Sovereign Credit & Debt

6/10High

Multilateral lending activity is elevated, with IMF and World Bank programs active across Sri Lanka, Ethiopia, Nigeria, Morocco, and Pakistan, reflecting ongoing frontier-market fiscal stress.

WEEKLY REPORT · 2026-W27 · Jun 29 – Jul 5, 2026

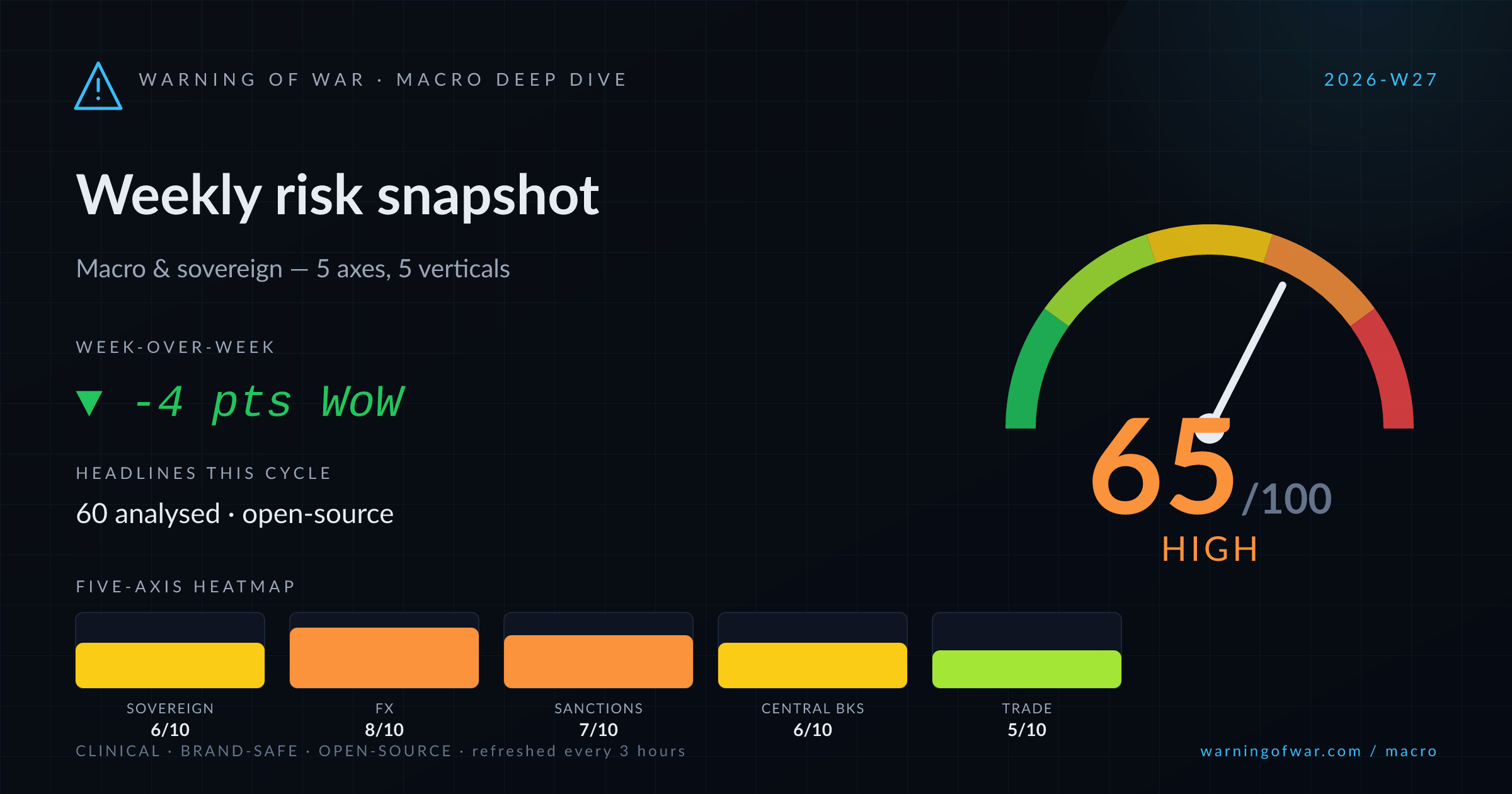

Weekly macroeconomic & sovereign risk snapshot — composite 65/100 (High), ◆ first weekly snapshot.

