Tanker Markets

9/10Critical

Hormuz toll regime, VLCC detention releases, soaring resale premiums, and VLGC rate spike define a critically stressed tanker market.

WEEKLY REPORT · 2026-W21 · May 18 – May 24, 2026

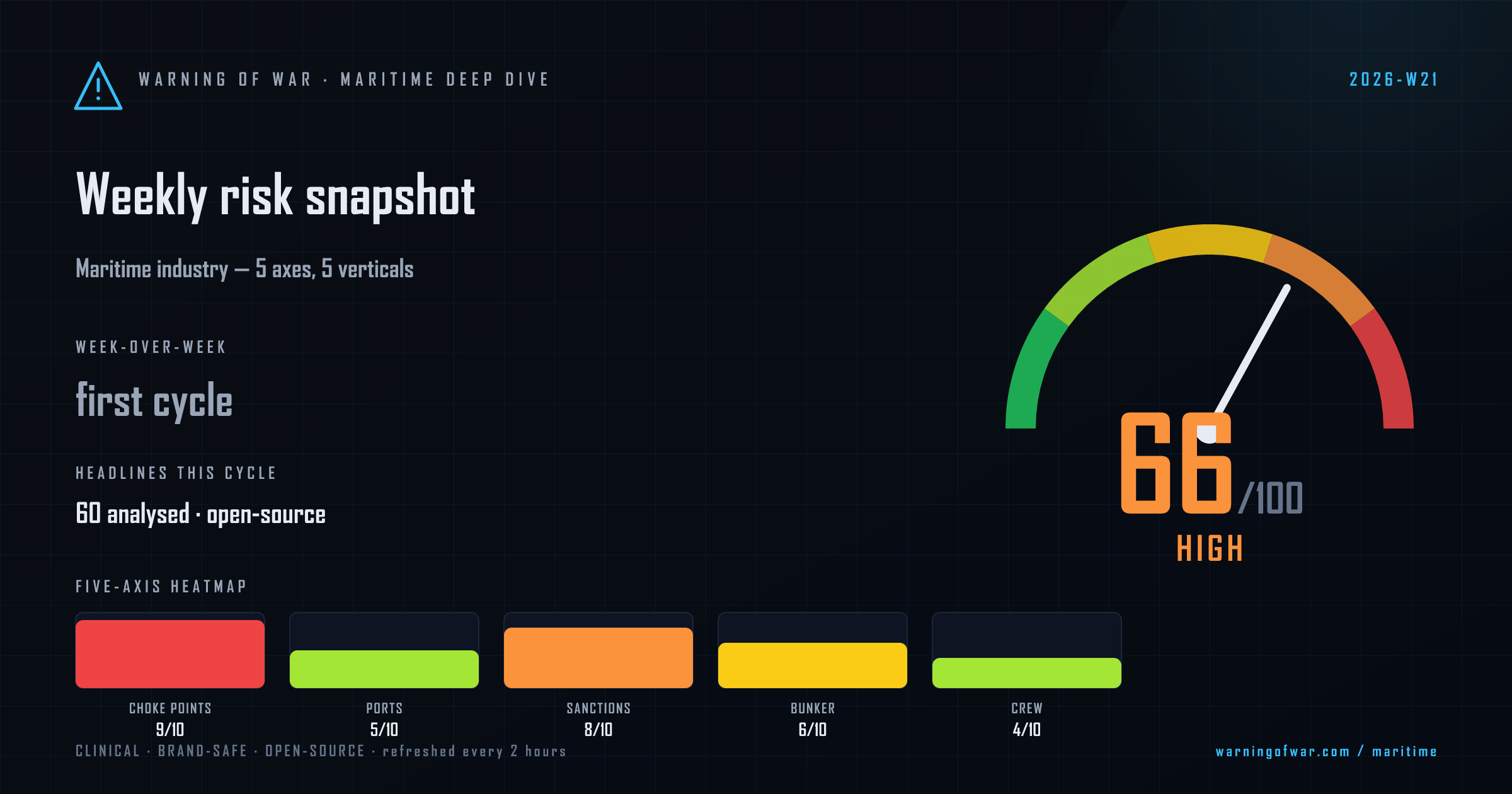

Weekly maritime industry risk snapshot — composite 66/100 (High), ◆ first weekly snapshot.

The Strait of Hormuz dominates this scoring cycle as the single most consequential commercial-risk vector in global shipping. Iran's newly established Persian Gulf Strait Authority (PGSA) has formalised a state-administered transit-toll regime, with per-voyage fees reported at up to USD 2 million settled in CNY and Bitcoin. Three VLCCs detained for over two months have begun exiting the strait, and Iran claims to have coordinated passage of 26 vessels in a single 24-hour window. U.S. naval forces have boarded multiple Iranian-flagged tankers, sustaining elevated war-risk premiums across the Persian Gulf corridor. Tanker resale premiums are soaring as owners accelerate delivery timelines. VLGC spot rates have reached USD 6 million per month on scarce availability. On dry-bulk, the Baltic Dry Index recorded a fourth consecutive decline. ARA bunker fuel terminals report loading delays that have stretched lead times to approximately 10 days. The UAE's Hormuz-bypass crude pipeline reached 50% completion. Indonesia has imposed new commodity export controls, adding compliance complexity for dry-bulk and container operators across Southeast Asian trade lanes.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

Critical

Hormuz toll regime, VLCC detention releases, soaring resale premiums, and VLGC rate spike define a critically stressed tanker market.

Elevated

Baltic Dry Index on a four-session losing streak; Hormuz-related bauxite trade-flow disruption and Indonesian export controls add route complexity.

High

Asia-Europe freight cost volatility intensifies as Cape of Good Hope rerouting persists and Hormuz disruption prolongs schedule unreliability.

Elevated

OSV order pipeline remains structurally low despite elevated energy prices; offshore-wind CTV segment continues incremental fleet expansion.

Guarded

Yacht-leisure segment shows no material disruption signals this cycle; Piraeus port development and Belfast investment plan provide positive infrastructure backdrop.

Iran's newly established Persian Gulf Strait Authority has formalised a state-administered per-transit fee structure of up to USD 2 million per voyage, settled in CNY and Bitcoin, with bilateral carve-outs for select flag states — fundamentally altering the commercial calculus for all vessels transiting the Strait of Hormuz.

Three VLCCs carrying approximately 6 million barrels of Middle East crude were detained in the Persian Gulf for over two months before commencing southbound Hormuz transit, with a South Korean tanker completing the first fee-free exit in 81 days under diplomatic coordination.

U.S. naval forces have conducted multiple boardings of Iranian-flagged oil tankers suspected of circumventing enforcement measures, sustaining elevated war-risk insurance premiums across Persian Gulf tanker routing.

Bunker fuel loading lead times at ARA hub terminals have approximately doubled to 10 days, tightening VLSFO supply availability and adding cost and scheduling uncertainty for vessel operators bunkering in Northwest Europe.

The Baltic Dry Index fell for a fourth consecutive session to 3,005 points — its lowest level since mid-May 2026 — with Capesize softness leading the decline amid shifting bauxite trade flows and Indonesia export-control headwinds.

Persistent Cape of Good Hope rerouting driven by Middle East corridor instability is generating material total-landed-cost uncertainty on Asia-Europe lanes, with freight forwarders increasingly unable to lock in final costs at the point of booking.

Outlook pending.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.