Tanker Markets

8/10Critical

Hormuz transit recovery is driving a partial VLCC rate rebound, but elevated war-risk premiums and shadow-fleet compliance dynamics keep the sector at high stress.

WEEKLY REPORT · 2026-W27 · Jun 29 – Jul 5, 2026

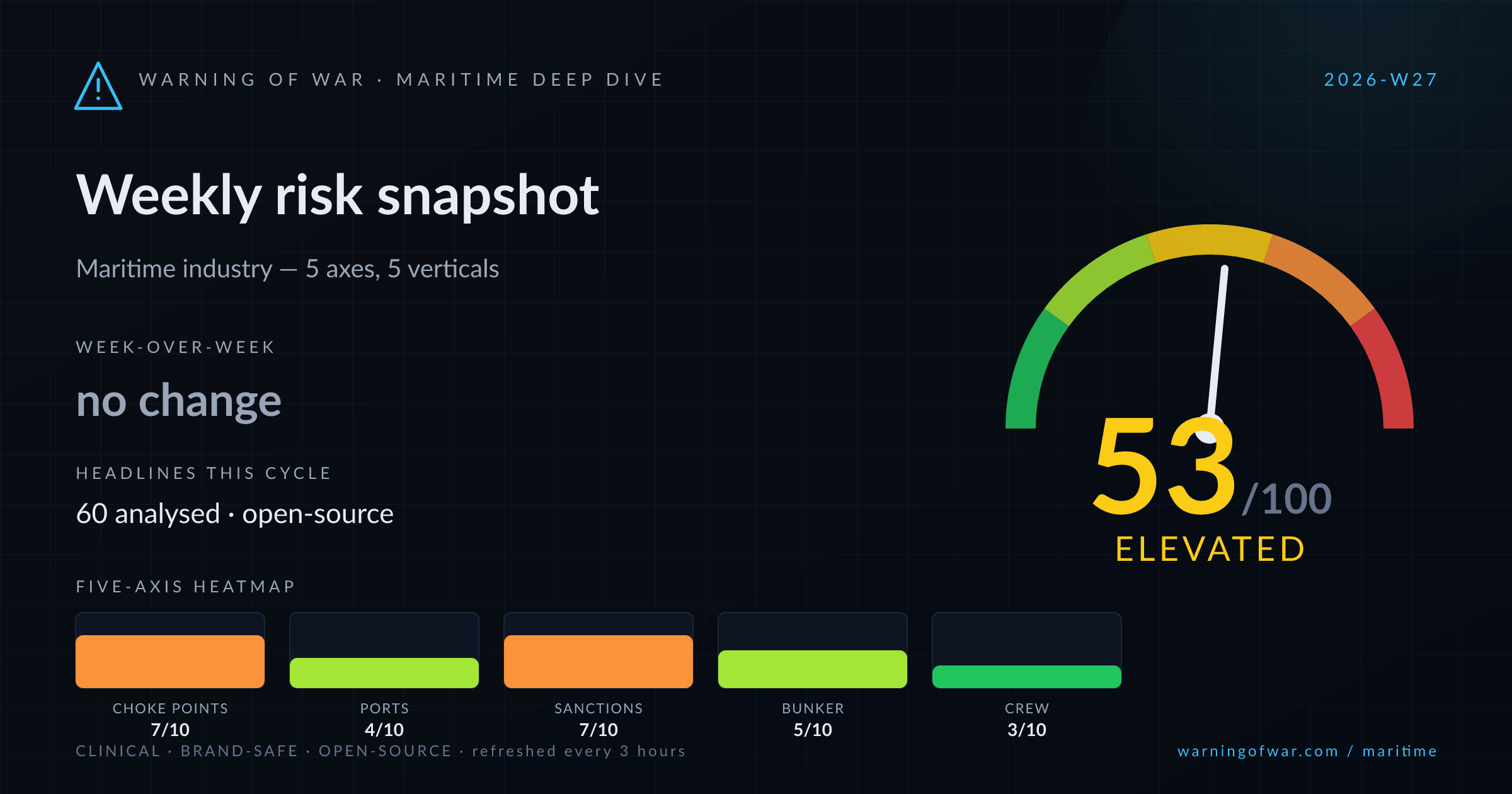

Weekly maritime industry risk snapshot — composite 53/100 (Elevated), ◆ first weekly snapshot.

