules, and First Solar capacity expansion mark steady but incremental transition-policy momentum.

US-Iran MOU framework has enabled stranded VLCC fleets to resume Hormuz transits, releasing backlogged Persian Gulf crude volumes into physical markets and flipping the key oil time-spread to contango.

UAE's potential departure from OPEC could reduce the organisation's global crude market share from 35% to 31% per EIA modelling, materially altering OPEC+ quota-management and price-support architecture.

A labour strike forces full output cessation at ExxonMobil's Antwerp refinery from 29 June to 3 July, removing ARA-hub refining capacity and providing near-term crack-spread support for diesel and naphtha.

The Moscow Kapotnya refinery is assessed as unlikely to resume operations before end-2026, potentially extending offline status to 2027, forcing Russia to source gasoline imports from India and Kazakhstan to offset a ~25% domestic production decline.

Ukraine has struck a Russian gas-processing facility near the Kazakhstan border, introducing operational uncertainty for Central Asian pipeline gas flows and Russian upstream gas production volumes.

An intense summer heatwave across Europe has triggered power outages in France and Naples, Italy, exposing peak-demand vulnerability in transmission infrastructure and elevating near-term grid reliability risk for European utilities.

Over the 60–90 day forward window, crude oil price action will hinge on the durability of the US-Iran MOU and whether Hormuz transit volumes normalise fully or face renewed restriction — any re-escalation would rapidly reverse the current contango structure and retest $80+ Brent levels. OPEC+ cohesion risk is the dominant structural overhang: a formalised UAE exit or accelerated quota-exempt production increases could entrench sub-$75 Brent, pressuring upstream E&P capex budgets for H2-2026 planning cycles. In refining, the Antwerp restart post-strike and the Russian gasoline import programme from India will be the key margin-directional signals for ARA and Asian product markets respectively, with Chinese teapot utilisation recovery contingent on Beijing export-quota liberalisation. European power grids face continued heatwave-season reliability risk through August, with AI-driven load growth adding a structural demand overhang that capacity markets have not yet priced. On the transition front, the EU Hydrogen Bank fourth auction and Brazil's 2027 clean hydrogen programme will advance project pipelines but near-term commercial impact remains limited pending final subsidy structures.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.