This cycle's dominant signals are a JPY/USD dislocation to 40-year lows with market speculation targeting 200, a Korean won under pressure from foreign equity outflows despite a 30-month inflation high, and a fragile INR as RBI intervention thins. On sovereign credit, IMF programs for Sri Lanka and Ethiopia are advancing while Nigeria draws fresh World Bank facilities amid rising debt concerns. OFAC has extended its crypto-sanctions perimeter via 134 ISIS-K-linked wallet designations with Tether compliance. ECB policy council is fractured on the next rate move, while incoming Fed Chair Warsh signals balance-sheet tightening and de-emphasises forward guidance. BIS flags systemic AI-investment risk.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

High

Multilateral lending activity is elevated, with IMF and World Bank programs active across Sri Lanka, Ethiopia, Nigeria, Morocco, and Pakistan, reflecting ongoing frontier-market fiscal stress.

Critical

JPY at a 40-year low versus the dollar with market pricing toward 200 threshold, Korean won slipping on foreign equity outflows, Vietnamese dong stabilisation actions, and RBI intervention thinning on INR constitute a broad EM/G10 FX stress event.

High

OFAC has expanded its digital-asset sanctions perimeter with 134 cryptocurrency wallet designations linked to an ISIS-K network, prompting immediate Tether compliance freezes totalling $4.4B across 131 TRON-based wallets.

High

The ECB council is divided on its next rate move as oil-driven disinflation deepens, while incoming Fed Chair Warsh signals balance-sheet reduction priority and de-emphasises forward guidance, and the Bank of England advances leverage limits on hedge funds.

Elevated

South Korea's record trade surplus is colliding with a won selloff driven by foreign capital outflows, while Nigeria's federal government implements tariff reductions and U.S.-Saudi diplomatic friction over Hormuz access introduces a regional energy-trade risk premium.

The Japanese yen has reached a 40-year low versus the U.S. dollar, with market participants actively modelling worst-case scenarios and short sellers increasing directional bets, raising the probability of Bank of Japan or Ministry of Finance FX intervention.

U.S. Treasury OFAC has designated 134 cryptocurrency wallets linked to an ISIS-K financing network, with Tether executing compliance freezes on 131 TRON wallets representing $4.4B in USDT — a record digital-asset sanctions enforcement action.

ECB governing council members are publicly diverging on the direction of the next rate move as oil-price-driven disinflation erodes the hawkish case, introducing forward-guidance uncertainty into Eurozone sovereign spread pricing.

South Korea's Korean won is declining against the U.S. dollar on sustained foreign-investor equity outflows even as domestic CPI accelerates to a 30-month high, creating a policy dilemma for the Bank of Korea between currency defence and rate normalisation.

Nigeria has drawn over $3B in new World Bank facilities this cycle, with press commentary flagging rising debt-sustainability concerns against a backdrop of ongoing fiscal reforms under the Tinubu administration.

A reported dispute between the U.S. and Saudi Arabia over Strait of Hormuz access policy is introducing a geopolitical risk premium into energy-trade flows, affecting base-metals pricing and broader commodity import cost assumptions for Asian economies.

Over the next 60–90 days, the dominant macro risk vector remains the JPY dislocation: absent a coordinated Bank of Japan and Ministry of Finance intervention, USD/JPY positioning toward the 200 level would propagate cross-asset volatility, tighten financial conditions for EM sovereigns with USD-denominated debt, and amplify capital-outflow pressure on the Korean won, Indonesian rupiah — where Fitch has flagged rising FX-buffer stress — and the Indian rupee. The Fed's balance-sheet reduction agenda under Chair Warsh, if telegraphed aggressively, will reinforce dollar strength and compress EM FX headroom further. The ECB's internal policy fracture risks Eurozone sovereign-spread widening if a rate-cut is delayed while oil disinflation continues. On the sanctions front, OFAC's crypto-wallet enforcement action signals an accelerating compliance perimeter for stablecoin issuers and DeFi infrastructure, with secondary-sanctions risk likely to be explicitly extended in forthcoming OFAC guidance. Nigeria's debt trajectory warrants close monitoring given the scale of fresh multilateral borrowing against a backdrop of elevated debt-service ratios. U.S.-Iran talks via Qatar and the Hormuz access dispute with Saudi Arabia will jointly determine whether an energy-trade risk premium re-prices crude and LNG freight for Asian importers in Q3 2026.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.