The Strait of Hormuz dominates this scoring cycle: traffic is recovering following a period of elevated transit risk, with supertankers re-entering the Persian Gulf as US–Iran talks resume in Doha. War-risk premium pressure persists, and Oman's rejection of mandatory transit fees adds a regulatory dimension. Russia's price-cap ban extension through 2027 sustains shadow-fleet compliance scrutiny in the Baltic. Container markets are tightening — Maersk upgrades full-year 2026 guidance on Far East demand strength, while global shipping costs are reported at their highest level since the Red Sea disruption. Singapore bunker prices are rising, and B100 biofuel premiums are narrowing on EU routes, signalling active fuel-switch cost pressure.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

Critical

Hormuz transit recovery is driving a partial VLCC rate rebound, but elevated war-risk premiums and shadow-fleet compliance dynamics keep the sector at high stress.

Elevated

Dry-bulk fundamentals are steady but subdued, with copper pricing pressure and modest iron ore volume milestones offering mixed demand signals.

High

Container markets are at a high-stress inflection: Maersk upgrades full-year guidance on surging Far East demand and spot rates, while global shipping costs hit their highest level since the Red Sea disruption.

Elevated

Offshore wind sector is expanding in Europe and Korea, but Chinese supply-chain scrutiny in Korean bid awards is introducing geopolitical friction into project execution.

Guarded

Yacht and leisure sector shows no material new commercial stress signals this cycle; EcoMarine ESG index activity in the Black and Caspian Seas is the primary operational note.

Supertanker traffic through the Strait of Hormuz is recovering incrementally as US–Iran diplomatic talks resume in Doha, reducing acute rerouting frequency while war-risk insurance premiums remain above pre-disruption baseline.

President Putin extended Russia's ban on supplying oil subject to G7/EU price-cap mechanisms through end-2027, sustaining elevated sanctions-compliance cost and shadow-fleet activity across Baltic and dark-fleet tanker trades.

Global shipping costs have reached their highest level since the Red Sea blockade period, driven by sustained Far East demand strength and carrier capacity discipline, prompting Maersk's full-year 2026 earnings guidance upgrade.

A Russian civilian LNG carrier operating in the Baltic has been identified carrying heavy machine guns, raising war-risk and compliance scrutiny for vessels sharing Baltic transit corridors with Russian-flagged or Russian-chartered tonnage.

Oman has formally rejected mandatory transit fees for the Strait of Hormuz while indicating openness to maritime service charges, creating regulatory uncertainty for commercial operators planning Persian Gulf transits.

MSC's Terminal Investment Limited agreed to acquire a 49% stake in Adani Ports' Vizhinjam transshipment terminal for $1.4bn, accelerating Indian Ocean hub infrastructure consolidation and reshaping South Asia container routing.

Over the next 60–90 days, the Strait of Hormuz will remain the primary commercial variable: if US–Iran negotiations in Doha produce a durable framework, war-risk premiums on Persian Gulf tanker trades should compress and crude/LNG loadings from Oman, Iraq, and Qatar will normalise, providing a meaningful tailwind to VLCC and LNG carrier earnings. Conversely, any diplomatic breakdown re-elevates rerouting cost and war-risk premia across the tanker and LNG verticals. Container markets are likely to sustain elevated freight rates through Q3 2026 on Far East demand momentum and carrier blank-sailing discipline, though the risk of sudden demand softening — particularly if Fed tightening accelerates and Chinese domestic consumption remains weak — is non-trivial. Russia's 2027 price-cap ban extension will keep sanctions-compliance costs structurally elevated for tanker operators with CIS or Baltic exposure. Biofuel adoption dynamics, particularly B100 premium compression on Singapore–EU routes, will sharpen fuel-strategy decisions for operators preparing for FuelEU Maritime compliance. Offshore wind M&A in Europe and supply-chain scrutiny in Korea's tender programme are expected to generate further asset and regulatory activity through the quarter.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.