Upstream Oil & Gas

6/10High

WTI sub-$70 as OPEC+ accelerates output increases and US-Iran diplomacy tempers Middle East risk premium.

WEEKLY REPORT · 2026-W27 · Jun 29 – Jul 5, 2026

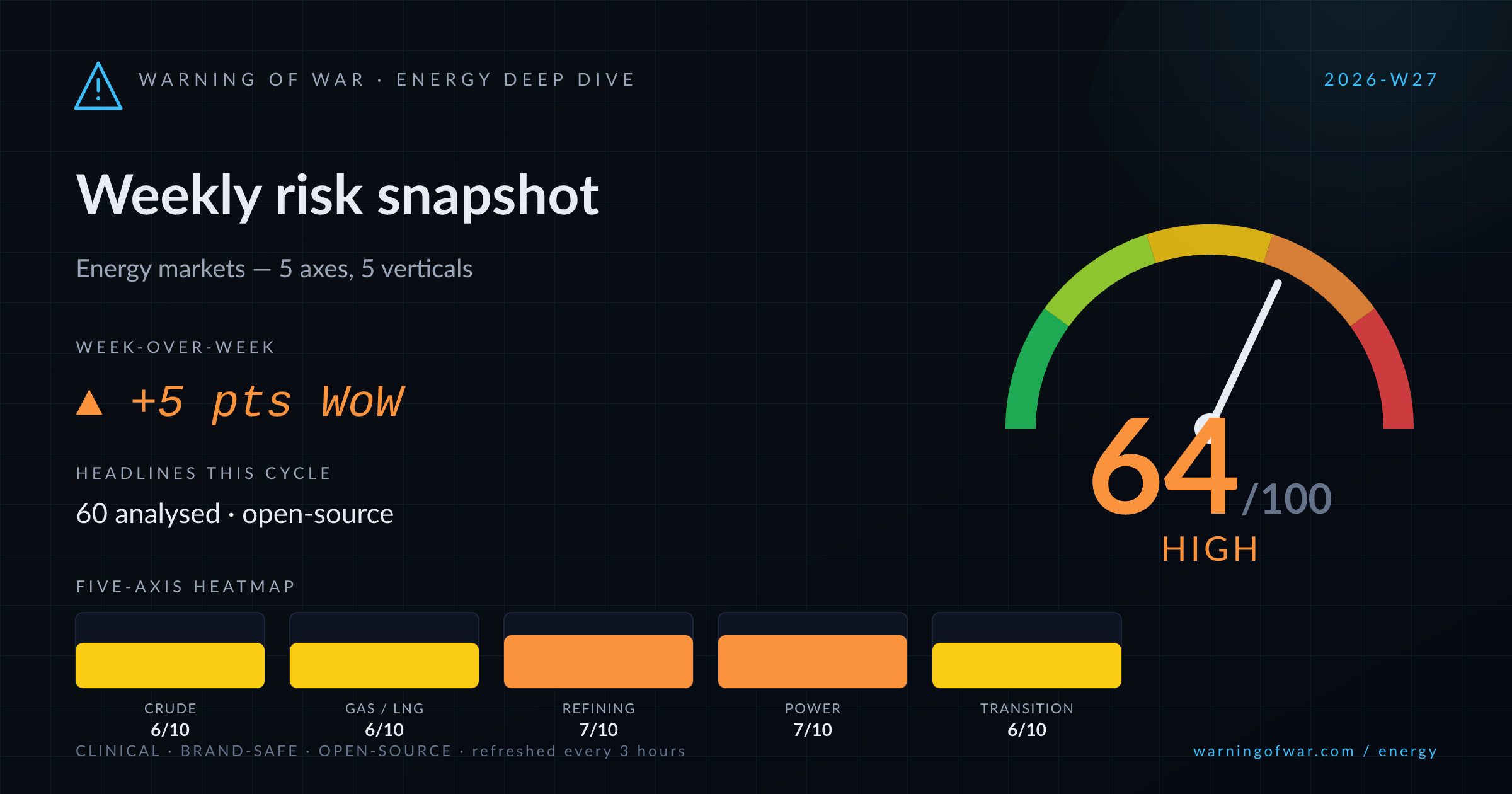

Weekly energy markets risk snapshot — composite 64/100 (High), ◆ first weekly snapshot.

