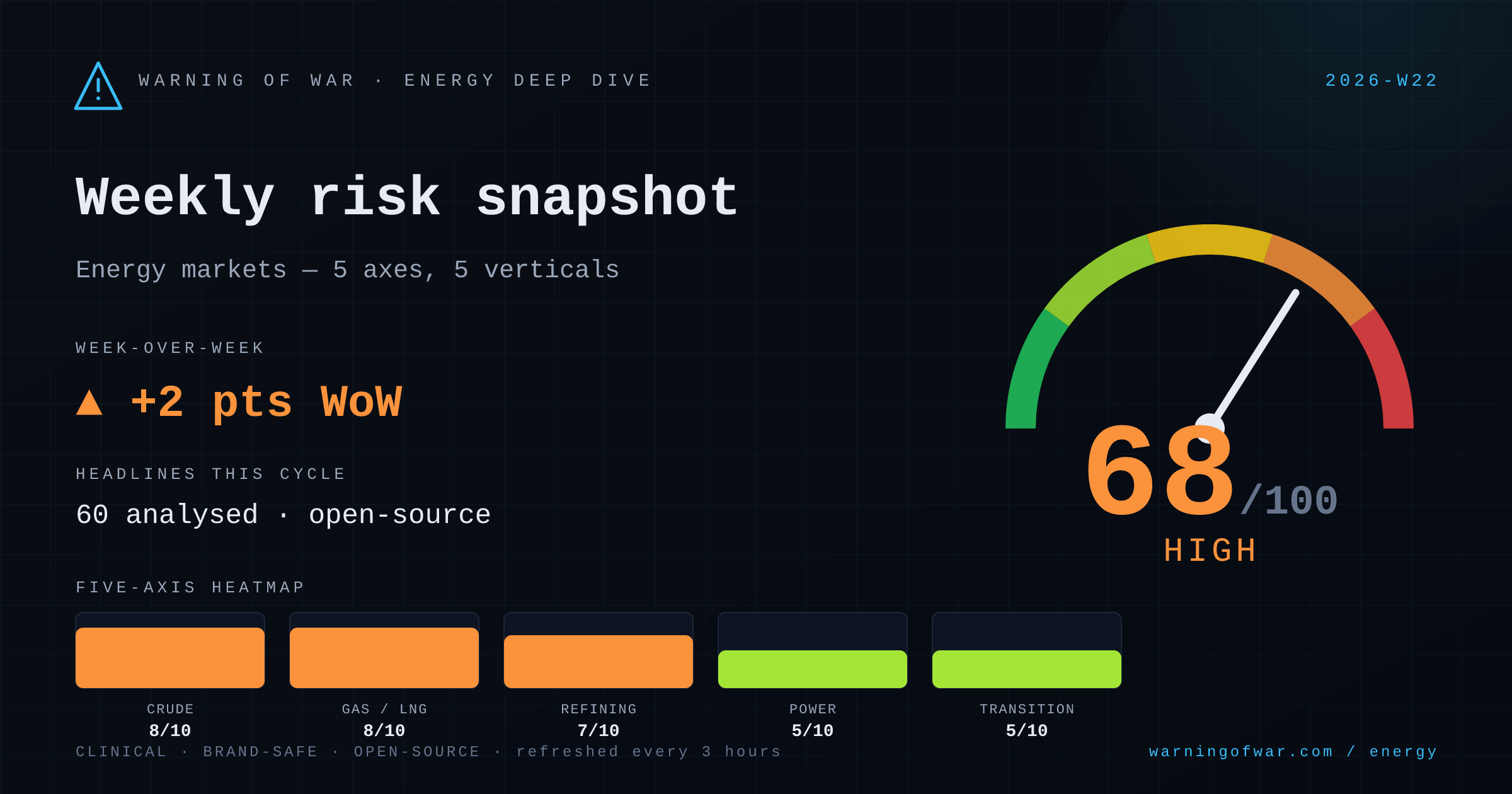

Upstream Oil & Gas

8/10Critical

Hormuz closure risk and SPR diversions dominate upstream crude flow dynamics this cycle.

WEEKLY REPORT · 2026-W22 · May 25 – May 31, 2026

Weekly energy markets risk snapshot — composite 68/100 (High), ◆ first weekly snapshot.

The Strait of Hormuz closure—driven by U.S.-Iran hostilities—is the dominant commercial signal this cycle, with Brent and WTI pricing in a prolonged-disruption premium and ADNOC deploying tankers in "dark mode." The U.S. SPR has dispatched a rare Asian cargo, reshaping short-haul trade flows. Russia's Tuapse refinery has sustained its fifth successive drone strike, compressing Urals-grade crack spreads. UK Ofgem's 13% price-cap uplift from July 1 reflects wholesale gas pass-through from Middle East risk. CNOOC's Kenli 10-2 Bohai Sea field entering full production adds modest incremental supply. Canada-Germany LNG offtake alignment accelerates European de-Russification of gas supply.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

Critical

Hormuz closure risk and SPR diversions dominate upstream crude flow dynamics this cycle.

Critical

Hormuz closure scenarios and European supply complacency are driving acute LNG market uncertainty.

High

Repeated drone strikes on Tuapse refinery and product-market stress are the key refining signals this cycle.

Elevated

UK energy bill shock and a Sumatra blackout highlight gas-to-power price pass-through and grid reliability risks.

Elevated

EV outlook, solar portfolio expansion, and US-EU policy cross-currents define a mixed transition landscape.

No named disruption events reported in this cycle.

Outlook pending.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.