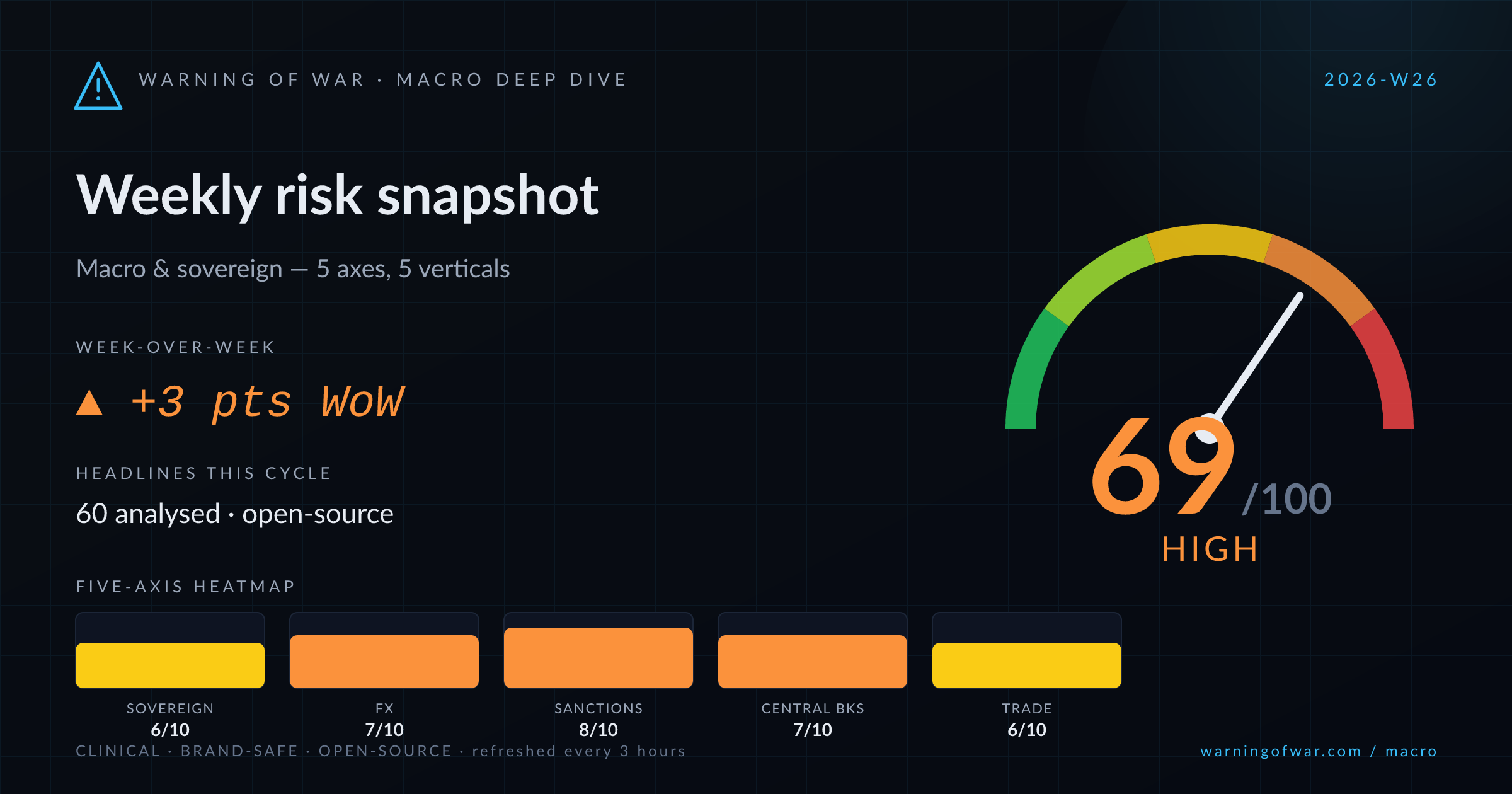

Sovereign Credit & Debt

6/10High

Frontier and emerging-market sovereign stress is rising, led by Moody's negative outlook cut on Gabon, renewed IMF programme approaches, and China's record sovereign Eurobond issuance signalling diversified funding strategy.