WTI has slipped below $70/bbl — its weakest level since late February — as OPEC+ prepares a further 188,000 bpd output increase for August, Saudi Aramco moves rare spot cargoes, and US-Iran diplomatic talks in Doha ease geopolitical risk premiums. A 3.8 million-barrel EIA drawdown partially offsets bearish supply pressure. Russia's Slavyansk-na-Kubani and Ufa refinery complexes have sustained operational disruptions, tightening Russian product balances and prompting Indian gasoline imports. Iraq's West Qurna 2 NDA with Chevron signals near-term upstream capacity ambitions. JERA's new Singapore trading arm and the India-Japan LNG security pact signal structural LNG demand growth in Asia.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

High

WTI sub-$70 as OPEC+ accelerates output increases and US-Iran diplomacy tempers Middle East risk premium.

High

Asian LNG demand structurally rising; JERA launches Singapore trading arm and India-Japan ink LNG security pact.

High

Russian refinery operational disruptions tighten domestic product balances; Moscow sourcing gasoline imports from India.

High

PJM — the US's largest grid — issues record-demand warnings as summer load surge tests reserve margins.

High

Hydrogen FIDs, offshore wind auctions, and UK solar capacity ambitions mark an active policy and investment cycle.

Kyiv's deep-strike operations have disrupted eleven Russian refinery complexes — including Slavyansk-na-Kubani and Ufa — within a single month, reducing available run rates and triggering Russian gasoline procurement from India.

OPEC+ is likely to approve an additional 188,000 bpd output quota increase for August, continuing the accelerated unwind of voluntary production cuts and adding further downward price pressure to WTI and Brent.

WTI crude has declined below $70/bbl to its lowest level since late February, driven by OPEC+ supply expansion signals, Saudi Aramco spot sales, and easing US-Iran geopolitical risk premium.

PJM, the US's largest grid operator, has issued formal operational warnings ahead of projected record summer electricity demand, raising reserve margin and transmission adequacy concerns across its 13-state footprint.

US and Iran are engaged in technical talks in Doha aimed at a peace framework and shipping-lane normalisation, reducing near-term Hormuz risk premium but leaving core nuclear and sanctions disputes unresolved.

Scenario analysis of a potential Hormuz disruption is actively reframing LNG supply routing and contracting strategies through 2027, with Shell noting global LNG trade at 422 million tonnes and demand projected to grow 65% by 2050.

Over the next 60–90 days, crude oil prices face continued downward pressure as OPEC+ executes successive monthly quota increases — each increment approximately 188,000 bpd — while Saudi Aramco actively manages elevated output via spot market sales; WTI is likely to remain range-bound in the $65–$72/bbl corridor absent a breakdown in US-Iran Doha talks or an unexpected geopolitical supply shock at Hormuz. Russian refining capacity will remain constrained by ongoing operational disruptions, sustaining India–Russia product trade flows and marginally tightening regional diesel and naphtha balances outside Russia. In the LNG vertical, JERA GES's Singapore operations and the India-Japan security pact will accelerate Asian offtake consolidation and long-term contracting activity, supporting JKM price stability into the winter restock cycle. PJM's record demand warnings signal that US power capacity margins and merchant power prices will face acute stress through the August peak-load window, providing a near-term uplift signal for gas-fired generation dispatch and Henry Hub spot prices. On policy, EU ETS overhaul negotiations, the UK solar CfD auction cycle, and South Korea's offshore wind fixed-price contracts will be key watch points for renewable investment pipeline visibility in Q3–Q4 2025.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.