Sovereign Credit & Debt

7/10High

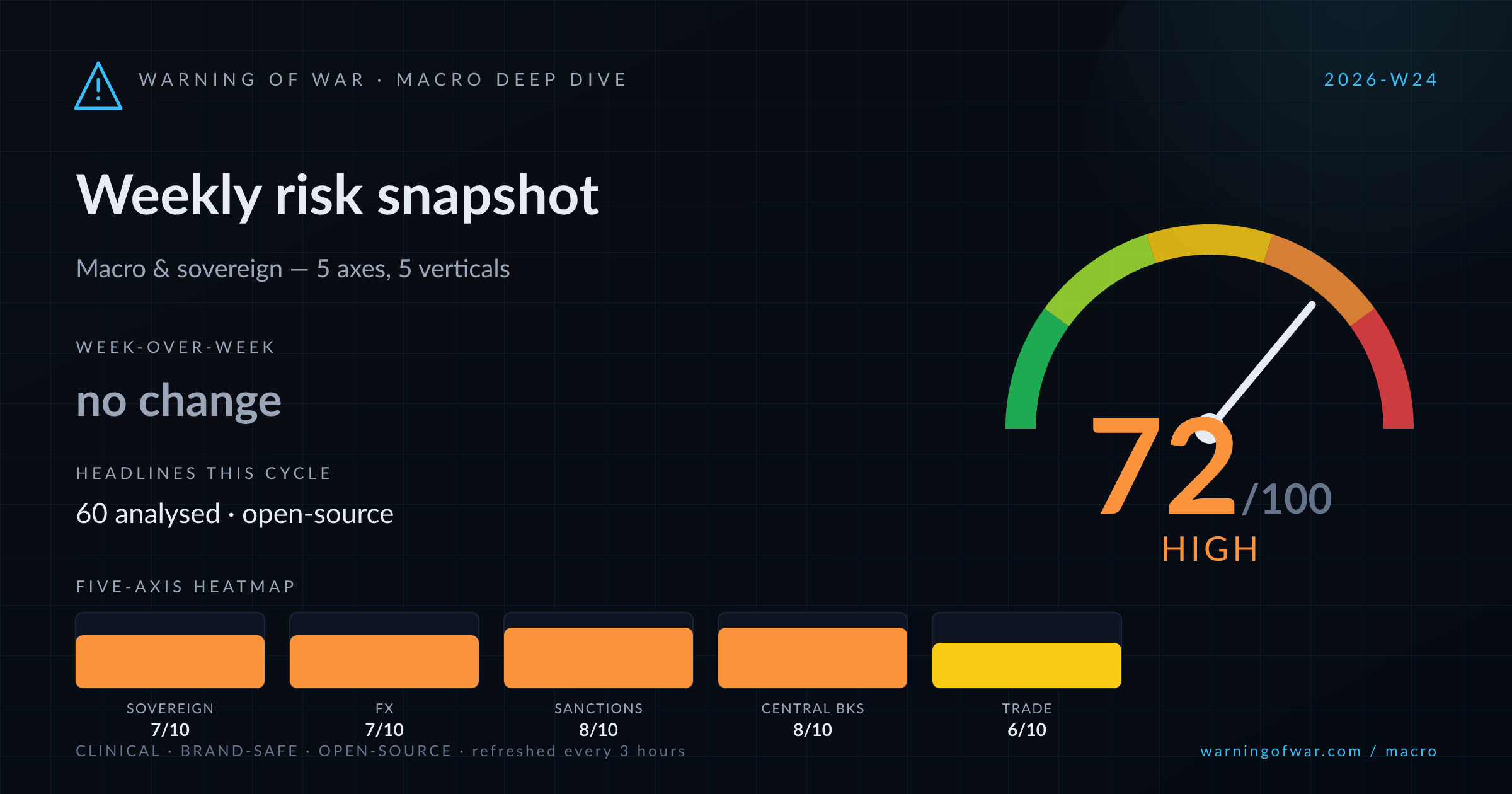

Fitch's deteriorating global sovereign outlook, Indonesian fiscal stress, and Nigeria's IMF Article IV consultation signal broad EM credit pressure.

WEEKLY REPORT · 2026-W24 · Jun 8 – Jun 14, 2026

Weekly macroeconomic & sovereign risk snapshot — composite 72/100 (High), ◆ first weekly snapshot.

Global macro risk is materially elevated this cycle. Fitch has revised its 2026 global sovereign outlook to "Deteriorating," citing geopolitical-linked inflation spillovers. The ECB is pricing an insurance rate hike as energy-price pressures broaden across the euro zone. The Bank of Japan faces acute governance uncertainty following Governor Ueda's hospitalization ahead of the June policy meeting. The EU's 21st Russia sanctions package targets cryptocurrency platforms in Georgia and Russian cod imports, while the US has sanctioned 13 Iran-Belarus-China entities supplying the IRGC. Iran's Strait of Hormuz closure announcement compounds oil supply and sovereign-spread risk across multiple emerging-market corridors.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

High

Fitch's deteriorating global sovereign outlook, Indonesian fiscal stress, and Nigeria's IMF Article IV consultation signal broad EM credit pressure.

High

Multiple EM and G10 currency pairs are under simultaneous pressure, with JPY approaching prior intervention thresholds and the Nigerian Naira recording fresh depreciation.

Critical

A convergent multi-regime sanctions escalation — EU's 21st Russia package, new US IRGC-network designations, and an EU court ruling redefining extraterritorial sanctions limits — marks the most active sanctions cycle in recent quarters.

Critical

A rare simultaneous policy-pivot cluster — ECB insurance hike, BoJ governance disruption, Fed rate-hike repricing, and CBSL parliamentary briefings — defines an unusually active G10 and EM central bank cycle.

High

The Iran-linked Strait of Hormuz closure announcement, US emergence as the world's top oil exporter, and China-EU diplomatic cancellations signal material BoP and trade-flow disruption risk.

No named disruption events reported in this cycle.

Outlook pending.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.