Geopolitical & Regional

6/10Elevated

Geopolitical & Regional risk at 60/100 — elevated for the week ahead.

WEEKLY REPORT · 2026-W24 · Jun 8 – Jun 14, 2026

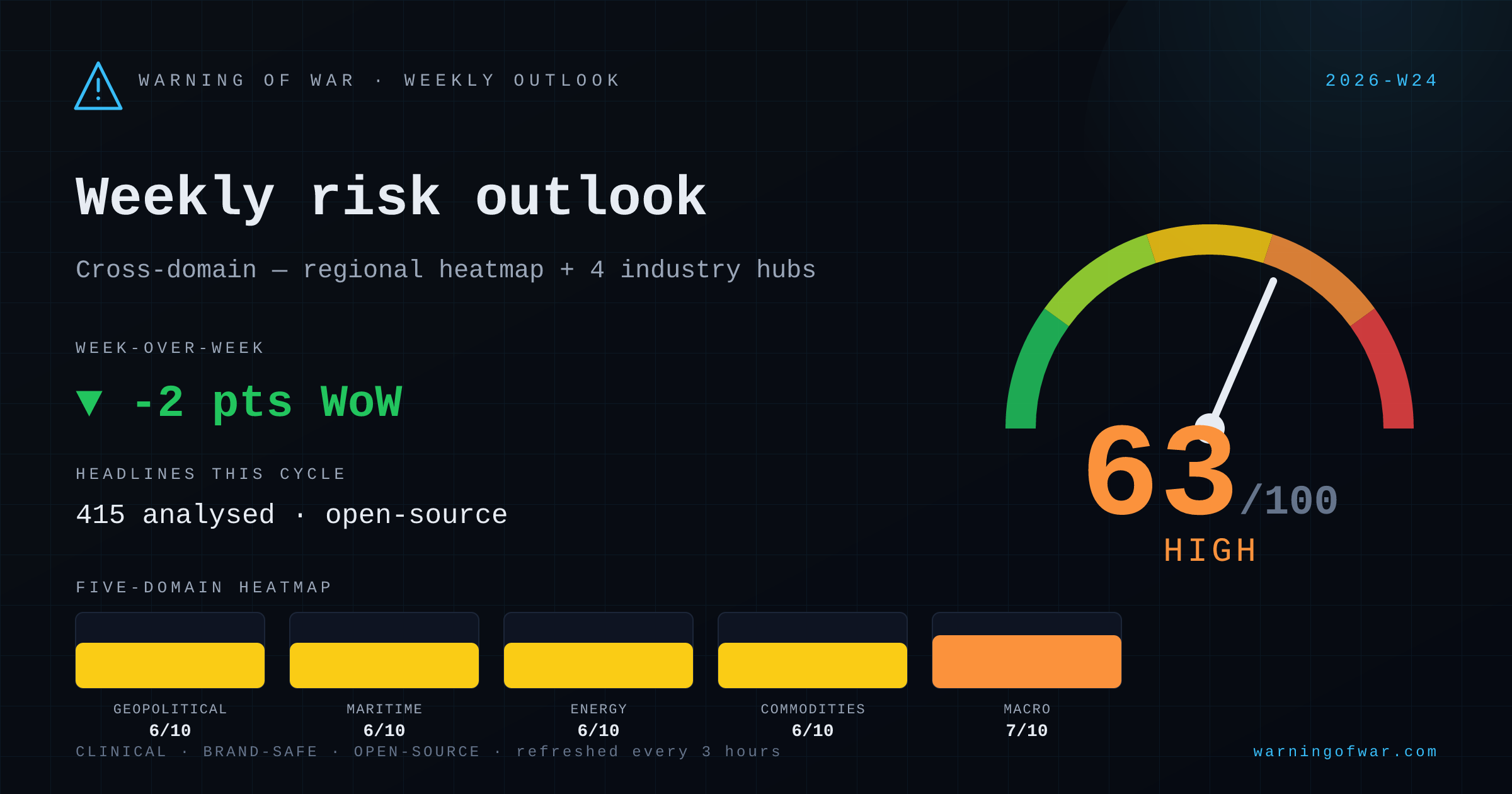

Weekly cross-domain risk snapshot — composite 63/100 (High), ◆ first weekly snapshot.

Cross-domain composite holds at 63/100 (High) for the week ahead, blended evenly across the regional heatmap and the maritime, energy, commodities, and macro hubs. Macro & Sovereign leads the picture at 68/100; Energy Markets is the least-stressed domain at 60/100. 415 open-source headlines were analysed across all domains this cycle.

Each axis scored 1–10 from open-source signals. The composite at the top is a weighted blend.

Elevated

Geopolitical & Regional risk at 60/100 — elevated for the week ahead.

Elevated

Maritime & Supply Chain risk at 64/100 — elevated for the week ahead.

Elevated

Energy Markets risk at 60/100 — elevated for the week ahead.

Elevated

Commodities & Materials risk at 62/100 — elevated for the week ahead.

High

Macro & Sovereign risk at 68/100 — high for the week ahead.

The ECB is expected to raise its benchmark rate by 25 basis points, leading G7 central banks in tightening and materially repricing eurozone sovereign and corporate borrowing costs.

Ongoing Middle East conflict is sustaining a cost premium on European energy imports routed through eastern Mediterranean and Red Sea corridors, feeding directly into ECB inflation deliberations.

Tata Steel's £1.25bn electric arc furnace project faces a delay attributable to electrical grid connectivity constraints, deferring a significant uplift in domestic UK steel production capacity.

Multinational NATO naval exercise activity in the Baltic Sea is applying marginal upward pressure on regional maritime insurance risk classifications and route risk premiums.

Houthi forces have declared a formal ban on Israeli-linked vessel transits through the Red Sea, operationally restricting a key segment of Asia-Europe shipping traffic and increasing diversion to longer alternative routes.

Reciprocal aerial strike activity between Israel and Iran has introduced material operational uncertainty for energy infrastructure assets — including refinery, terminal, and grid capacity — in both countries.

The week ahead is led by Macro & Sovereign and Maritime & Supply Chain risk. Detailed five-axis decompositions follow in this week's sector deep dives — Maritime on Tuesday, Commodities and Energy on Wednesday, and Macro on Thursday. This outlook synthesises the live regional heatmap with all four industry hubs, refreshed every three hours from open-source signals.

← All weekly reports · Methodology →

Important: Warning of War provides AI-generated risk intelligence from public open-source data. Output is informational only — not investment advice, official assessment, or operational guidance. Always consult primary sources and qualified analysts before any commercial decision.