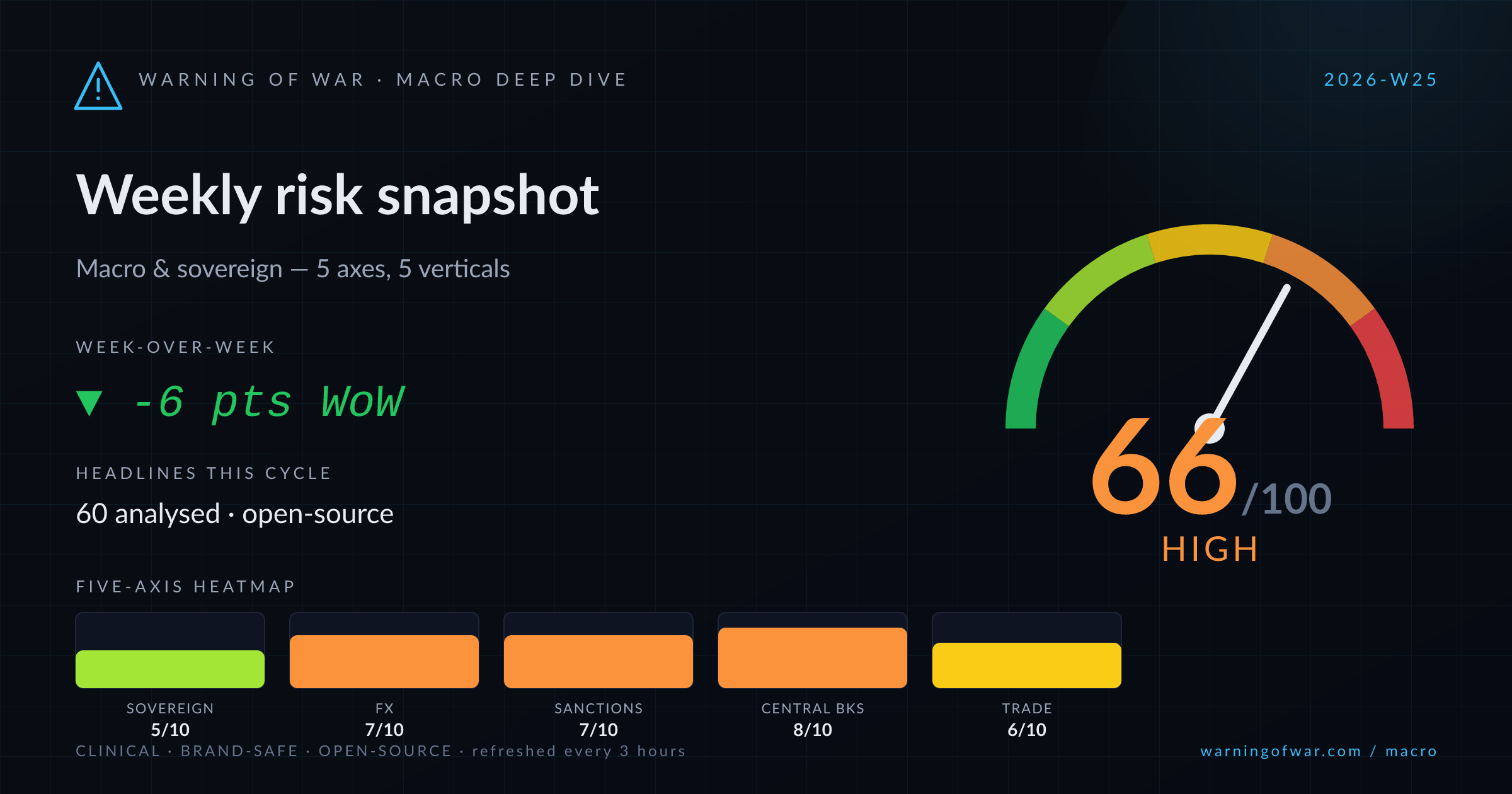

Sovereign Credit & Debt

5/10Elevated

Mixed sovereign signals: Fitch upgrades South Africa and Eskom, Gabon re-enters Eurobond markets, while Jordan advances IMF programme milestones and Iraq's commodity-revenue concentration draws World Bank attention.